Download

1 / 21

271 likes | 836 Views

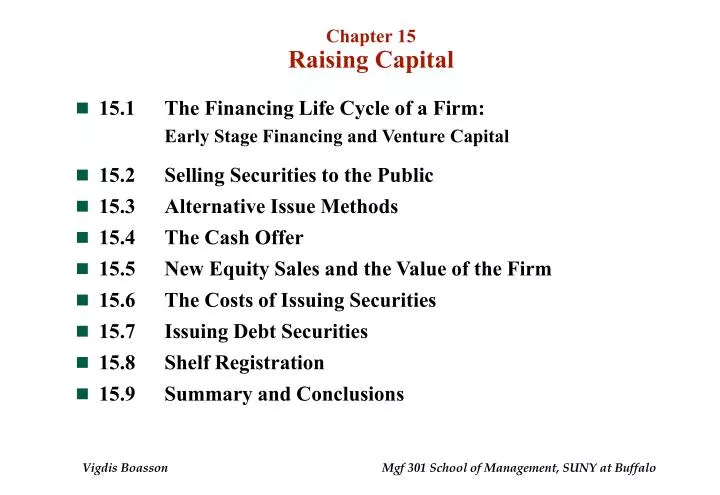

Chapter 15 Raising Capital. 15.1 The Financing Life Cycle of a Firm: Early Stage Financing and Venture Capital 15.2 Selling Securities to the Public 15.3 Alternative Issue Methods 15.4 The Cash Offer 15.5 New Equity Sales and the Value of the Firm 15.6 The Costs of Issuing Securities

E N D

Chapter 15Raising Capital • 15.1 The Financing Life Cycle of a Firm: Early Stage Financing and Venture Capital • 15.2 Selling Securities to the Public • 15.3 Alternative Issue Methods • 15.4 The Cash Offer • 15.5 New Equity Sales and the Value of the Firm • 15.6 The Costs of Issuing Securities • 15.7 Issuing Debt Securities • 15.8 Shelf Registration • 15.9 Summary and Conclusions Vigdis Boasson Mgf 301 School of Management, SUNY at Buffalo

15.2 Evaluation Activities Carried Out By Venture Capitalists “Prior to funding an investment as lead investor, how often do you engage in the following activities?” Interview management team/tour facilities 100% Tour facilities 100% Contact former business associates/outside investors 96% Contact current customers 93% Have informal discussions with experts about the product 84% Conduct in-depth review of pro forma financials 84% Contact competitors 71% Contact banker 62% Contact suppliers 53% Secure formal technical study of product 36% Secure formal market research study 31%

15.3 Venture Capitalist • Venture Capital • Venture capital financing for new, often high-risk ventures. • First-stage financing early financing used to get the firm off the ground • Second-stage financing subsequent financing to begin operations and manufacturing Key Considerations in Choosing a Venture Capitalist: • Financial Strength - the ability to supply additional resources • Management Style - level of involvement in decision-making • References - the results of previous ventures • Contacts - ability to provide introductions • Exit Strategy - how and under what circumstances does the venture capitalist plan to “cash out”?

15.4 The Basic Procedure for a New Issue • 1. Obtain Approval from the Board of Directors • 2. File Registration Statement with SEC • 3. 20-Day Waiting Period Provide Preliminary Prospectus Place Tombstone Ad File Price Amendment with SEC • 4. Sell Securities to the Public

15.5 An example of Tombstone Advertisement (Figure 15.1) 58,750 Shares Consolidated Rail Corporation Common Stock (par value $1.00 per share) __________ Price $28 Per Share __________ The shares are being sold by the United States Government pursuant to the Conrail Privatization Act. The Company will not receive any proceeds from the sale of the shares. Upon request a copy of the Prospectus describing these securities and the business of the Company may be obtained within any State from any Underwriter who may legally distribute it within such State. The securities are offered only by means of the Prospectus, and this announcement is neither an offer to sell nor a solicitation of any offer to buy. 52,000,000 Shares The portion of the offering is being offered in the United States and Canada by the undersigned. (continued)

15.6 Alternative issue methods • General cash off - issue of securities offered for sale to the general public on a cash basis. • Rights offer - a public issue of securities in which securities are first offered to existing shareholders. • IPO (Initial public offering) - a new equity issue of securities by a company that has previously issued securities to the public. • Seasoned equity offering - a new equity issue of securities by a company that has previously issued securities to the public

15.7 Underwriters • Underwriters - investment firms that act as intermediaries between the issuer and the public. Services provided include: • 1. advice on type of security and offer method • 2. advice on price • 3. advice on selling • Syndicate - a group of underwriters, formed to share the underwriting risk. • Spread - the difference between the underwriter's buying price and the offering price; it is the underwriter's main source of compensation.

15.8 Underwriters • A. Choosing an Underwriter • Competitive offer basis taking the underwriter that bids the most for the securities. • Negotiated offer basis the more common (and expensive) method. • B. Types of Underwriting • 1. Firm commitment underwriting the most prevalent form for seasoned new issues. The underwriter buys the entire issue of securities at an agreed upon price from the issuer, and assumes responsibility for reselling them. • 2. Best efforts underwriting common with IPOs, the underwriter promises to sell as much as possible at the offer price, but unsold securities are returned to the issuer.

15.9 IPO • IPOS AND UNDERPRICING • The underpricing of new issues, especially IPOs, appears to be common. • 2. Why does underpricing exist? • Smaller, more speculative issues account for much of the observed underpricing. • It is argued that because "underpriced" IPOs are oversubscribed while "overpriced" issues are avoided, underpricing is necessary to allow the average investor to make a normal return across all issues. • Underpricing is a kind of insurance for underwriters against legal suits by angry stock buyers if issues were overpriced.

15.10 Average Initial Returns by Month for SEC-Registered IPOs: 1960-1996 (Fig. 15.2) Percentage Average Initial Return

15.11 Number of Offerings by Month for SEC-Registered IPOs: 1960-1996 (Fig. 15.3) Number of Offerings Source: Roger G. Ibbotson, Jody L. Sindelar, and Jay R. Ritter, “The Market’s Problems with the Pricing of Initial Public Offerings” Journal of Applied Corporate Finance 7 (Spring 1994), as updated by the authors.

15.12 Average Initial Returns Categorized by Annual Sales of Issuing Firm (Table 15.3) Annual Sales of Issuing firms Number of firms Average initial returns 0 386 42.9% 1-999,999 678 31.4 1,000,000-4,999,999 353 14.3 5,000,000-14,999,999 347 10.7 15,000,000-24,999,999 182 6.5 25,000,000 and larger 4935.3 All 2,439 20.7%

15.13 NEW EQUITY SALES AND THE VALUE OF THE FIRM • NEW EQUITY SALES AND THE VALUE OF THE FIRM • Stock prices tend to decline following the announcement of a new equity issue, and rise on news of a debt offering. Some suggested reasons for this include: • 1. Managerial information. Some believe that stock is issued when managers know that it is overpriced. Market participants recognize this and react accordingly. • 2. Debt usage. Issuing new equity may signal that the firm has too much debt. • 3. Issue costs. There are substantial costs involved in issuing securities and these are typically higher for equity.

15.14 Rights Offerings: Basic Concepts • Rights offering • Share rights • Offering terms • Subscription price • Number of rights to purchase a share • Value of a right • Ex-rights date • Holder-of-record date

15.15 The Value of a Right • The value of a right equals the difference in the price of the issuer’s outstanding shares before and after the rights offering, and is determined by three factors: - the total amount of money to be raised, - the subscription price of the new shares, and - the number of existing shares. The number of new shares to be issued equals (Funds to be raised)/Subscription price

15.16 The Value of a Right (concluded) The number of rights needed to buy one share: = (Number of old shares)/(Number of new shares) After the offering, the new value of the firm is: Pre-offering firm value + funds raised, and the new share price must be: (New firm value) / (Total number of shares outstanding). The value of the right must equal: Old share price - new share price.

15.17 Ex Rights Stock Prices (Figure 15.4) Rights On Ex Rights Announcement Ex-rights Record date date date September 30 October 13 October 15 Rights-on price $20.00 $3.33 =Value of a right Ex-rights price $16.67

15.18 Rights Offerings: Issues • Standby fees • Oversubscription privilege • Effects on shareholders • The rights offerings “puzzle”

15.19 New Issues and Dilution • Dilution - loss in existing shareholders’ value • Dilution of proportionate ownership • Dilution of market value • Dilution of book value and earnings per share (EPS) • Under what circumstances does market value dilution occur?

15.20 Solution to Problem 15.1 Bajor Mining Co. is proposing a rights offering. Presently there are 250,000 shares outstanding at $50 each. There will be 50,000 new shares offered at $40 each. a. What is the new market value of the company? b. How many rights are associated with one new share? c. What is the ex-rights price? d. What is the value of a right? e. Why might a company have a rights offering rather than a general cash offer?

15.20 Solution to Problem 15.1 (concluded) a. New value = (250,000 $50) + (50,000 $40)$14.5 million b. There will be (250,000/ 50,000 ) = 5 rights associated with each new share. c. The ex-rights price is $14.5 million/300,000 = $48.33. d. The value of one right equals $5048.33 = $1.67.