Download

1 / 56

590 likes | 830 Views

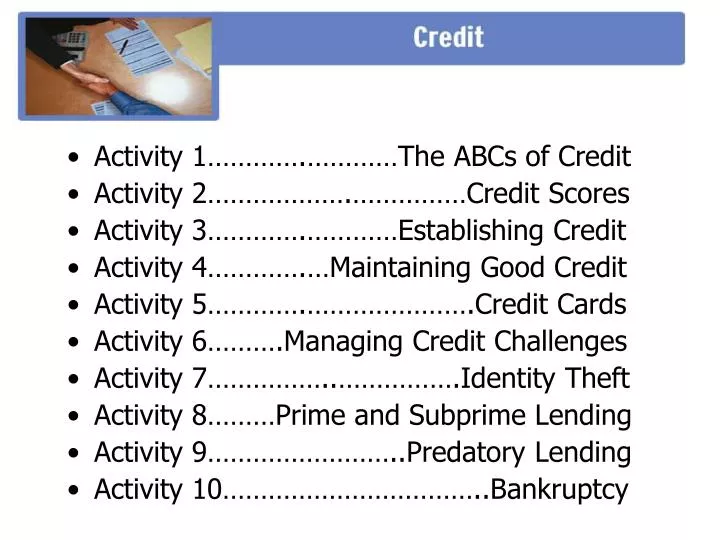

Activity 1………….…………The ABCs of Credit Activity 2……………….……………Credit Scores Activity 3………….…………Establishing Credit Activity 4………….…Maintaining Good Credit Activity 5………….………………….Credit Cards Activity 6……….Managing Credit Challenges Activity 7……………..…………….Identity Theft

E N D

Activity 1………….…………The ABCs of Credit • Activity 2……………….……………Credit Scores • Activity 3………….…………Establishing Credit • Activity 4………….…Maintaining Good Credit • Activity 5………….………………….Credit Cards • Activity 6……….Managing Credit Challenges • Activity 7……………..…………….Identity Theft • Activity 8………Prime and Subprime Lending • Activity 9……………………..Predatory Lending • Activity 10……………………………..Bankruptcy

Credit - Activity 1 • ACTIVITY 1 • The ABCs of Credit • Overview • What is credit? • The five Cs of credit • Pros and cons of using credit • The big decision—Should I use credit? 2

CREDIT DEFINITIONS Credit Trust given to another person for future payment of a loan, credit card balance, etc. Creditor A person or company to whom a debt is owed. 3 Slide 1 – Credit Definitions Lesson Reference: Credit, Activity 1 – Handout 1

Slide 2 - The Five Cs of Credit Lesson Reference: Credit, Activity 1 – Overhead 1 THE FIVE Cs OF CREDIT C = Capacity C = Capital C = Collateral C = Conditions C = Character 4

WHEN TO USE CREDIT Can you describe a situation when it is a good time to use credit and when it is NOT a good time to use credit? 5 Slide 3 – When to Use Credit Lesson Reference: Credit, Activity 1 – Handout 2

QUESTIONS TO ASK BEFORE USING CREDIT 1. 2. 3. 4. 5. 6. 7. 6 Slide 4 – Questions to Ask Lesson Reference: Credit, Activity 1 – Handout 3

ACTIVITY 2 • Credit Scores • Overview • Credit scores and their impact • The factors that make up a credit score • Strategies to improve your credit score 7 Credit - Activity 2

WHAT IS A CREDIT SCORE? • A credit score is a number that helps a lender predict how likely an individual is to repay a loan, or make credit payments on time. • A credit score is a number that changes as the elements in a credit report change. • A credit score has broad use and impact. Your credit past is your credit future. • FICO® scores, one of the most common credit scoring systems, vary between 350 and 850. • VantageScoreSM, a new credit scoring system developed by the three credit bureaus, ranges from 501-990. 8 Slide 1 – What Is a Credit Score? Lesson Reference: Credit, Activity 2 – Overhead 1

WHAT MAKES UP A TYPICAL CREDIT SCORE? Source: Fair Isaac and Consumer Federation of America, 2005 9 Slide 2 – What Makes Up a Typical Credit Score? Lesson Reference: Credit, Activity 2 – Overhead 2

IMPROVING YOUR CREDIT SCORE • Pay bills on time. • Get current and stay current. • Don’t open a lot of new accounts too rapidly. • Correct mistakes. • Shop for loan rates within a focused period of time. • Keep balances low on revolving credit. • Pay off debt. • Check your credit report. 10 Slide 3 – Improving Your Credit Score Lesson Reference: Credit, Activity 2 – Handout 2

Credit - Activity 3 • ACTIVITY 3 • Establishing Credit • Overview • Types and sources of credit • Credit safeguards • Applying for credit • Questions to ask when applying for credit 11

TYPES OF CREDIT Cash Credit Sales Credit Secured Credit Revolving Credit I.O.U. Single Payment Credit Installment Credit Other Types of Credit 12 Slide 1 – Types of Credit Lesson Reference: Credit, Activity 3 – Handout 1

Slide 2 - Sources of Credit Lesson Reference: Credit, Activity 3 – Overhead 1 SOURCES OF CREDIT Banks Credit Unions Retail Stores Finance Companies Savings & Loan Associations Internet Stores What are other sources of credit? What sources of credit should be avoided? Why? 13

STEPS TO TAKE TO AVOID • ABUSIVE LENDING • Have you shopped around for the best deal? • Do you feel the lender pressured you to take the loan? • Do you understand the terms of the loan? 14 Slide 3 – Avoiding Abusive Lending Lesson Reference: Credit, Activity 3 – Handout 2

COMMON PARTS OF A • CREDIT APPLICATION • Reason for Loan • Personal Identification Information • Employment Information • Mortgage/Rental Information • Documentation Required (for some applications) • Current Debts • Credit References • Collateral (for some applications) • Bank References • Signature and Date 15 Slide 4 – Parts of a Credit Application Lesson Reference: Credit, Activity 3 – Handout 3

SAMPLE CREDIT APPLICATION 16 Slide 5 – Sample Credit Application Lesson Reference: Credit, Activity 3 – Handout 3

QUESTIONS TO ASK WHEN • APPLYING FOR CREDIT • What is the annual fee? • What is the annual percentage rate (APR)? • When are payments due? • What is the minimum payment required each month? • Is there a grace period? • Are there other fees associated with the credit, such as minimum finance charges? • What is the credit limit? • What are the penalties for late or missed payments? • What are the terms and conditions of the credit? What else is included in the fine print? 17 Slide 6 – Questions to Ask Lesson Reference: Credit, Activity 3 – Handout 5

Credit - Activity 4 • ACTIVITY 4 • Maintaining • Good Credit • Overview • Debt to income thermometer • Credit process • Credit reporting agencies • Credit safeguards for consumers • Credit reports, ratings and scores • Establishing a credit history 18

Slide 1 – Debt-to-Income Thermometer Lesson Reference: Credit, Activity 4 – Overhead 1 DEBT-TO-INCOME THERMOMETER 19

Slide 2 - The Credit Process Lesson Reference: Credit, Activity 4 – Overhead 2 THE CREDIT PROCESS CREDIT HISTORY • CREDIT BUREAU • CREDIT REPORT • CREDIT SCORE • CREDIT RATING 20

SAMPLE CREDIT REPORT 21 Slide 3 – Sample Credit Report Lesson Reference: Credit, Activity 4 – Handout 2

Slide 4 - Credit Safeguards for Consumers Lesson Reference: Credit, Activity 4 – Handout 3 CREDIT SAFEGUARDS FOR CONSUMERS Truth In Lending Act Fair Credit Reporting Act Equal Credit Opportunity Act Fair Credit Billing Act Fair Debt Collection Practices Act 22

THE FAIR AND ACCURATE CREDIT TRANSACTION ACT • One of the primary objectives behind the Fair and Accurate Credit Transaction Act (the FACT Act) is to help consumers fight the growing crime of identity theft. The following are some highlights of the Act. • Free credit reports • Fraud alerts and Active Duty alerts • Truncation: credit cards, debit cards, Social Security Number • Red flags • Disposal of consumer reports • Credit scores 23 Slide 5 – FACT Act Lesson Reference: Credit, Activity 4 – Handout 4

Slide 6 - Things to Establish Good Credit Lesson Reference: Credit, Activity 4 – Overhead 3 THINGS TO DO TO ESTABLISH AND MAINTAIN GOOD CREDIT What can everyone do to establish and maintain good credit? 1. Pay all bills on time. 2. Avoid late fees. 3. 4. 5. 6. 24

Credit - Activity 5 • ACTIVITY 5 • Credit Cards • Overview • Types of credit cards • Shopping for a credit card • Costs of credit 25

Slide 1 - Types of Credit Cards Lesson Reference: Credit, Activity 5 – Overhead 1 • TYPES OF CREDIT CARDS • Private Label • Issued by a single source • Can only be used at a single source • Examples: Department Stores, Gasoline Companies • General Label • Issued by a single source • Can be used in many places • Examples: Bank Card, Major Credit Card 26

Slide 2 - Shopping for a Credit Card Lesson Reference: Credit, Activity 5 – Overhead 2 SHOPPING FOR A CREDIT CARD DECISIONS, DECISIONS... ANNUAL FEE? APR? COMPUTATION METHOD? GRACE PERIOD? FINANCE CHARGE? CREDIT LIMIT? CARD INCENTIVES? 27

QUESTIONS TO ASK WHEN SHOPPING FOR A CREDIT CARD • Annual fee • Annual percentage rate (APR) • Minimum payment • Computation method • Grace period • Finance charges • Card incentives 28 Slide 3 – Questions to Ask Lesson Reference: Credit, Activity 5 – Handout 1

COSTS OF CREDIT How much can credit cost? If you make only the minimum payment for an item, here are some examples of what you might actually pay and how long it will take you to pay it. 29 Slide 4 – Costs of Credit Lesson Reference: Credit, Activity 5 – Handout 2

Credit - Activity 6 • ACTIVITY 6 • Managing Credit • Challenges • Overview • Warning signs of credit abuse • Credit card reductions • Correcting credit errors • Resources and assistance 30

MEASURING THE SERIOUSNESS OF CREDIT TROUBLE SIGNS Rate how serious you think each of the following trouble signs is. 1 = Not Serious 4 = Very Serious Trouble Signs • Delinquent Payments • Default Notices • Repossessions • Collection Agencies • Lien • Garnishment • Others? 31 Slide 1 – Rating Trouble Signs Lesson Reference: Credit, Activity 6 – Handout 1

WARNING SIGNS OF DEBT PROBLEMS • Delinquent Payments • Default Notices • Repossessions • Collection Agencies • Judgment Lien • Garnishment 32 Slide 2 – Warning Signs Lesson Reference: Credit, Activity 6 – Handout 2

CREDIT CARD REDUCTIONS Paying only the minimum payments on your credit card may seem appealing, but if only minimum payments are made, it can take years, and sometimes decades, to achieve full repayment. Paying the minimum amount due keeps your credit history clean, but it also costs you more. 33 Slide 3 – Credit Card Reductions Lesson Reference: Credit, Activity 6 – Handout 3

CORRECTING CREDIT ERRORS • Circle the incorrect items on your credit report. • Write a letter to the reporting agency, telling them which information you think is inaccurate. Provide supporting documentation. • Send all materials by certified mail. • Send a similar letter to the creditor whose reports you disagree with. • The reporting agency will conduct an investigation. • If negative information is accurate, it can stay on your report for 7-10 years. 34 Slide 4 – Correcting Credit Errors Lesson Reference: Credit, Activity 6 – Handout 4

CORRECTING CREDIT PROBLEMS • Take responsibility for actions. • Communicate with creditors. • Debt Consolidation • Credit Counseling • Bankruptcy 35 Slide 5 – Correcting Credit Problems Lesson Reference: Credit, Activity 6 – Handout 5

ACTIVITY 7 • Identity Theft • Overview • The growing problem of identity theft and how it occurs • Strategies to protect your personal information • Steps to take if your identity has been stolen. 36 Credit - Activity 7

IDENTITY THEFT Identity theft occurs when someone uses your personal identifying information to either establish credit under your name or to take over an existing account that you established without your authorization. This information may include: • Social Security Numbers • Name • Address • Date of birth • Mother’s maiden name • Passwords • PINs 37 Slide 1 – Identity Theft Lesson Reference: Credit, Activity 7 – Overhead 1

HOW TO AVOID IDENTITY THEFT • Monitor your credit report. • Don’t give out personal information to unknown persons or companies. • Protect your credit and debit cards. • Protect your mailbox. • Protect your wallet. • Use passwords and PINs that can’t be easily guessed. • Use anti-virus software on your computer. • Notify your bank when you change your address or phone number. • Other suggestions? 38 Slide 2 – How to Avoid Identity Theft Lesson Reference: Credit, Activity 7 – Handout 2

WHAT TO DO IF YOUR IDENTITY HAS BEEN STOLEN If you think your identity has been stolen, take the following steps: • Contact the three major credit bureaus (Equifax, Experian, and Trans Union). • Close accounts. • Contact all creditors involved. • File a police report. • Keep a record of your contacts. 39 Slide 3 – What to Do Lesson Reference: Credit, Activity 7 – Overhead 2

ACTIVITY 8 • Prime and Subprime Lending • Overview • Subprime and prime lending definitions • Alternative institutions that provide higher-cost loans • Strategies to improve credit in order to qualify for prime loans. 40 Credit - Activity 8

PRIME AND SUBPRIME MORTGAGE LENDING Prime Prime credit is typically available to an individual who has paid his or her outstanding credit on time. Subprime A subprime loan is typically available to a person with either no credit history or a damaged credit history and who is considered to be a high-risk borrower. Subprime loans have higher-than-average interest rates. 41 Slide 1 – Prime and Subprime Lending Lesson Reference: Credit, Activity 8 – Overhead 1

THE PRICE OF SUBPRIME LENDING How much does a subprime loan cost you? If you are making payments on a car, for example, you could be paying significantly more just for getting a loan with a higher interest rate. This added interest is significant over the life of the loan. 42 Slide 2 – The Price of Subprime Lending Lesson Reference: Credit, Activity 8 – Handout 1

MOVING FROM • SUBPRIME TO PRIME • Pay bills on time. • Correct mistakes. • Pay more than the minimum required. • Use credit sparingly. • Work with a reputable nonprofit credit counseling organization. If you currently have a lower credit score and want to be able to qualify for prime loans in the future, you should take steps to improve your credit. The following steps can help. 43 Slide 3 – Moving from Subprime to Prime Lesson Reference: Credit, Activity 8 – Handout 2

ACTIVITY 9 • Predatory Lending • Overview • Characteristics and warning signs of predatory lending. • The key targets of predatory lending. • Common abuses and scams. • Nonprofit organizations that can help consumers plagued by predatory lending. 44 Credit - Activity 9

PREDATORY LENDING • Sell properties for much more than they are worth, using false appraisals. • Encourage borrowers to lie about their income, expenses, or cash available for down payments in order to get a loan. • Knowingly lend more money than a borrower can afford to repay. • And many other scams. In communities across America, people are losing their homes and their investments because of predatory lenders, corrupt appraisers, mortgage brokers, and home improvement contractors who: 45 Slide 1 – Predatory Lending Lesson Reference: Credit, Activity 9 – Overhead 1

IDENTIFYING • PREDATORY LENDING • Packaging a loan with single-premium credit insurance products • Repeatedly refinancing a loan in a short period of time • Charging excessive rates and fees to a borrower who qualifies for lower rates and fees Predatory lending is not defined by federal law except to the extent that a loan is a high-cost loan and contains one of a fixed list of terms or conditions. Predatory or abusive lending practices can include: 46 Slide 2 – Predatory Lending Lesson Reference: Credit, Activity 9 – Handout 1

TEN WARNING SIGNS OF • PREDATORY MORTGAGES • Unreasonably high interest rates • Multiple refinancing • Unnecessary debt consolidation • Balloon payment • Negative amortization • Door-to-door solicitation • Back-dating of documents • Large loan broker fees • Kickbacks between lender and broker • Single-premium credit life insurance 47 Slide 3 – Ten Warning Signs Lesson Reference: Credit, Activity 9 – Handout 1

COMMON SCAMS • Advance fee schemes • The prize that will cost you • Online auctions • Fraud jobs • Moneymaking schemes • Bogus charities • Scam schools 48 Slide 4 – Common Scams Lesson Reference: Credit, Activity 9 – Handout 2

TOP STRATEGIES TO AVOID SCAMS • Don’t become a victim. • Investigate strangers who have deals too good to be true. • Always stay in charge of your money. • Don’t be fooled by appearances. • Watch out for salespeople who prey on fears. • Monitor your investments. • Report fraud or abuse. • Do your homework. • Be wary of door-to-door solicitations. 49 Slide 5 – Top Strategies to Avoid Scams Lesson Reference: Credit, Activity 9 – Handout 2

ADDITIONAL RESOURCES • Department of Housing and Urban Development (HUD)— Office of Consumer and Regulatory Affairs, Interstate Land Sales/RESPA Division. (202) 708-4560; www.hud.gov/complaints/landsales.cfm. • Federal Deposit Insurance Corporation (FDIC)— Consumer Affairs Division. (877) ASK-FDIC (925-4618); www.fdic.gov. • Federal Trade Commission (For federal lending violations involving mortgage and consumer finance companies.) (877) FTC-HELP (382-4357); TTY (202) 326-2502; www.ftc.gov. • Federal Reserve Board of Governors of the Federal Reserve System— Division of Consumer Affairs. (202) 452-3693; www.federalreserve.gov/pubs/complaints. 50 Slide 6 – Additional Resources Lesson Reference: Credit, Activity 9 – Handout 3