Download

1 / 42

440 likes | 622 Views

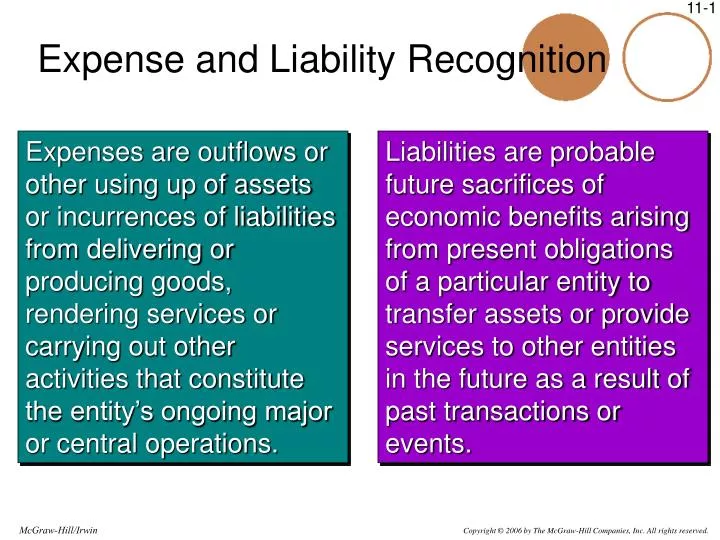

Expense and Liability Recognition. Expenses are outflows or other using up of assets or incurrences of liabilities from delivering or producing goods, rendering services or carrying out other activities that constitute the entity’s ongoing major or central operations.

E N D

Expense and Liability Recognition Expenses are outflows or other using up of assets or incurrences of liabilities from delivering or producing goods, rendering services or carrying out other activities that constitute the entity’s ongoing major or central operations. Liabilities are probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events.

Vendor Overview of the Purchasing Process A purchase transaction usually begins with a purchase requisition generated by the user department. The purchasing department prepares a purchase order that is sent to the vendor. When the goods are received or the services rendered, a liability is recorded. Finally, the entity pays the vendor. Receivingreport and liability recorded Purchase order Purchase requisition

Types of Transactions and Financial Statement Accounts Affected • There are three types of transactions: • Purchase of goods and services for cash or credit. • Payment of the liabilities arising from such purchases. • Return of goods to suppliers for cash or credit.

Types of Transactions and Financial Statement Accounts Affected

Purchaseorder(4 part) Flowchart of the Purchasing Process – EarthWear Clothiers Department Requesting Purchasing IT Approved purchaserequisition received Accountspayablemaster file Purchaserequisition Purchaseorder file Purchaseorder program Input Vendor Errorcorrections Errorreport A/P Receiving PO #2 Filed Numer-ically Purchasing

Flowchart of the Purchasing Process – EarthWear Clothiers Department Receiving Accounts Payable (A/P) PO #1 PO #3 Compare invoiceto PO and RR Reviewaccountdistribution Receivingreport Goodsreceived,counted, andinspected Vendorinvoice Voucherpacket Enter vendor, quantity, andPO # Receivingreport (RR) To IT Input Errorcorrection From IT Dailyreceiving log

Flowchart of the Purchasing Process – EarthWear Clothiers Department IT Purchase order file A/P master file General ledger file Open PO report A/P expensedistribution report Accounts payableupdate Monthlyreports Weekly Monthly Inputfrom A/P A/P reporting Voucher register Cash disbursementsjournal Daily A/P listing Errorreport Report to A/P Cashdisbursementreport Daily Generalledger

Checks Checks Checks Flowchart of the Purchasing Process – EarthWear Clothiers Department Accounts Payable (A/P) IT Cashier Cashdisbursementreport A/P master file Cashdisbursementprogram Review checksand mail tovendors Review documentsand authorize payment Cashdisbursementreport Input To Vendors

Types of Documents and Records • Purchasing documents and records . . . • Purchase Requisition – request to purchase goods or services. • Purchase Order – includes description, quality, and quantity or goods or services being purchased. • Receiving Report – records the receipt of goods. • Vendor Invoice – the bill from the vendor. • Voucher – serves as the basis for recording a vendor’s invoice. • Voucher Register – used to record vouchers for goods and services. • Accounts Payable Subsidiary Ledger – includes amount owed to individual vendors. • Vendor Statement – represents the purchase activity with vendor. • Check – pays for goods or services. • Check Register – contains columns to record credits to cash and debits to accounts payable and cash discounts.

Inherent Risk Assessment Industry-Related Factors 1.Is the supply of rawmaterials adequate? 2.How volatile areraw materialprices?

Inherent Risk Assessment Misstatements Detected in Prior Audits Generally, the purchasing process is not difficult to audit and does not present contentious accounting issues. However, the auditor’s experience in past audits must be considered when assessing inherent risk.

Planning and performing tests of controls of purchase transactions. Setting and documenting the control risk for the purchasing process. Control Risk Assessment Major steps in setting the control risk in the purchasing process. Understanding and documenting the purchasing process based on a reliance strategy.

For each major class of transactions in the purchasing process, the auditor must obtain the following information: • How purchase, cash disbursements, and purchase return transactions are initiated. • The accounting records, supporting documents, and accounts involved in processing purchases, cash disbursements, and purchase returns. • The flow of each type of transaction from initiation to inclusion in the financial statements, including computer processing. • The process used to estimate accrued liabilities. Control Risk Assessment Information Systems and Communication

Control Risk Assessment After testing controls, the auditor sets the level of control risk. When tests of controls support the planned level of control risk, no modifications are necessary to detection risk. The auditor may proceed with the substantive procedures as planned. When test do not support the planned control risk, the auditor lowers the level of detection risk leading to more substantive procedures.

Control Procedures and Tests of Controls – Purchase Transactions Assertions about Classes of Transactions and Events for the Period under Audit

Control Procedures and Tests of Controls – Purchase Transactions

Control Procedures and Tests of Controls – Cash Disbursement Transactions Occurrence of Cash Disbursement Transactions The auditor is concerned with a misstatement caused by a cash disbursement being recorded in the client’s record when no payment was made. The primary control procedures to prevent such misstatements include proper segregation of duties, independent reconciliation and review of vendor statements, and monthly bank reconciliations.

Control Procedures and Tests of Controls – Cash Disbursement Transactions Completeness of Cash Disbursement Transactions The major audit concern is that a cash disbursement is made but not recorded in the records. The auditor should account for the numerical sequence of checks and reconcile the daily cash disbursements with posting to the accounts payable subsidiary records.

Control Procedures and Tests of Controls – Cash Disbursement Transactions Authorization of Cash Disbursement Transactions Proper segregation of duties reduces the likelihood that unauthorized cash disbursements are made. The individual who approves a purchase should not have direct access to the cash disbursement.

Control Procedures and Tests of Controls – Cash Disbursement Transactions Accuracy of Cash Disbursement Transactions One of the major audit concerns is that the payment amount is recorded incorrectly. To detect such an error, client personnel should reconcile the total of the checks issued each day with the daily cash disbursements report.

Control Procedures and Tests of Controls – Cash Disbursement Transactions Cutoff of Cash Disbursement Transactions The auditor’s tests of controls include reviewing the reconciliation of checks with postings to the cash disbursements journal and accounts payable subsidiary records. The auditor also tests cash disbursements before and after year-end to ensure that transactions are recorded in the proper period.

Control Procedures and Tests of Controls – Cash Disbursement Transactions Classification of Cash Disbursement Transactions The auditor is concerned that a cash disbursement may be charged to the wrong general ledger account. The use of a chart of accounts, as well as independent approval and review of the account code on the voucher should provide adequate control.

Control Procedures and Tests of Controls – Purchase Return Transactions Generally, the number and magnitude of purchase return transactions are not material. The auditor normally does not test controls relating to purchase returns. Substantive testing is used to test the reasonableness of the amount.

Relating the Assessed Level of Control Risk to Substantive Procedures If the results of the tests of controls support the achieved level of control risk, the auditor conducts substantive procedures at the planned level. If the results do not support the achieved level of control risk, the auditor reduces the detection risk, which will increase substantive procedures.

Auditing Accounts Payable and Accrued Expenses Substantive Analytical Procedures

Tests of Details of Transactions, Account Balances, and Disclosures Completeness Obtain a listing of accounts payable, foot the listing, and agree it to the general ledger control account. Selected vouchers or vendor accounts should be traced to the supporting documents or subsidiary accounts payable records to verify the accuracy of the details.

The auditor should conduct a test for unrecorded liabilities that include the following procedures: • Ask management about control procedures used to identify unrecorded liabilities at the end of the period. • Obtain copies of vendors’ monthly statements and reconcile the amounts to the client’s accounts payable records. • Confirm vendor accounts, including accounts with small or zero balances. • Vouch large-dollar items from the purchases journal and cash disbursements journal for a limited time after year-end. • Examine the files of unmatched purchase orders, receiving reports, and vendor invoices for any unrecorded liabilities. Tests of Details of Transactions, Account Balances, and Disclosures Completeness

Tests of Details of Transactions, Account Balances, and Disclosures Existence The auditor’s major concern is whether the recorded liabilities are valid obligations of the entity. The auditor should vouch a sample of items on the listing of accounts payable to other supporting documents.

Tests of Details of Transactions, Account Balances, and Disclosures Cutoff The auditor attempts to determine if all purchase transactions are recorded in the proper period. On most audits, the purchase cutoff is coordinated with the client’s physical inventory count. Proper cutoff should also be determined for purchase return transactions.

Tests of Details of Transactions, Account Balances, and Disclosures Rights and Obligations There is little risk related to this assertion because clients seldom have an incentive to record liabilities that are not obligations of the entity.

Tests of Details of Transactions, Account Balances, and Disclosures Valuation Accounts payable are recorded at either the gross amount of the invoice or net of cash discount amount. The valuation of accruals depends upon the type and nature of the accrued expense. Most accruals are relatively easy to value.

Tests of Details of Transactions, Account Balances, and Disclosures Classification, Presentation, and Disclosure • Major classification issues include . . . • Identifying and reclassifying any material debits contained in accounts payable. • Segregating short-term and long-term payables. • Ensuring that different types of payables are properly classified.

Tests of Details of Transactions, Account Balances, and Disclosures Disclosure Items for the Purchasing Process Payables by type (trade, employees, etc.). Purchases from and payables to related parties. Dependence on a single vendor or a small number of vendors. Short- and long-term payables. Long-term purchase contracts, including any unusual purchase commitments. Costs by reportable segment of the business.

Tests of Details of Transactions, Account Balances, and Disclosures Other Presentation Disclosure Assertion The auditor must ensure that all related party transactions have been identified. When the client has entered into formal long-term purchase contracts, adequate disclosure of the terms must be made.

Accounts Payable Confirmation Accounts payable confirmations are used less often than accounts receivable confirmations. The auditor is able to examine externally created source documents relating to accounts payable. When confirmations are used they are usually positive and referred to as blank confirmations. The vendor is asked to supply the balance owed by the client.

Evaluating the Audit Findings All identified misstatements should be aggregated. The likely misstatement is then compared to tolerable misstatement. If the likely misstatement is less than the tolerable misstatement, the auditor has evidence that the account is fairly presented. Conversely, it the likely misstatement exceeds the tolerable, the auditor should conclude that the account is not fairly presented.