Download

1 / 24

240 likes | 448 Views

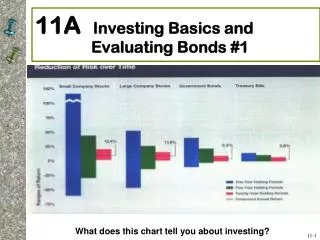

11A Investing Basics and Evaluating Bonds #1. What does this chart tell you about investing?. 11- 1. Why People Invest. To achieve financial goals, such as the purchase of a new car, a down payment on a home, or paying for a child’s education. To increase current income.

E N D

11A Investing Basics and Evaluating Bonds #1 What does this chart tell you about investing? 11-1

Why People Invest • To achieve financial goals, such as the purchase of a new car, a down payment on a home, or paying for a child’s education. • To increase current income. • To gain wealth and a feeling of financial security. • To have funds available during retirement years.

Objective 1Explain Why You Should Establish an Investment Program Establishing Investment Goals • Financial goals should be: • Specific • Measurable • Tailored to your financial needs • Aimed at what you want to accomplish • Financial goals should be the driving force behind your investment plan 11-3

Establishing Investment Goals • What will you use the money for? • How much money do you need to satisfy your investment goals? • How will you obtain the money? • How long will it take you to obtain the money? • How much risk are you willing to assume in an investment program? • What possible economic or personal conditions could alter your investment goals? • Considering your economic circumstances, are your investment goals reasonable? • Are you willing to make the sacrifices necessary to ensure that you meet your investment goals? • What will the consequences be if you don’t reachyour investment goals? 11-4

Performing a Financial Checkup • Work to balance your budget • Do you regularly spend more than you make? • Pay off high interest credit card debt first • Obtain adequate insurance protection • Start an emergency fund you can access quickly • Three months of living expenses • Have access to other sources of cash for emergencies • Pre-approved line of credit • Cash advance on your credit card 11-5

Surviving a Financial Crisis • Establish a larger than usual emergency fund • Know what you owe • Identify debts that must be paid • Reduce spending • Pay off credit cards • Apply for a line of credit at your bank, credit union, or financial institution • Notify credit card companies and lenders if you are unable to make payments • Monitor the value of your investment and retirement accounts 11-6

Getting the Money Needed to Start an Investing Program • Pay yourself first • Take advantage of employer-sponsored retirement programs • Participate in elective savings programs • Make a special savings effort one or two months each year • Take advantage of gifts, inheritances, and windfalls 11-7

The Value of Long-Term Investing Programs • Even small amounts invested regularly grow over a long period of time • If you begin saving $2,000 each year. depending on the rate of return, you could have over $1 million by the time you are age 65 (See Exhibit 11-1 on page 356) • The higher the rate of return, the greater the investment risk 11-8

Objective 2Describe How Safety, Risk, Income, Growth, and Liquidity Affect Your Investment Decisions Factors Affecting the Choice of Investments • Safety and risk • Risk = uncertainty about the outcome • Investment Safety = minimal risk of loss • Risk-Return Trade-Off • The potential return on any investment should be directly related to the risk the investor assumes • Speculative investments are high risk, made by those seeking a large profit in a short time 11-9

Components of the Risk Factor • Inflation Risk during periods of high inflation, your investment return may not keep pace with inflation; lose purchasing power • Interest Rate Risk the value of bonds or preferred stock may increase or decrease with changes in interest rates • Business Failure Risk affects stocks and corporate bonds(when business is not profitable) • Market Risk the risk of being in the market versus in a risk-free asset (stocks follow market cycle) 11-10

Investment Income, Growth and Liquidity • Investment Income • A predictable source of income (dividends or interest) • Most conservative = passbook savings, CDs and government securities • Other choices: • Municipal and corporate bonds • Preferred stock • Utility stocks • Selected common stocks • Selected Mutual funds • Rental real estate 11-11

Investment Income, Growth and Liquidity • Investment Growth • Growth in value (price appreciation) • Common stock usually offers the greatest potential for growth • Mutual funds and real estate offer growth potential • Investment Liquidity • 2 Dimensions: • Ability to buy or sell investment quickly • Without substantially affecting the investment’s value • Bank accounts VERY liquid; CDs have penalties; stocks and bonds could lose money upon sale 11-12

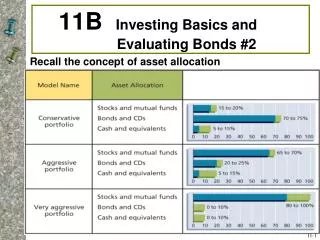

Objective 3Identify the Factors That Can Reduce Investment Risk Asset Allocation = The process of spreading your assets among several different types of investments (choose % weightings in each) • The ratio of stocks, bonds, cash assets, other securities in your portfolio(Conservative, Moderate, Aggressive portfolios with different asset weights: conservative portfolio = less stock) • Most important determinant of overall investment success = Diversification (“eggs in different baskets”) 11-14

Portfolio Management & Asset Allocation Other Factors to Consider: • Your Tolerance for Risk • At what point can you no longer sleep easily? • See http://njaes.rutgers.edu/money/riskquiz/ • Your Investment Time Horizon • When will you need the money? • How long can your money continue to grow? • Your Age • Growth vs. income (olderpeople more conservative) • Recovery time if investments nosedive • One guideline: 110 – age = % of portfolio in stock 11-15

Your Role in the Investment Process • Evaluate potential Investments • Monitor the value of your investments • Keep accurate records • Other factors • Seek help from personal financial planner • Consider the tax consequences of selling investments 11-16

Objective 4Understand Why Investors Purchase Government Bonds • Government bonds = written pledge to: • Repay a specified sum of money (face value) • At maturity • Along with periodic interest (coupon payments) • Sold to fund the national debt and the ongoing costs of government • Three levels of government issues: • Federal • State • Local municipalities 11-17

U.S. Treasury Bills, Notes and Bonds Treasury Bills (T-Bills) • $100 minimum • 4, 13, 26 and 52 weeks to maturity • Sold at a discount • Federal, but no state, tax on interest earned • “Reciprocal immunity” doctrine Treasury Notes • $100 units • Typical maturities = 2, 3, 5, 7, and 10 years • Interest paid every six months • Higher rate than T-bills (Why?) • Federal, but no state, tax on interest earned 11-18

U.S. Treasury Bills, Notes and Bonds Treasury Bonds • Issued in minimum units of $100 • 30 year maturity dates • Interest rates higher than Treasury notes & bills • Interest paid every six months Treasury Inflation-Protected Securities (TIPS) • Sold in minimum units of $100 • Sold with 5, 10 or 20 year maturities • Principal changes with inflation (measured by CPI) • Pays interest twice a year at a fixed rate 11-19

Federal Agency Debt Issues • Essentially risk free • Slightly higher interest rates than Treasury securities (Why?) • Minimum investment may be as high as $10,000 to $25,000 • Maturities range from 1 – 30 years • Average maturity = 12 years • Issuing agencies sample: • Fannie Mae • Freddie Mac • GNMA • TVA 11-20

State and Local Government Securities Municipal Bonds (“Munis”) • Issued by a state or local government • Cities • Counties • School districts • Special taxing districts • Funds used for ongoing costs and to build major projects such as schools, airports, and bridges • General Obligation Bonds • Backed by the full faith, credit and taxing authority of the issuing state or local government • Revenue Bonds • Repaid from money generated by the project the funds finance, such as a toll bridge 11-21

State and Local Government Securities Municipal Bonds (“Munis”) • Key characteristics: • Interest exempt from federal taxes • Capital gains may NOT be tax exempt • Usually exempt from state and local taxes in state where issued • Exempt status determined by use of funds • Lower rate of return than on taxable bonds • Insured municipal bonds • Private insurance to reduce risk 11-22

Taxable Equivalent Yield Formula Used to compare tax-exempt and taxable bonds 11-23

Wrap Up • Concept Check 11-1- Why Develop Specific Investment Goals? Why Participate in Employer Retirement Savings Plan? How the TVoM Affects Investing. • Exhibit 11-2- A Quick Test to Measure Investment Risk • Concept Check 11-2- Four Components of Risk • Concept Check 11-4- Taxable Equivalent Yields