Download

1 / 8

620 likes | 2.91k Views

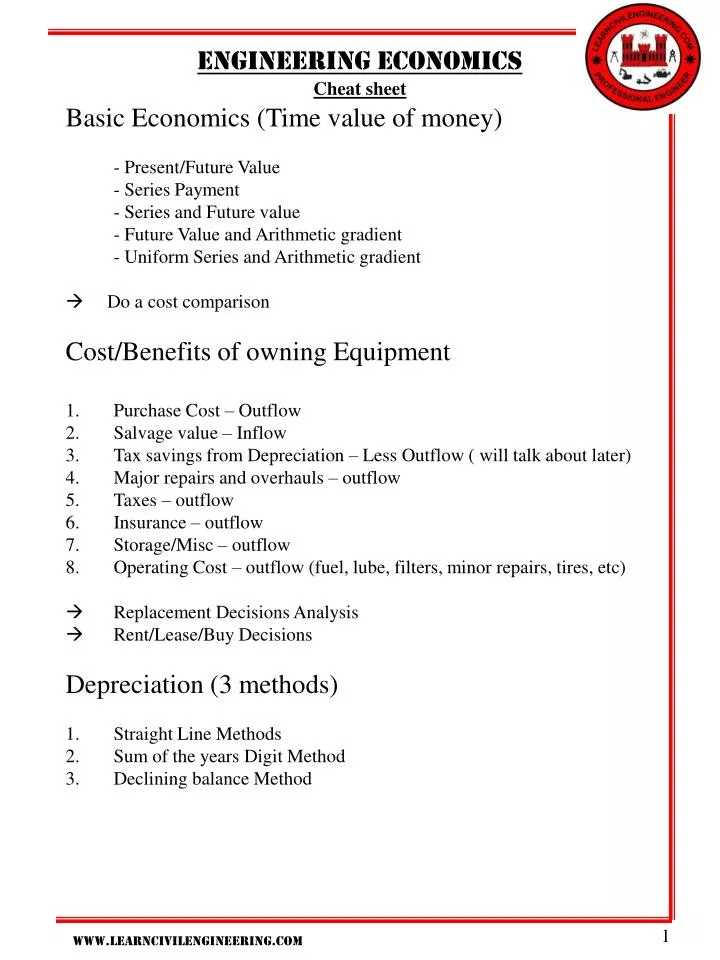

Engineering economics Cheat sheet. Basic Economics (Time value of money) - Present/Future Value - Series Payment - Series and Future value - Future Value and Arithmetic gradient - Uniform Series and Arithmetic gradient Do a cost comparison Cost/Benefits of owning Equipment

E N D

Engineering economics Cheat sheet • Basic Economics (Time value of money) • - Present/Future Value • - Series Payment • - Series and Future value • - Future Value and Arithmetic gradient • - Uniform Series and Arithmetic gradient • Do a cost comparison • Cost/Benefits of owning Equipment • Purchase Cost – Outflow • Salvage value – Inflow • Tax savings from Depreciation – Less Outflow ( will talk about later) • Major repairs and overhauls – outflow • Taxes – outflow • Insurance – outflow • Storage/Misc – outflow • Operating Cost – outflow (fuel, lube, filters, minor repairs, tires, etc) • Replacement Decisions Analysis • Rent/Lease/Buy Decisions Depreciation (3 methods) • Straight Line Methods • Sum of the years Digit Method • Declining balance Method www.learncivilengineering.com

Basic economics (Time value of money) • - As everyone knows if you put money in the bank, and your money earns interest, the amount of money in the bank will increase over time. • These type of problems can be solved with equations and/or value tables. Table is the quicker way however, you may have to use equations for some problems that are not as straight forward. • present/future value- • The equation for calculation Present/Future Value is; • F= P(1+i)n or P = F/ (1+i)n F = Future value after n time • P = Present Value • i = interest rate per period • n = number of periods • sometimes the problem calls for you to find the interest rate; i= (F/P)1/n – 1 • Quick Ex Problem to illustrate point: • You put $2000 in a savings account that generates 3% interest per year (annual). What is the value after 10 years. • Solution: P = $2000, i= .03, n = 10 years • F= P(1+i)n = $2000(1+.03)10= $2000(1.344) = $2,687 • Try using the charts and see if you can get the same answer – Look in the F/P section. F = x(P), x = number from chart • What is the solution if the 3% interest rate was per month? Solution: i= .03, n=10 years(12months/year) = 120, $2000(1+.03)120= $2000(34.7) = $69,422 • What is the solution if the 3% interest rate was per year but compounded monthly? Solution: i= .03/12 = .0025, n=10 years(12months/year) = 120, $2000(1+.0025)120= $2000(1.35) = $2,699 which is more than same interest rate compounded yearly • What is the interest rate if you invested $7,000 and receive $11,000 after 7 years? • - i= (F/P)1/n – 1 = ($11,000/$7,000)1/7 – 1 = .067 = 6.7 % www.learncivilengineering.com

Series payments- • Number 1 Type is the common loan payment schedule that we are all used to. If you get a loan for a car, house or a construction business loan, this is the equation you need to figure out what are your monthly payments. • The equation for calculating a Present Value/Series payment is; • P=A[(1+i)n- 1]/[i(1+i)n] A = Series Payments • P = Present Value • i = interest rate per period • n = number of periods • Quick Example Problem to illustrate point: • You acquire a 10 year bank loan for $2,000,000 for a construction project at a 3.5% annual interest rate. What are your monthly payments? • Solution: P = $2,000,000, i= .0029, n = 10 years = 120 months • P=A[(1+i)n- 1]/[i(1+i)n] = A=P/[(1+i)n- 1]/[i(1+i)n) = • A=$2,000,000/[(1+.0029)120- 1]/[.0029(1+.0029)120) = • A =$2,000,000/[1.415- 1]/[.0029(1.415)] = • A =$2,000,000/[.415]/[.0041] = • A =$2,000,000/[101.22] = $19,759 • Try using the charts and see if you can get the same answer – Look in the A/P section. • Number 2 Type is the common investment strategy. You make a series of investments/payments and you assume a interest rate, what is the lump sum in the future. • The equation for calculating a Future Value/Series payment is; • F=A[(1+i)n- 1]/[i] A = Series Payments • F = Future Value • i = interest rate per period • n = number of periods • Quick Example Problem to illustrate point: • You make a $10,000 yearly payment to your 401K for 20 years, assuming a 7% annual rate of return. How much money should you have when you retire in 20 years. • Solution: F = $10,000, i= .07, n = 20 years • F=A[(1+i)n- 1]/[i] = $10,000[(1+.07)20 – 1]/.07 = • F = $409,954 • Try using the charts and see if you can get the same answer – Look in the F/A section. www.learncivilengineering.com

Arithmetic gradient- • Arithmetic gradients are when payment increase after every payment. It is not very common in loans or investments. However, if you know that every year or month you are going to increase your investment to figure out the future value you will need to use these formulas. • The equation for calculating Future Value and Arithmetic Gradient is; • F=G/i[((1+i)n- 1)/i)-n] F = Future Value • G = Arithmetic Gradient (Value increased per period) • i = interest rate per period • n = number of periods • Quick Example Problem to illustrate point: • You are making monthly payments of 0, 500,1000,1500, etc for 11 years. What is the lump sum payment after 11 years if the interest rate is 5%? • Solution: G = $500, i= .05, n = 11 years • F=G/i[((1+i)n- 1)/i)-n] = $500/.05[((1+.05)11- 1)/.05)-11] • = $500/.05[((.71)/.05)-11] = = $500/.05[((14.21)-11] = = $500/.05[3.21] • $500/.05[3.21] = $32,100 • Try using the charts and see if you can get the same answer – Look in the F/G section. • The equation for calculating Present Value and Arithmetic Gradient is; • P = Present Value • G = Arithmetic Gradient (Value increased per period) • i = interest rate per period • n = number of periods www.learncivilengineering.com

Series payments- • Number 1 Type is the common loan payment schedule that we are all used to. If you get a loan for a car, house or a construction business loan, this is the equation you need to figure out what are your monthly payments. • The equation for calculating a Present Value/Series payment is; • P=A[(1+i)n- 1]/[i(1+i)n] A = Series Payments • P = Present Value • i = interest rate per period • n = number of periods • Quick Example Problem to illustrate point: • You acquire a 10 year bank loan for $2,000,000 for a construction project at a 3.5% annual interest rate. What are your monthly payments? • Solution: P = $2,000,000, i= .0029, n = 10 years = 120 months • P=A[(1+i)n- 1]/[i(1+i)n] = A=P/[(1+i)n- 1]/[i(1+i)n) = • A=$2,000,000/[(1+.0029)120- 1]/[.0029(1+.0029)120) = • A =$2,000,000/[1.415- 1]/[.0029(1.415)] = • A =$2,000,000/[.415]/[.0041] = • A =$2,000,000/[101.22] = $19,759 • Try using the charts and see if you can get the same answer – Look in the A/P section. • Number 2 Type is the common investment strategy. You make a series of investments/payments and you assume a interest rate, what is the lump sum in the future. • The equation for calculating a Future Value/Series payment is; • F=A[(1+i)n- 1]/[i] A = Series Payments • F = Future Value • i = interest rate per period • n = number of periods • Quick Example Problem to illustrate point: • You make a $10,000 yearly payment to your 401K for 20 years, assuming a 7% annual rate of return. How much money should you have when you retire in 20 years. • Solution: F = $10,000, i= .07, n = 20 years • F=A[(1+i)n- 1]/[i] = $10,000[(1+.07)20 – 1]/.07 = • F = $409,954 • Try using the charts and see if you can get the same answer – Look in the F/A section. www.learncivilengineering.com

Depreciation- • Depreciation means the decline in fair market value of an item due to its age and it standard deterioration. There are two very separate uses for depreciation. One is for tax liability and the other one is for calculation the allocation of the cost of the asset per time period used. • The Main methods for depreciation are 1. Straight Line Method 2. Sum of the years Digit Method 3. Declining balance Method 4. 200% Declining Balance Method • Straight Line Method This is the simplest and most often used method. All you do is estimate the salvage value of the asset at the end of a time period. Then subtract that salvage value from the initial value and divide by the time period. That value will be the depreciation per year. Dn = (Initial Cost – Salvage Value)/ N Dn = Depreciation per period N = Equipment life per period Example: A dozer that you own depreciates over a 7 year period and was purchased for $168,000 and will have a salvage value of $30,000. a. What is the depreciation value per year? What is the book value of the dozer at the end of two years. b. What is the book value of the dozer at the end of two years. Answer: a. Find Dn = $168,000 - $30,000 = $138,000/7 = $19,714 b. Find book value = Initial Cost – Dn(n) = $168,000 – ($19,714)(2years) = $128,572 www.learncivilengineering.com

Depreciation- • Sum of the year Digit Method This method is a depreciation that results in a more accelerated write off than straight line but less than declining balance method. • The sum of the digits can be determined by using the following formula; Dn = (n2 + n)/ 2 , where n is equal to useful life of the assets Or just sum the digits. • So for an example if the useful life of an asset is 5 years. The sum of the would be (52 + 5)/2 = 15, or 5+4+3+2+1 = 15 • The depreciation rates are as follows if you are using the 5 years of the useful life - For example: 1st Year: 5/15, 2nd Year: 4/15, 3rd Year: 3/15, 4th Year: 2/15, 5th Year: 1/15 Example: A dozer that you own depreciates over a 7 year period and was purchased for $168,000 and will have a salvage value of $30,000. a. Using the Sum of the year Digit Method. What is the depreciation value by year? b. What is the book value of the dozer at the end of two years. Answer: • Find Dn = (72 + 7)/2 = 28 , 7+6+5+4+3+2+1 = 28 1st Year: $168,000 - $30,000 = $138,000(7/28) = $34,500 2nd Year: $138,000(6/28) = $29,571 3rd Year: $138,000(5/28) = $24,643 4th Year: $138,000(4/28) = $19,714 5th Year: $138,000(3/28) = $14,785 6th Year: $138,000(2/28) = $9,857 7th Year: $138,000(1/28) = $ 4,928 b. Find book value = Initial Cost – Dn(n) = $168,000 – ($34,500+$29,571) = $103,929 www.learncivilengineering.com

Depreciation- • Declining Balance Depreciation Method • This method accelerates the depreciation since a large part of the depreciated cost is taken at the beginning of the life of the asset. • To calculate declining balance depreciation the depreciable basis of the fixed asset is multiplied by a factor. The factor is the percentage of the asset that would be depreciated each year under straight line depreciation times an accelerator. • For example, an asset with a five year life would have 20% of the cost depreciated each year. If the accelerator is 200% then the factor would be 40% (20% x 200%). The 200% accelerator is referred to as double declining balance and is the most common. But you put 150% or any accelerator percentage if it was specified. Example: A dozer that you own depreciates over a 7 year period and was purchased for $168,000 and will have a salvage value of $30,000. a. Using the double declining balance. What is the depreciation value by year? b. What is the book value of the dozer at the end of two years. Using double declining balance the depreciation would be calculated as follows: factor = 2 * (1/7) = 0.285 • since the salvage value was $30,000 after the 6th year, you weren’t able to use anymore depreciation. If the salvage value was lower you would be able to. • Book value after 2 years is $85,886. www.learncivilengineering.com