Download

1 / 38

380 likes | 499 Views

Building Insurance into Your Client’s Estate Plan. Kevin Wark, LLB, CFP. CIFPS Annual National Conference. Case Study. Your client, Ron is 65 years old Married to Lisa (62) – second marriage Ron has two children, Mary (32) and Richard (27) both from first marriage

E N D

Building Insurance into Your Client’s Estate Plan Kevin Wark, LLB, CFP CIFPS Annual National Conference

Case Study • Your client, Ron is 65 years old • Married to Lisa (62) – second marriage • Ron has two children, Mary (32) and Richard (27) both from first marriage • Currently 2 grandchildren – uncertain if there will be more in the future

Case Study • Ron started a manufacturing company 20 years ago, currently valued at $3 million and drawing salary/bonus of $200,000 per year • Mary is involved in the business as VP Marketing • Richard currently traveling in Europe • Commercial property acquired for $400,000 in 1996, currently valued at $600,000 – rented to business for $40,000 pa. and has UCC of $200,000

Case Study • Ron’s other main assets consist of personal residence, $300,000 in RRSPs, $200,000 in shareholder loans • Ron has personally guaranteed $1 million loan to business • Ron is President of local hospital board • Home (valued at $400,000) has no mortgage and no other major debts

Ron’s Estate Objectives • Ensure Lisa has income of at least $200,000 per year (before-tax) if he predeceases her • Pass on business to daughter (Mary) • Treat son (Richard) “fairly” on his death • Minimize impact of taxes on his estate

Ron’s Estate Objectives • Provide gifts to grandchildren for post secondary education and other significant obligations • Creditor protect his estate • Large gift to the hospital on death

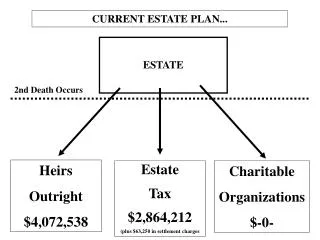

Some Observations • Value of estate assets (before tax) is approximately $4.5 million • Taxes could reduce estate by approx. 20% ($900,000) • Major asset (representing almost 75% of aggregate estate) going to daughter

Conflicting Demands on the Estate Plan • Ron wants major estate asset to go to the daughter – impact on income to Lisa and ability to be “fair” to Richard • Significant tax and other liabilities may impact viability of estate plan • How to fund gifts to grandchildren and charity from estate?? • Family law implications

Planning Idea #1– Collateral Insurance • Corporation acquires $1 million term or permanent policy on Ron’s life • Corporation assigns or hypothecates policy to bank as collateral for loan • Corporation can deduct lesser of premium and “net cost of pure insurance”

Planning Idea #1 – Collateral Insurance • Insurance proceeds would repay loan on Ron’s death and corporation would receive credit to its capital dividend account (CDA) • CDA could be used to flow tax-free dividends to Lisa to provide required level of income (subject to availability of cash in the corporation) or convert to secured shareholder loan • Removes significant liability from corporation and Ron’s estate

Planning Idea #2 – Creditor Protection/Capital Growth • Ron has significant wealth tied up in his business • Ron also has $200,000 shareholder loan account subject to business risks • Corporation could repay shareholder loan and replace with conventional bank debt • Split dollar arrangement between corporation and Ron for $1 million exempt UL contract

Planning Idea #2 – Creditor Protection/Capital Growth • Under a split dollar arrangement the Corporation owns death benefit and pays term costs of policy • Ron owns the cash value and funds with proceeds from the repaid shareholder loan • Corporation assigns its interest to the bank and can deduct lesser of premium and net cost of insurance • On Ron’s death the corporate debt is repaid by insurance proceeds and cash values flow to Lisa on tax-free basis outside of estate

Planning Idea #2 – Creditor Protection/Capital Growth • Corporation pays $31,000 per year for insurance coverage of $1 million • Ron pays $24,000 per year for 10 years and owns tax-deferred cash values • Assuming death at age 85, corporation receives $1 million (full credit to CDA) and Ron’s estate receives over $700,000 • Represents a total return of 5.5% (after-tax) and 10% (before-tax) on Ron’s deposits

Planning Idea #3 – Estate Freeze/ Buy-Sell with Mary • Ron converts common shares into two classes of shares redeemable for $500,000 and $2.5 million respectively (total of $3 million) • As part of this transaction Ron also completes an estate freeze and increases cost base of first class of preference shares to $500,000 • Deferred tax liability on shares of approximately $600,000 • New common shares issued to Mary

Planning Idea #3 – Estate Freeze/Buy-Sell with Mary • Buy-sell agreement between Ron, Lisa, Richard and Mary funded by corporate owned insurance • Corporation acquires $3 million permanent insurance policy on Ron’s life • Under Ron’s will $2.5 million low ACB shares are transferred to Lisa and $500,000 high ACB shares to Richard • Lisa’s shares are redeemed by the Corporation – no gain or loss on redemption as funded by capital dividend arising from insurance proceeds

Planning Idea #3 – Estate Freeze/Buy-Sell with Mary • Mary buys Richard’s shares for $500,000 with a promissory note • Remainder of insurance proceeds flowed out to Mary to repay promissory note • Lisa receives $2.5 million tax-free, Richard $500,000 tax-free and Mary has all common shares (worth at least $3 million) with $500,000 ACB

Planning Idea #4 - Estate Equalization • Ron wants to ensure Richard and Mary are treated “equitably” on his death • Mary will be sole owner of a corporation worth between $3-4 million • Assume Richard has received $500,000 tax-free on sale of preferred shares to Mary • Still significant disparity in values being received by children upon Ron’s death

Planning Idea #4 – Estate Equalization • Simplest and most cost effective approach would be to purchase joint second to die insurance on lives of Ron and Lisa • Make Richard beneficiary of policy • On death of surviving parent Richard will receive a tax-free gift outside of the estate • Cost of $500,000 UL policy - $6,600 p.a.

Planning Idea #5 - Estate Equalization • Another option would be for Ron to transfer the commercial property to his Corporation on a rollover basis • Ron would take back redeemable preference shares with redemption value of $600,000 and ACB of $200,000 • Mary would enter into agreement with Ron to purchase shares on Ron’s death

Planning Idea #5 - Estate Equalization • Mary would acquire a $600,000 policy on Ron’s life to fund purchase of shares • Taxable gain in Ron’s estate on shares • Ron’s will would provide for after-tax sale proceeds to flow to Richard • Mary would own preference shares with full cost base

Charitable Gifting • Number of ways to cost effectively structure major gifts on death • Can be funded through personal or corporate dollars • Can structure to receive tax credit for premium payments or death benefit

Planning Idea #6 – Personal Charitable Gift while Alive • Ron could purchase $200,000 insurance policy and gift to the hospital • Ron would be able to claim a tax credit for premiums paid on policy after transfer • 10 Year Direction to hold would exclude gift from charity’s disbursement quota

Planning Idea #7 – Personal Charitable Gift on Death • Ron acquires $200,000 insurance policy and designates hospital as beneficiary • No charitable credit for premiums paid • On Ron’s death estate can claim entire death benefit as charitable gift • Gift bypasses estate and potential creditors • Tax credit available to offset gains on death (i.e. from sale of preference shares to Mary)

Planning Idea #8 – Corporate Charitable Gift • Ron’s Corporation could purchase $200,000 policy on his life • On Ron’s death life insurance proceeds could be gifted to the hospital (cannot designate hospital as direct beneficiary) • Corporation can claim deduction for donation • Corporation also receives $200,000 credit to the capital dividend account – tax free dividends

Planning Idea #9 – Gifts to Grandchildren • Complicated by fact these are not natural grandchildren of Ron’s wife • Ron will want to take steps to “protect their inheritance” • Purchase insurance to provide gifts on death • Could establish life insurance trusts to hold benefits for grandchildren • Benefits include bypassing the estate and management of funds while grand children are minors

Three years later… Ron has incorporated a holding company, sold the operating business and invested after-tax proceeds in the holding company

Planning Idea #10 – Corporate Insured Annuities Objectives of Program • Increase corporate investment yield and cash flow • Increase value of estate by reducing taxes • Facilitate distribution of corporate assets on tax effective basis

Corporate Insured Annuities - Process • Corporation applies for $4 million joint first to die UL on Ron and Lisa’s life • Corporation liquidates $4 million of investments to purchase a “life 0” annuity with payments to the first death of Ron and Lisa • Corporation borrows $4 million to replace investment portfolio • Corporation assigns both contracts to bank as security for loan and pays interest annually

Corporate Insured Annuities – Cash Flow Annuity payments used to: • Pay insurance premium ($177,500 pa) • Pay loan interest ($340,000) @ 8.5% • Pay taxes on annuity (non-prescribed) * $36,600 in year 1 * $80,600 in year 2 and declines every year thereafter

Corporate Insured Annuities – Cash Flow Corporate Income Taxes Reduced by: • Loan interest expense ($340,000) • NCPI deduction ($146,000 in year 1 and increases to equal total premium in year 3) Loan is repaid with insurance proceeds on Ron’s death

Corporate Insured Annuities – Cash Flow in Year 1 Inflow Outflow Annuity $367,000 Insurance $177,500 Loan Interest 340,000 Tax on Annuity* 36,600 Tax Savings* $243,000 Net Cash Flow $60,000 * Assuming 50% corporate rate

Corporate Insured Annuities – Cash Flow in Year 2 Inflow Outflow Annuity $367,000 Insurance $177,500 Loan Interest 340,000 Tax on Annuity* 80,600 Tax Savings* $259,000 Net Cash flow $30,000 * Assuming 50% corporate tax rate

Corporate Insured Annuities –Impact while Ron is Alive • No reduction in corporate investments (except for any tax payable on disposition) • Loan fully secured (other security may be required) • Positive cash flow as a result of tax deductions

Corporate Insured Annuities – Tax consequences on Death • Corporate shares deemed disposed of at FMV – insured annuity has no value for tax purposes • Corporate value reduced by bank loan of $4 million (tax savings of up to $1 million) • CDA credit of $4 million less ACB of policy (allowing corporate investments to be extracted on tax-free basis)

Corporate Insured Annuity - Risks • Liquidation of corporate assets may have tax consequence and/or penalties for early termination • Interest rate fluctuations – borrowing rates may rise but annuity rates are fixed • No commutation value for annuity • Separate insurers should be used for life insurance and annuity contracts

Corporate Insured Annuities - Risks • General anti-avoidance rule (has value of company really been reduced?) • Interest deductibility (new REOP proposals requires annual testing) • Financial strength of insurance companies backing the arrangement

Other Planning Tips • Joint second to die insurance if Ron is substandard/uninsurable or for corporate back to back scenario • Use of holding companies for corporate-owned insurance (creditor proofing, avoids transfer on sale of operating business, valuation issues) • Having other family members or business partners share in costs of insurance