Download

1 / 35

350 likes | 551 Views

Investment Appraisal (Discounted Cash Flow and NPV) by Binam Ghimire. Objectives. To implement NPV for investment decisions . Making Capital Investment Decisions. Here, we make discussions related with discounted cash flows and NPV technique for investment appraisal. . Net Cash Flows.

E N D

Investment Appraisal (Discounted Cash Flow and NPV) by Binam Ghimire

Objectives • To implement NPV for investment decisions

Making Capital Investment Decisions • Here, we make discussions related with discounted cash flows and NPV technique for investment appraisal.

Net Cash Flows • Net Cash Flows = Revenue – Costs – Investments • Net Cash Flows are used as a basis for evaluating potential investment projects using the NPV technique • For the project it is net relevant cash flow

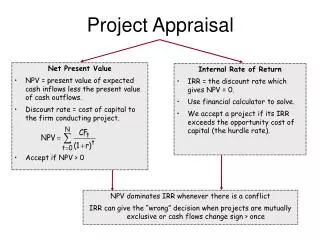

NPV and Investment Appraisal • NPV leads to better investment decisions • Discounted Free cash flows are totalled to provide the NPV of the project and the project with positive NPV is accepted • The above would require • Estimation of cash flows for the project • Estimation of Cost of Capital

Investment appraisal Estimation of cash flows for the project

Estimation of Cash Flows for the project • What to estimate? • Cash flows that will occur or • Brealey and Myers (1996, p. 113) put it in the context of “What to Discount “ and authors have mentioned: • Only cash flow is relevant • Always estimate cash flows on an incremental basis • Be consistent in your treatment of inflation

Estimation of Cash Flows for the project • Estimate actual Cash Flows that will occur • Use the simple counting concept of money coming in and going out. • Not like an accountant (e.g. in case of capital expenses. Depreciation charged from Profit and Loss account. Depreciation is not a cash flow). • Record when occurred as IN and OUT. (e.g. taxes should be discounted from their actual payment date, not from the time when the tax liability is recorded in the firm’s books).

Estimation of Cash Flows for the project • Example: • Best Food Plc paid £10 million in cash for a restaurant chain as part of new investment project of 20 years. • The accounting concept will charge £500,000 this year and remaining £9.5 million over the next 19 years if the depreciation is straight line. • Note that for investment appraisal, the relevant cash outflow is the full £10 million in year 0, different than only £500,000 of accounting concept. • Cash Flows that occur may be divided into: Investment related cash flows and incremental cash flows

Estimation of Cash Flows for the project • Investment related cash flows • Installation costs • Opportunity costs • Sunk costs • Working capital

Estimation of Cash Flows for the project • Installation costs: shipping and installation charges, electrical work required to put the machine in working condition • Opportunity costs: • Best Food Plc considers use of land purchased 10 years ago at £100,000. The market value of the land now is £300,000. • Should the company consider the value of the land as investment cost? Which value should be considered? The book value or the market?

Estimation of Cash Flows for the project • Sunk Costs: spilled milk. • Cost that the company has already incurred but that has no current or future value. • Example: Best Food Plc paid £20,000 to install fence in a land. Now it is considering to make a building on the land for a new restaurant. Unfortunately the fence must be removed before construction begins. By including the £20,000 already spent for the fence in the cost of the project we commit the sunk cost fallacy.

Estimation of Cash Flows for the project • Discussion: As part of evaluation of a new fast food item Best Food Plc had made a test marketing in which they spent £1.0 million last year. Best Food Plc is now evaluating the NPV of new restaurant in ten major cities of the world where they will sale this food which was liked by people during the test marketing. • Question: Is the cost of test marketing relevant for the capital budgeting decision now?

Estimation of Cash Flows for the project • No • The cost of £1.0 million is not recoverable • The decision to spend £1.0 million was a capital budgeting decision in itself • Once the company incurred the expense, the cost became irrelevant for any future decision.

Estimation of Cash Flows for the project • Working Capital: By accepting a project you may require investment in working capital say inventories. When the project is over you would expect the working capital to be released i.e. all inventory sold.

Estimation of Cash Flows for the project • Assuming the firm will invest in working capital for the duration of the project, you would keep it as cash outflow in the beginning and as inflow in the end. Remember the cash inflow from recapturing the working capital investment is not taxed. WC WC 0 n Time

Estimation of Cash Flows for the project • Incremental Cash flows • Principle: In investment appraisal we should only include the extra income/ expenses that would result from the project • You would not pay big money for an old cow regardless of how much milk it gave in the past. You would prefer a relatively young one who will give you milk for some time in the future i.e. Incremental is important and not average.

Estimation of Cash Flows for the project • Allocated Costs • A particular expenditure may benefit a number of projects. Accountants allocate this cost across the different projects when determining income. • For example overhead costs such as rent, salaries, light, heat may not be related to a particular project but to be paid. When accountant assigns costs to the project a charge for the overhead is usually made. • In capital budgeting, we should be cautious that the allocation of overheads represents the true extra expenses that would be incurred for the project. • Such a cost should be viewed as a cash outflow only if is an incremental cost of the project

Estimation of Cash Flows for the project • Side Effects: A difficulty in determining incremental cash flows comes from the side effects of the proposed project on other parts of the firm. A side effect is classified as either erosion or synergy. • Erosion occurs when a new product reduces the sales and, hence, the cash flows, of existing products. • Synergy occurs when a new project increases the cash flows of existing projects

Estimation of Cash Flows for the project • Erosion Example: • Best Food Plc introduced new ice cream, the Vanilla and Tropical Fruits Ice Cream (VATFIC). Calculated NPV of the VATFIC project is £100 million. • However, it is learnt that half of the VATFIC customers are again customers of Best Food Plc who are currently buying Vanilla and Summer Fruit Ice Cream (VASFIC). • This means the sales of VASFIC will go down by 50 percent. • If lost VASFIC sales has an NPV of - £200 million then the true NPV is not £100 million but -£100 million (-£200 + £100)

Estimation of Cash Flows for the project • Synergy Example: • Best Food Plc is contemplating to invest in a green environment project which has a NPV of -£10 million. • However, it is learnt that this will create greater publicity for all Best Food products. It is estimated that the increase in cash flow elsewhere in the restaurant has a PV of £35 million. • Assuming that the estimates of the synergy is trustworthy, the net present value of the green environment project will be £15 million • Best Food should invest in the green environment project

Estimation of Cash Flows for the project • Select the appropriate for the followings from- Do not, Include, Forget, Beware • ………….confuse average with incremental • …………. all incidental effects • …………. sunk costs • ………….opportunity Costs • …………. forget investment in Working Capital • …………. shutdown Cash Flows • …………..of allocated Overhead Costs • …………. incidental cash flows

Estimation of Cash Flows for the project • Select the appropriate for the followings from- Do not, Include, Forget, Beware • Do not confuse average with incremental • Include all incidental effects • Forget sunk costs • Include opportunity Costs • Do not forget investment in Working Capital • Include shutdown Cash Flows • Beware of allocated Overhead Costs • Include all incidental cash flows

Estimation of Cash Flows for the project: Dealing with inflation • Note that cash flows are affected by the level of inflation in the country • Generally, the rate of interest quoted in the market are nominal interest rate which does not take into consideration the effect of price changes. The real interest rate can be calculated using the formula:

Estimation of Cash Flows for the project: Dealing with inflation • Example: The real cost of capital of a company is 8%. The general price level is increasing by 6.5%. What is the cost of capital that you would use to discount the free cash flow? • Cost of capital: 1+8% = 1+ k% / 1+ 6.5% • Therefore the nominal rate of interest (the cost of capital) is 15%.

Estimation of Cash Flows for the project: Dealing with inflation • Note we converted real into nominal. • Here we had two choices 1. Real Method 2. Nominal Method • Real Method: Do not inflate the cash flows (leave in real terms) then discount using the real rate • Nominal Method: inflate each cash flow by its specific inflation rate (convert into money terms) then discount using money rate • Discounting real payment by real interest rate and Nominal Payment by Nominal interest rate will always give the same answer. We must not mix up real and nominal

Estimation of Cash Flows for the project: Dealing with taxation • Operating Cash Inflows taxed at Corporation Tax Rate • Operating Cash Outflows are tax deductable (tax relief) • Tax is paid on the same year (If not mentioned) • Investment spending attracts Capital or Writing down allowances (i.e. depreciation) • The scrap value may create a balancing allowance or charges

Estimation of Cash Flows for the project: Dealing with taxation • Example: Cost of machine £10,000 which will be used on a project for four years. Corporate tax is 30% payable one year in arrears and capital allowance is 25% diminishing balance. Calculate the tax savings.

Estimation of Cash Flows for the project: Dealing with taxation • Solution

Investment appraisal Estimation of Cost of Capital

Project appraisal: Estimation of cost of capital • We can use the WACC as a discount rate in project appraisal. • However the new project should have the same level of business risk as the existing operations. • Undertaking the new project will not alter the firm’s gearing (financial risk) • If the above two do not apply then alternative methods should be applied.

Project appraisal • WACC, Risk Adjusted WACC and APV

Example • A company invests £30,000 in a project that will yield cash flows of £10,000 per annum for 3 years before tax. Written Down Allowances are given at 25% and corporation tax is 30%. The cost of capital is 8%. The residual value at the end of the project is expected to be £10,000. • Calculate the NPV of the project.

Case Study • Case Study – iPhoneMind and iPhone5 • Case Study – The Baldwin Company • Practice exercises : Discounted Cash Flow Techniques and use of NPV