Download

1 / 13

640 likes | 1.34k Views

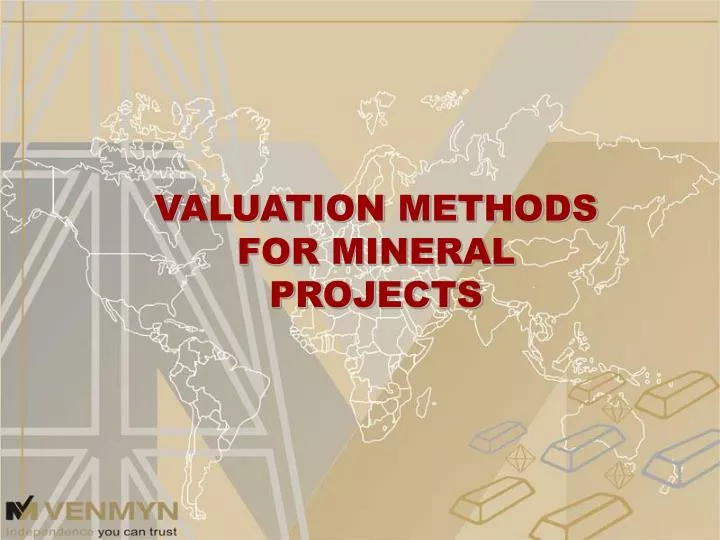

VALUATION METHODS FOR MINERAL PROJECTS. Resources. Reserves. PROSPECT. MINE. MINERAL EXPLORATION. PROJECT CONSTRUCTION. EVALUATION. PRODUCTION. PROJECT . COMMISSIONING. FEASIBILITY. STUDY. PRE-FEASIBILITY . STUDY. DESK TOP . STUDY. DISCOVERY. Value. Confidence.

E N D

VALUATION METHODS FOR MINERAL PROJECTS

Resources Reserves PROSPECT MINE MINERAL EXPLORATION PROJECT CONSTRUCTION EVALUATION PRODUCTION PROJECT COMMISSIONING FEASIBILITY STUDY PRE-FEASIBILITY STUDY DESK TOP STUDY DISCOVERY Value Confidence A function of the amount of knowledge on a mineral resource/property and the degree of probability of it being brought to account.

MINE PROSPECT MINERAL EXPLORATION PROJECT CONSTRUCTION EVALUATION PRODUCTION PROJECT COMMISSIONING FEASIBILITY STUDY PRE-FEASIBILITY sTUDY DESKTOP STUDY DISCOVERY Value Confidence A function of the amount of knowledge on a mineral resource/property and the degree of probability of it being brought to account Resources Reserves • STANDARD METHODS • Prospectivity Enhancement Multiplier (“PEM”) • Comparative Value Method • Royalties/Farm-in Agreements

STANDARD METHODS 1. Prospectivity Enhancement Multiplier (“PEM”) • Based on the principle of “Past Expenditure”; • A premium (or discount) multiplier is applied to the total cost of exploration to date, depending on whether the exploration has enhanced the prospectivity of the ground or not; • Multiplier typically ranges from 0.5 – 3.0; • Historical expenditures must be declared as audited; • Issue – Subjective choice of multiplier value.

STANDARD METHODS 2. Comparative Value Method • Value is based upon recent ‘arms length’ transactions of a similar nature; • Based on a monetary value per unit of resource in the ground or per unit area of defined mineralisation; • Issue – Often insufficient similar publicly quoted transactions to make a meaningful comparison.

STANDARD METHODS 3. Royalties or Farm–in Agreements • The initial committed expenditure establishes a base value for the property; • The staged expenditure is discounted to determined the value a buyer is placing on the vendor’s interest; • The funding partner predetermines the ratchet effect of exploration success (PEM). This is a legal document and thus the value is firmly entrenched; • The level of discounting is an opinion based on the probability that the buyer will actually commit the funds; • Issue – Aspects of the method are subjective.

MINE PROSPECT MINERAL EXPLORATION PROJECT CONSTRUCTION EVALUATION PRODUCTION Resources Reserves PROJECT COMMISSIONING FEASIBILITY STUDY PRE-FEASIBILITY STUDY DESK TOP STUDY DISCOVERY Value A function of the amount of knowledge on a mineral resource/property and the degree of probability of it being brought to account STANDARD METHODS & EXPECTED VALUE METHOD Confidence

EXPECTED VALUE METHOD • Statistically defines the probability of successful outcome of expenditure; and • Based upon geological knowledge, cost and time. • Issue – Highly subjective.

MINE PROSPECT MINERAL EXPLORATION PROJECT CONSTRUCTION EVALUATION PRODUCTION Resources Reserves PROJECT COMMISSIONING FEASIBILITY STUDY PRE-FEASIBILITY STUDY DESK TOP STUDY DISCOVERY Value A function of the amount of knowledge on a mineral resource/property and the degree of probability of it being brought to account DCF & STANDARD METHODS Confidence

DISCOUNTED CASHFLOW METHOD (“DCF”) • Where possible a cashflow model should be generated; • This method takes into account the uniqueness of each resource; • Value is calculated from future cashflows generated from the mining of the mineral resource; • Cashflow assumptions are based on the likely costs of construction, production and sales for a mine of a similar nature; • Discount rate is applied to the cashflows according to the risk profile; • Issues - The accuracy of the input assumptions; and • - The selection of a suitable discount rate which is a highly contentious issue; • Question – Should inferred resources be included?

MINE PROSPECT MINERAL EXPLORATION PROJECT CONSTRUCTION EVALUATION PRODUCTION Resources Reserves PROJECT COMMISSIONING FEASIBILITY STUDY PRE-FEASIBILITY STUDY DESK TOP STUDY DISCOVERY Value Confidence A function of the amount of knowledge on a mineral resource/property and the degree of probability of it being brought to account DCF & OPTION PRICING

OPTION PRICING MODEL • Typically used for Wits gold properties; • Method is applied when the current viability of exploiting the resource is negative by using the DCF; • Reflection of the potential for the resource to be developed into a viable mine at some time in the future when the commodity price is favourable; • The owner of the resource has the option to list the project on a stock exchange and realise the value the market would place on it; • Use the option pricing theory to calculate the commodity price at which the full risk adjusted NPV of the mine is greater than 0.

THE BOTTOMLINE “Where possible, use a number of different valuation methods to increase the voracity of your results” Venmyn