Download

1 / 13

130 likes | 255 Views

The Causes and Consequences of Rising Health Insurance Premiums. Mark Pauly, Ph.D. Wharton School University of Pennsylvania. Two Problematic and Puzzling Propositions.

E N D

The Causes and Consequences of Rising Health Insurance Premiums Mark Pauly, Ph.D. Wharton School University of Pennsylvania

Two Problematic and Puzzling Propositions • 1. The bulk of the growth in health insurance premiums comes either from things that we do not want to control or from things we find very hard to control. • 40-70% of growth: costly but beneficial new technology • Almost all of the rest: higher wages and profits, increased incidence of some diseases. • Trivial: aging of the population (0.5%)

Two Problematic… • 2. Workers almost always pay for almost all of their health insurance. • They pay part through explicit premiums • They pay the rest (the “employer contribution”) through lower growth in money wages. So the share doesn’t matter. • Mandating that employers pay is a disguised employee mandate that makes workers take lower raises. • No need to thank the boss (or thank for wages)

The Question • In the face of these facts, what is good public policy? • Define “good.” • 1) not perfect; that is impossible and there are inevitably going to be tradeoffs. • 2) any change should help to improve efficiency • 3) any change should help to improves equity. • 4) any change should be politically feasible.

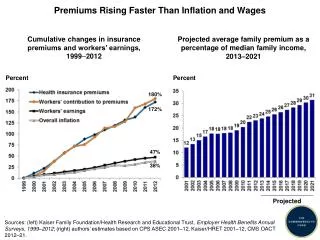

Two Different Questions That Are Often Confused • What causes health insurance premiums to be “high” (relative to income, GDP,etc)? • What causes health insurance premiums to rise (faster than almost anything)? • Focusing on the answers to the first question may not help with the second.

Why Are Premiums “High”? • People get sick and want treatment. • Some wages and profits are above average. • “Inefficiency” (My guess: 15-20%) • Administrative costs and insurer profit or surplus.

Why Are Premiums Rising (at 4-5% real rate per year, or more)? • As noted, mostly because of beneficial but net costly new technology (including new ways to use old tech; also driven by quality effects on demand). • Wages for non-doctors rising faster than average. • Sometimes, increased incidence of some illnesses (more true now than in 1980).

The good news and the not-so-good news for Hawai’i • Probably possible to close most of the gap with subsidies to basic insurance coverage for “tweeners” and expanding Medicaid to able-bodied adults. • But the inexorable technology driven rise in premiums is going to offer stronger incentives to tweeners to avoid the mandate and will impoverish those who cannot avoid it. • % uninsured in Hawai’i only slightly below PA.

Short run solutions • Design a decent but basic policy for tweeners and Evel Knievels of health insurance. • Subsidize fairly generously, thru vouchers • Do not raise the subsidy by taxing premiums—shoots yourself in the foot. • Tax income, french fries, anything with an inelastic demand or that you want people to do less of.

Short run solutions 2 (More tentative) • Offer this policy in a well functioning individual market since self employed and part timers are not good group members. • Permit choice but have a fallback insurer (state employee plan?)

Long run solutions • Face facts: we are not going to IT or disease manage our way out of permanent premium growth. We will need to sacrifice. • Try to develop a rational policy toward new technology and make sure the law does not inhibit. • Would there be a market for a “prudent adoption” or “go slow” insurance policy?

Hope and Conclusions • A few bittersweet hints that we may be coming in for a smooth landing in which premiums still grow but not as fast as income. • Lower rate of introduction of new drugs. • Current on-trend spending growth seems recently related more to the increased incidence of some disease than pure technology. • We need to be able to have a civil conversation about hard things.