Download

1 / 25

250 likes | 399 Views

Midterm!! . Wednesday March 19 Midterm question sheet: 12 total questions I added 3 to the original file 70-80% of the test will be from these questions The rest will be from short answer questions Closed book/notes/internet/text/email/chat test – just you and the test

E N D

Midterm!! • Wednesday March 19 • Midterm question sheet: • 12 total questions • I added 3 to the original file • 70-80% of the test will be from these questions • The rest will be from short answer questions • Closed book/notes/internet/text/email/chat test – just you and the test • Can either hand write, or type on your laptop • Econ is fun!

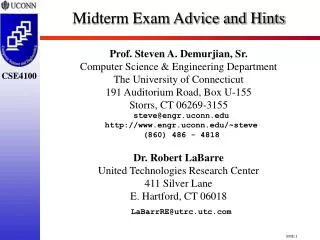

Revisiting Adverse Selection in Insurance $ Demand MC P AC Qeq Qmax

Takeaways from the graph • Even with adverse selection, the market could still function – though not necessarily efficiently • But a “death spiral” is possible • The mandate penalty will induce some but not all to participate • The more risk averse the population is, the less adverse selection will occur • Young invincibles – tend to be both below average users and less risk averse • Lowering admin costs lowers improves efficiency of market

Now back to today’s lecture! • The Role of the Employer in Insurance Markets

Employer Provision of Insurance • About half of the US population receives insurance through their employer • Currently about 45% of expenditures are publicly funded while 55% privately funded. • In 1980 public funds accounted for 40% • Out of pocket payments have declined: • 1970=36.9% of healthcare consumption • 2000=15.6% • 2010=12.2%, 2012=12.5%. • Most of this has gone into insurance premiums

Role of the Employer • No other country really has the mix of public and private coverage. How did this occur? • Great Depression – Blues • WWII wage and price controls • IRS ruled benefits not part of taxable income (about $210 billion) • Basically all this was an accident • But had some good characteristics • Hidden mandate, logical risk pool,

Changes over time • Employer-based coverage peaked in the 1980s and has been slowly declining. • Movement away from community rating to experience rating. “quasi-social insurance” nonprofit Blues with large firms. Unions played key role • Movement of for-profit insurance moved toward experience rated plans • Movement to self insure

Employers’ Comparative Advantage in Offering Health Insurance • Not subject to federal or state income taxes or Social Security payroll tax • For the typical worker, this reduces the cost of insurance by about 1/3 • Mitigates adverse selection • Effective risk pool with a hidden mandate • Large economies of scale • Loading factor per enrollee (includes profits and any risk premium, plus marketing and admin costs) may be as little as half for individually purchased.

Who Pays for Insurance? • Firms hire workers based on what those workers can do for the bottom line. Workers must “earn” their compensation (at least in the long run). • So in theory, a worker’s wage is lowered by an amount exactly equal to the amount of the insurance, so the worker pays the total premium by accepting a proportionate lower wage.

Who Pays for Insurance? • When health premiums increase, this requires wages to fall. Inflation and increased productivity can help. But when premiums are rising faster than productivity this poses a problem. • Short run vs. long run • Workers do not necessarily perceive that they are paying for insurance through lower wages, but see it as something their employer does for them. So on the one hand this helps us with the hidden mandate, but also harms us since it shields the worker from the cost of insurance and healthcare.

Employers’ Offering Reflect Workers’ Preferences • Supply and demand work together to determine compensation • Benefit package reflects the firm’s attempt to balance the preferences of workers • The more homogeneous the work force the easier this is to do

Flaws in System • Administrative costs – on the order of 13-16% of premium. Does not include administrative costs on the provider or employer’s side. • Allocation of costs – higher wage workers pay less when account for tax savings • Labor relations • Misaligned incentives

The decline in offer rates is not as large as you might expect

Workers in “high wage” firms tend to not only have better coverage, but they also pay a lower percentage of the premium (24% vs 34% for family coverage.

PPOs are still the largest type of insurance. Note the decline in the HMO, but even in its prime, it was not the dominate model. Also the large rise in HDHP/SO is recent years is significant. The percentage of HSAs has increased pretty dramatically. About 30% of firms offered a HDHP/SO option in 2013. In 2010 it was 15%.

Wellness programs have become quite a prominent part of employer provided health insurance, especially among large firms.