Download

1 / 50

500 likes | 1.12k Views

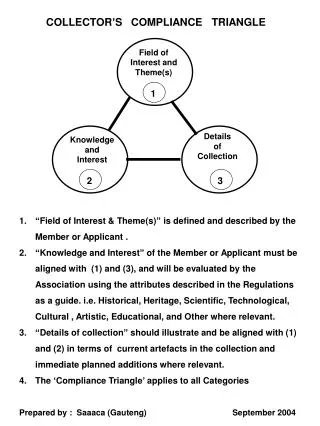

Cooking Up Compliance The Fraud Triangle. Dr. Tony Dimnik and Dr. Pamela Murphy Queen’s School of Business. Agenda. Pamela Murphy Introduction of fraud triangle Tony Dimnik Situational vs. dispositional focus on compliance Motivation Tone at the Top

E N D

Cooking Up ComplianceThe Fraud Triangle Dr. Tony Dimnik and Dr. Pamela Murphy Queen’s School of Business

Agenda • Pamela Murphy • Introduction of fraud triangle • Tony Dimnik • Situational vs. dispositional focus on compliance • Motivation • Tone at the Top • Folly of Rewarding A While Hoping for B • Systems first • Pamela Murphy • Rationalization

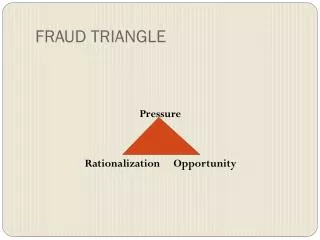

The Fraud Triangle Opportunity Motivation Fraud Attitude / Rationalization

Elements of the Fraud Triangle • Opportunity: • Situations or conditions that allow an individual to commit fraud • Motivation: • Pressures, incentives, and other motivators to commit fraud • A reason to commit fraud • Attitude / Rationalization: • Attitude: a predisposition to commit fraud • Rationalization: a justification for committing fraud

Key Things to Think About… • Systems are necessary but not sufficient in promoting compliance • The environment in which individuals work may be more important than the characteristics of individuals in understanding and promoting compliance • Are situational factors motivating your employees to commit fraud? • Are situational factors allowing employees to rationalize fraud?

Botticelli’s Chart of Hell circa 1480 (also painted Birth of Venus)

Dante’s Inferno circa 1310 Those who commit Violence Those who commit Fraud Traitors

Circle 8 – The FraudulentThose guilty of deliberate, knowing evil • Worse than murderers • Slightly better than traitors if external • No better than traitors if internal

The Lucifer Effect by Philip Zimbardo Social situations often exert much greater power over human actions than has been generally acknowledged by most psychologists or recognized by the general public. This situational approach is a corrective or counterweight to the dominance of the traditional dispositional perspective that has been at the core of Anglo-American psychology. The primary focus on personality and inner determinants of behavior is fueled by the reliance on an individualist orientation, in contrast to a collectivist evaluation that places greater emphasis on the community as the basic unit rather than the person. The Individual is the coin of the operating realm in virtually all of the major Western institutions of medicine, education, law, religion, and psychiatry.

The Lucifer Effect continued These institutions collectively help create the myth that individuals are always in control of their behavior, act from free will, and are thus personally responsible for any and all of their actions…Situational factors are assumed to be little more than a set of minimally relevant extrinsic circumstances…That view seemingly honors the dignity of individuals who should have the inner strength and will power to resist all temptations and situational inducements…We should be aware that a range of apparently simple situational factors could impact our behavior more compellingly than seems possible.

Motivation: Situational Factors • Tone at the Top • Rewards • Systems

Tone at the Top Matters The Chicago Sun-Times Story

Assessing Tone at the Top1992 COSO Control Environment checklist • Existence and implementation of a comprehensive code of conduct and other policies • Codes are periodically acknowledged by all employees • Employees understand what behavior is acceptable or unacceptable and know what to do if they encounter improper behavior • Commitment to integrity and ethics is communicated effectively both in words and deeds • Employees feel pressure to do the right thing • Everyday dealings with customers, suppliers and employees are based on honesty and fairness • Management responds to violations of behavioral standards • The board and audit committee evaluate the effectiveness of tone at the top

Folly of Rewarding A While Hoping for B • Manchester bus service • Moscow opera house • German airline Check the reward system before you blame the individual.

Systems • Allow managers to monitor the organization • Release management time and attention for situational initiatives • How much time do you spend on people? • How much time do you spend on the future? • How much time do you spend on strategy (external issues and organizational design)? Do you have the time to look at the faces of the people who workin your organization?

The Fraud Triangle Opportunity Motivation Fraud Attitude / Rationalization

How Much is Attitude vs. Rationalization? • If opportunity is present, and • If motivation is present, • How much of fraud is due to attitude vs. rationalization?

Are all these people “bad apples”? WorldCom Enron Jeff Skilling Bernie Ebbers Ken Lay Scott Sullivan Adelphia Health South Andy Fastow Tyco Dennis Kozlowski Richard Scrushy John Regis

Were they all “predisposed” to commit fraud? Or Were they able to rationalize it?

My Premise… • Most people are not “predisposed” to commit fraud • Most people have ethical values

My Premise… • Most people are not “predisposed” to commit fraud • Most people have ethical values • If they commit fraud, they will feel guilty • They will use psychological methods of reducing that guilt so they can sleep at night…

The Fraud Triangle Opportunity Motivation Fraud Rationalization

What is Rationalization? • A way of justifying or explaining one’s behavior in a particular situation, while still maintaining one’s beliefs • “I believe that committing fraud is wrong, but I did it in this particular situation because…” • This justification may not be said aloud, but is certainly said to oneself • Eight categories of rationalization

Rationalization Category 1 • Ignore or misconstrue consequences • Minimize, ignore, or misconstrue the consequences of the act

Rationalization Category 1 • Ignore or misconstrue consequences • Minimize, ignore, or misconstrue the consequences of the act “I’m not hurting anyone”

Rationalization Category 2 • Diffusion of responsibility • Obscuring personal agency by diffusing responsibility

Rationalization Category 2 • Diffusion of responsibility • Obscuring personal agency by diffusing responsibility • “Everybody does it” Richard Scrushy, Health South

Rationalization Category 3 • Displacing responsibility • Obscuring personal agency by displacing responsibility

Rationalization Category 3 • Displacing responsibility • Obscuring personal agency by displacing responsibility “We have to hit the numbers” Bernie Ebbers, CEO WorldCom Scott Sullivan, CFO WorldCom

Rationalization Category 4 • Advantageous comparison • By comparing the wrongful act against a much more flagrant act, the original act looks better

Rationalization Category 4 • Advantageous comparison • By comparing the wrongful act against a much more flagrant act, the original act looks better “This is nothing compared to…”

Rationalization Category 5 • Moral justification • Reprehensible acts are reconstrued as socially worthy or having a moral purpose

Rationalization Category 5 • Moral justification • Reprehensible acts are reconstrued as socially worthy or having a moral purpose “I was a hero” Andy Fastow Enron

Rationalization Category 5 • Moral justification • Reprehensible acts are reconstrued as socially worthy or having a moral purpose “I was a hero” Andy Fastow Enron “I’m helping my family…”

Rationalization Category 6 • Euphemistic labeling • Using convoluted verbiage to make a wrongful act sound better

Rationalization Category 6 • Euphemistic labeling • Using convoluted verbiage to make a wrongful act sound better “I’m trying to level the playing field”

Rationalization Categories 7 and 8 • Dehumanize the victim • Attribute blame to the victim

Rationalization Categories 7 and 8 • Dehumanize the victim • Attribute blame to the victim “The company had it coming” “The company treated me unfairly, they deserve it” “Company executives get all the perks”

Category 9? • Postponement • Try not to think about it Does this work?

Category 9? • Postponement • Try not to think about it…along with… • Self affirmation • Do or say something that makes one feel better about oneself

Category 9? • Postponement • Try not to think about it…along with… • Self affirmation • Do or say something that makes one feel better about oneself Bernie Ebbers WorldCom John Rigas Adelphia Dennis Kozlowski Tyco

So What? • Have you heard any of these rationalizations within your organization? • Do you believe individuals are capable of both: • altruistic behavior • fraudulent behavior?

So What?? • Ethical decision making is often based in emotion • Most people are not predisposed to commit fraud, but virtually everyone can rationalize • By knowing typical rationalizations: • Make employees aware of the flaws of typical rationalizations • In my experiments, misreporting rates dropped by more than 20% when participants were reminded of flaws in rationalizations • Be aware of and probe for rationalizations from employees

So What?? Understanding institutional and environmental situations are essential to reduce the motivation to commit fraud Motivation Opportunity Fraud Attitude / Rationalization

So What?? Understanding rationalization helps detect fraud more quickly and may prevent fraud Motivation Opportunity Fraud Attitude / Rationalization

So What?? • Systems are essential to reduce the opportunity to commit fraud • Microsoft compliance solutions can help you reduce this opportunity Motivation Opportunity Fraud Attitude / Rationalization

Moving Forward Begin thinking about how to action some of the ideas shared today by engaging in a complimentary half-day workshop with a corporate governance, risk and compliance consultancy & technology partner. To arrange your workshop, please contact your sales rep or Sujan Menezes Industry Manager - Financial Services sujanm@microsoft.com Today’s presentation will be made available at www.microsoft.ca/improvecompliance