Download

1 / 14

150 likes | 277 Views

GSTT in a nutshell The GSTT is levied, in addition to any gift or estate taxes that apply to the transfer On the value of any life insurance (and/or any other property) Transferred during lifetime or at death without adequate consideration

E N D

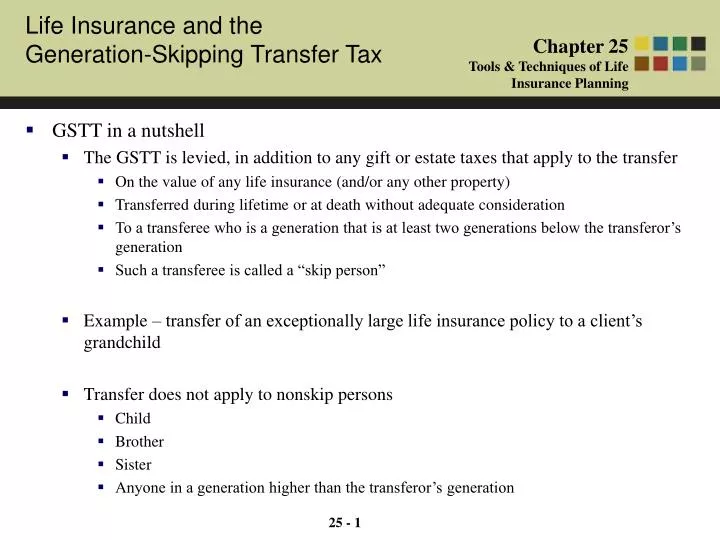

GSTT in a nutshell • The GSTT is levied, in addition to any gift or estate taxes that apply to the transfer • On the value of any life insurance (and/or any other property) • Transferred during lifetime or at death without adequate consideration • To a transferee who is a generation that is at least two generations below the transferor’s generation • Such a transferee is called a “skip person” • Example – transfer of an exceptionally large life insurance policy to a client’s grandchild • Transfer does not apply to nonskip persons • Child • Brother • Sister • Anyone in a generation higher than the transferor’s generation

GSTT in a nutshell (cont’d) • GSTT is imposed as a flat tax at the highest federal estate tax level • 45% in 2008 • GSTT annual exclusion • $12,000 (in 2008) per donee annual exclusion for transfers to skip persons • Double by splitting gifts with spouse • Transfers to a trust may qualify • All trust beneficiaries must be skip persons • No distribution can ever be made to a nonskip person • Each skip person’s share is held in an account separate from the others

GSTT annual exclusions (cont’d) • Leverage the annual exclusion • Irrevocable life insurance trust • Split dollar • Survivorship life insurance • Downsides to qualifying for the GSTT annual exclusion • If the beneficiary dies before the client-grantor, trust includable in beneficiary’s estate • Crummey power techniques, such as the hanging power, will not qualify for the annual exclusion • Exclusion requires dispositive rigidity (separate trusts required) • Trust cannot provide financial security for intervening skipped generation

GSTT exemption • $2,000,000 (in 2008) exemption per transferor • Can allocate to transfers during lifetime or at death • Can effectively double to $4,000,000 by splitting gifts with spouse • Triggering the GSTT • Direct skip • Occurs when a transfer subject to gift or estate tax is made to a skip person • For this purpose, a trust is treated as a skip person if all trust beneficiaries are skip persons • Examples • Client gives life insurance policy to grandchild • Client transfers life insurance policy to ILIT for grandchildren and great-grandchildren • Client dies owning life insurance and proceeds are paid to grandchild

Triggering the GSTT (cont’d) • Taxable termination • Occurs when there are no more nonskip persons ahead of the skip person • Transfer is assumed to occur at the moment nothing stands between the skip person and the transferred cash or other asset • Example • Client creates a life insurance trust that provides “Income from this trust is to be paid to my three children for life. At the death of the last survivor, principal is to be distributed to my six grandchildren” • When the last nonskip person’s (children’s) interest terminates (in this example, by death), the property in the trust is subject to the GSTT

Triggering the GSTT (cont’d) • Taxable distribution • Occurs when either income or principal is distributed from a trust to a skip person • Such distributions can occur while the nonskip persons are alive • Computing the taxable amount • Direct skip • Amount subject to the GSTT is equal to the value of the transfer reduced first by the estate tax imposed on it • Example • $2,000,000 transfer, 45% estate tax bracket • GSTT would be imposed on the $1,100,000 left after the federal estate tax of $900,000 was taken.

Computing the taxable amount (cont’d) • Taxable termination • Amount on which the tax is computed is the value of the property to which the termination pertains • Example • Client dies and $2,000,000 in policy proceeds are paid to a trust providing income to the client’s son for life. Client in 45% estate tax bracket. $1,100,000 remains after estate tax of $900,000. • At the son’s death, the remainder (assumed to remain constant) is to be paid to the client’s grandson • GSTT would be 45% of $1,100,000, or $495,000

Computing the taxable amount (cont’d) • Taxable Distribution • Amount on which the tax is computed is the value of the property the transferee receives. • Example • Client dies and $2,000,000 in policy proceeds are paid to a trust that can sprinkle or spray principal to the client’s son or grandson, or both. Client is in the 45% estate tax bracket. • The federal estate tax would be $900,000 (45% of $2,000,000), leaving $1,100,000 in the trust • Trustee immediately distributes $1,100,000 to the grandson • GSTT would be 45% of $1,100,000, or $495,000

Amount of exemption 1- Total value of transfer 150,000 1- 1,500,000 • Computing the taxable amount (cont’d) • Inclusion ratio • The amount of a generation-skipping transfer that is subject to the GSTT is found through an inclusion ratio • Example • Value of gift = $1,500,000 • Client had only $150,000 of his $2,000,000 exemption available • Inclusion ratio would be .900

Computing the taxable amount (cont’d) • Inclusion ratio (cont’d) • Leverage implications with respect to cash to irrevocable life insurance trusts • Once the exemption shields a gift of life insurance premiums or a gift of a life insurance policy, the proceeds generated by those projected premiums or policy will not be subject to the GSTT when paid out • Example • Irrevocable life insurance trust purchases a $20,000,000 policy on the client’s life. • Over the next 10 years, client pays $100,000 each year in premiums towards that policy. • Client allocates GST exemption against each premium. • None of the $20,000,000 proceeds would be subject to the GSST

Reverse QTIP Election • QTIP Trust • Obtaining a marital deduction for property that is not left outright to a spouse • Client can provide income to a spouse for life, but at the spouse’s death, the client can be sure it will pass to the person or persons the client has selected • Whatever remains in the trust at the spouse’s death must be included in the spouse’s estate as if the spouse had transferred the property • This same fiction applies for GSTT purposes. The surviving spouse is treated as the transferor of property really transferred by the client. • This might cause a portion or all of the client’s GSTT exemption to be wasted

Reverse Q-tip Election (cont’d) • With a reverse QTIP election, the first spouse to die will be treated as the transferor of reverse QTIP property for GSTT purposes. Therefore, that spouse’s GSTT exemption can be allocated to the reverse QTIP property. • Example • Husband dies leaving $4,000,000 of life insurance (the entire estate) in 2007 • Previous gifts of $500,000 made using his unified credit • $1,500,000 passed into a credit equivalent bypass trust for his 5 children and their 5 children • Balance of proceeds ($2,500,000) was paid into a QTIP trust for his wife • Executor allocates $1,500,000 of husband’s GST exemption to CEBT and $500,000 to reverse QTIP trust (QTIP trust is split) • Husband is able to use all of his $2,000,000 exemption • Wife can allocate her $2,000,000 exemption to QTIP trust • Full $4,000,000 is exempt from GSTT • No federal estate tax payable on husband’s death

GSTT and irrevocable life insurance trusts (ILITs) • Transfers to ILITs are potentially subject to GSTT • Three ways to utilize the GSTT exemption with an ILIT • Use it immediately • Allocate the exemption to (a) the gift of the policy itself and (b) premium payments • Wait until the client dies • Use the exemption against the much larger insurance proceeds • Wait until the client dies • Use the GSTT exemption to shelter transfers of other estate assets • It is the timely and creative use of the GSTT exemption coupled with life insurance that is the key to maximizing the exemption

GSTT and irrevocable life insurance trusts (ILITs) (cont’d) • Costs to using the exemption to shelter premium payments • The GSTT exemption is not available to avoid the tax on other transfers to skip persons • The client will have to file annual tax returns claiming the exemption • Opportunity cost. Exemption could be wasted if allocated to ILIT and ILIT later turns out to not be generation-skipping.