Download

1 / 28

280 likes | 429 Views

VIII Keynesian revolution – economic policies. Legacy for economic policy. Keynesian theory suffered significant setbacks, BUT Two Keynesian conclusions survived till today: Capitalist economy, if left to market forces, can operate for a long time with substantial involuntary unemployment

E N D

Legacy for economic policy • Keynesian theory suffered significant setbacks, BUT • Two Keynesian conclusions survived till today: • Capitalist economy, if left to market forces, can operate for a long time with substantial involuntary unemployment For practical purpose, it is not important whether the economy might converge towards full employment equilibrium, if this happens with long delay • Insufficient demand is the principal culprit of depression situation, hence fiscal and/monetary demand stimulation are the principle tools of short term economic policies It is the role of the Government to perform this demand stimulating policies

Keynes’ policy prescriptions • His principal focus – the depression situation • Aggregate demand requires stimulation • Subsequent simplifications: fiscal and monetary multipliers in the framework of ISLM model • Easy illustration of the basic idea, bellow we will do the same • Keynes himself – much wider considerations: • Concern about autonomous components of consumption and – especially – investments (famous quote on “socialization of investment”) • Understanding the role of expectations • Concern about the political forces and the role of trade unions • All this quite often quoted by his disciples, but almost nothing survived as to the practical recommendations • Entire victory of simplified, “hydraulic” ISLM interpretation

Policy innovations (1) • Fiscal and monetary policies • Preference of fiscal policies • Monetary policy less efficient due to almost flat LM curve and interest-inelastic investment • Sharp departure from pre-1930 policy taboos: • Accepts budget deficits • Refuses the crowding-out effect – remember LIV: fiscal stimulation via increase of government spending is crowding-out the either personal consumption of private investment • Here his views were shared by many economists, but widely opposed by British Treasury (Finance Ministry) – the “Treasury view” problem

Policy innovations (2) • Refused wage cuts as a remedy for depression • Both on political and economic ground • Political power of trade unions and social tension during the depression • In the US, real wages were falling during most of 1930’s, without any practical impact • Similar situation observed in many other countries (except Britain, due to overvalued currency) • Fiscal multiplier and its effect on growth and employment • The policy role of the governments: the theory provides the tools to increase the product (and employment) by stimulating aggregate demand • Government is the only “agent” on the market, capable to perform this role

ISLM vs. complete model • The complete model multipliers (as we did for Classical model in LIV) – see Sargent’s textbook in Literature • Requires more theoretical discussion on specification of consumption and investment function – beyond the scope her • Instead – ISLM illustration • Keep in mind that it is a simplification

VIII.2.1 Fiscal policy in ISLM • Changes of governmental expenditures • Changes in tax rates • Transfers to population (not included in the simple model here) • Time aspect

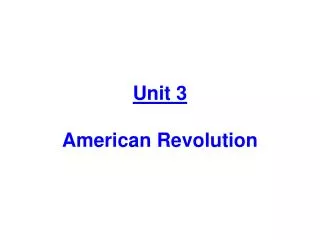

Increase of governmental expenditures • Initial equilibrium in • Increase: → higher AD • Shift of IS (when each level of interest corresponds to higher level of Y) → at given interest, point A represents new equilibrium on goods market • However, in A, disequilibrium on money market (off LM curve), EDM→ interest → I → AD → Y • New equilibrium in

LM r A Y

Multiplier of governmental expenditures • Differentiation of both equations: , hence • Substituting in the first equation for dr from second equation and after arrangement we have • By assumptions and

Crowding out effect (1) • In ISLM model, multiplier of governmental expenditures is lower than the same multiplier for the goods market only (when interest is given) • Full model (and in reality) – higher governmental expenditures are partially offset by decrease of investment (due to the increase of interest) - G crowds out private investment • Formally: impact of the term

Crowding out effect (2) • Keynes (short term): increase in governmental expenditures will have higher impact on product when • Interest elasticity of demand for money is high (LM curve almost horizontal) • And/or interest elasticity of investment is low (IS curve very steep) • Hence • Classical model (long term): vertical LM ↔ increase of governmental expenditures fully crowds out private investment

Tax policies • Simplification: • Tax multiplier (derived equally as above) • Policy induced change: impact of the tax change enabled first through the change of disposable income, than impact on consumption, AD and product (income); only than multiplier applies. • Effect less certain – the reaction of consumers to a tax change might modify MPC .

Balanced budget multiplier • Keynes – allowed for budget deficit • Reality – budget balance is always watched • Question: what is the multiplier in case of equal change in governmental expenditure and amount of taxes, i.e. and after arrangement • Balanced budget multiplier is equal one.

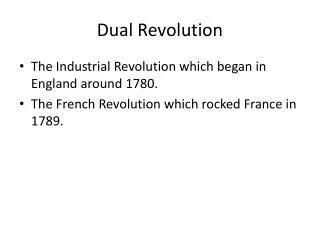

VIII.2.2 Monetary policy in ISLM • Original equilibrium in E1 • Increase of money supply • At given Y, excess supply of money → higher demand for bonds, higher price of bonds and lower interest → shift of LM to the right, new equilibrium on money market at point A • However, disequilibrium at goods market (EDG) → low interest increases investment, AD and product. Higher product increases demand for money → increase of interest → overall equilibrium at E2

r A IS Y

Multiplier of monetary policy • Again, differentiation of both equilibrium conditions, hence • After arrangements

Efficiency of monetary policy • The higher efficiency (impact on product growth) of monetary policy, • The lesser interest elasticity of demand for money (the steeper is demand for money and LM curve as well) • The higher is interest elasticity of investment (the flatter is IS curve • If (flat LM) , than multiplier of monetary policy is equal to zero and monetary policy is entirely ineffective → liquidity trap

VIII.2.3 Some crucial differences with Classical model • Equilibrium at less than full employment • and demand does not have to equal supply on some markets • Quantitative adjustment, wages and prices adjust slowly • Money in not neutral • It is not a veil • Demand stimulation is not completely crowded out

Basics • Capitalist economy must be steered towards full employment output by policies, performed by the governments, stimulating aggregate demand • Monetary policies less efficient → crucial role of fiscal policies • Multiplier effect • When output at less than full employment level, then wages and prices adjust slowly • Downward wage rigidity as general concept • At full employment out put level – classical model applies again

Keynes’ wrong predictions (1) • Estimate if numerical value of fiscal multiplier • Expectations up to value of 3, in reality just above 1 • Inherent stagnation of the capitalist economy, APC falls with growing income • Not proved by the data (Kuznets) • High interest elasticity of money demand (reason for liquidity trap) or low interest elasticity of investment • Not validated by the data

Keynes’ wrong predictions (2) • Expectation about the return of recession after the end of WWII • Lack of aggregate demand, either because of lack of consumer demand (low income and/or falling APC) or investment demand (after the war economy stops to generate government military demand) • Completely refuted by the post-WWII economic development • Till today discussion of this was result of the application of Keynesian recommendations of not • See next Lectures, but: after WWII, it was mainly the effect of private investment that filled the gap between AD and AS

Lasting impact on economic policy • After Keynes: for more than 3 decades, a prevailing view was that the governments must intervene to steer capitalist economy towards production at full employment • This remained accepted by many (not only economists), even by those who criticize Keynes or understand his fallacies • After 1970 – a reversal in prevailing views (see chapters later) • Today: • his model is considered as one stage in the development of macroeconomics • new Keynesian economics (see later)

Literature to Ch. VIII Again, the literature to this Lecture is immense, bellow are 3 recommendations • ISLM model as policy instrument – any intermediate textbook on macroeconomics • Snowdon, B., Vane, H.: Modern Macroeconomics, Edvard Elgar, 2005, namely Chapter 3 (and the literature given here) • Blaugh, M.: Economic Theory in Retrospect, CUP 1997 (5th edition), Chapter 16, namely parts 16.1-16.5 and 16.19-16.23