Download

1 / 5

50 likes | 76 Views

E N D

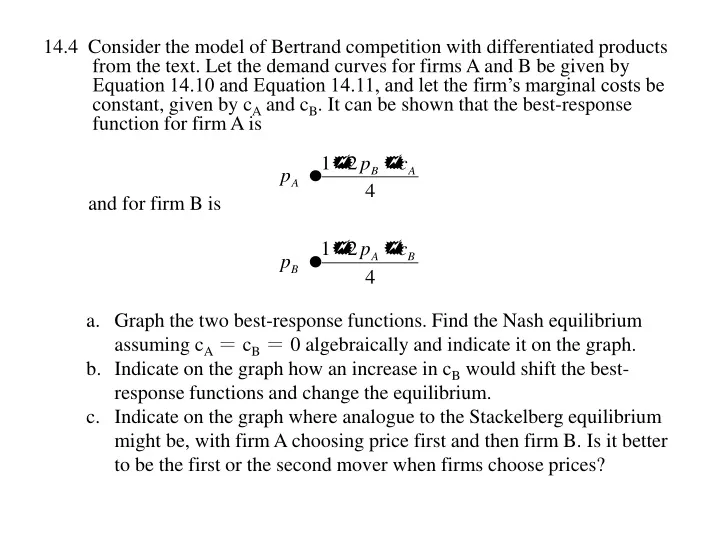

14.4 Consider the model of Bertrand competition with differentiated products from the text. Let the demand curves for firms A and B be given by Equation 14.10 and Equation 14.11, and let the firm’s marginal costs be constant, given by cA and cB. It can be shown that the best-response function for firm A is and for firm B is • Graph the two best-response functions. Find the Nash equilibrium assuming cA= cB= 0 algebraically and indicate it on the graph. • Indicate on the graph how an increase in cB would shift the best-response functions and change the equilibrium. • Indicate on the graph where analogue to the Stackelberg equilibrium might be, with firm A choosing price first and then firm B. Is it better to be the first or the second mover when firms choose prices?

14.10 Suppose that the total market demand for crude oil is given by QD= 70,000 - 2,000P where QD is the quantity of oil in thousands of barrels per year and P is the dollar price per barrel. Suppose also that there are 1,000 identical small producers of crude oil, each with marginal costs given by MC = q + 5 where q is the output of the typical firm. • Assuming that each small oil producer acts as a price taker, calculate the typical firm’s supply curve (q = . . .), the market supply curve (QS = . . .), and the market equilibrium price and quantity (where QD = QS). • Suppose a practically infinite source of crude oil is discovered in New Jersey by a would-be price leader and that this oil can be produced at a constant average and marginal cost of AC = MC = $15 per barrel. Assume also that the supply behavior of the competitive fringe described in part a is unchanged by this discovery. Calculate the demand curve facing the price leader.

Assuming that the price leader’s marginal revenue curve is given by how much should the price leader produce in order to maximize profits? What price and quantity will now prevail in the market?

![Market Research Report - Global Forecast on Oil Recovery [2020]](https://cdn4.slideserve.com/7244751/slide1-dt.jpg)