Download

1 / 0

0 likes | 106 Views

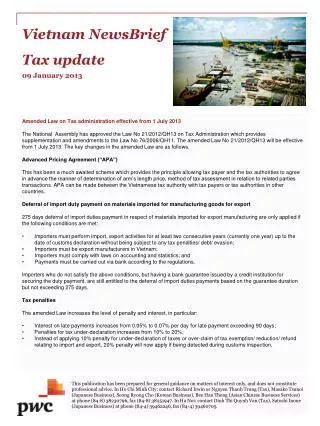

Vietnam New sBri ef Tax update 09 January 2013. Amended Law on Tax administration effective from 1 July 2013

E N D