Download

1 / 20

200 likes | 300 Views

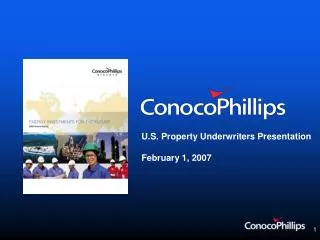

U.S. Property Underwriters Presentation February 1, 2007. CAUTIONARY STATEMENT FOR THE PURPOSES OF THE “SAFE HARBOR” PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995.

E N D

CAUTIONARY STATEMENTFOR THE PURPOSES OF THE “SAFE HARBOR” PROVISIONSOF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 Forward Looking Statements - The following presentation includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended, which are intended to be covered by the safe harbors created thereby. You can identify our forward-looking statements by words such as “anticipates,” “expects,” “intends,” “plans,” “projects,” “believes,” “estimates,” and similar expressions. Forward-looking statements relating to ConocoPhillips’ operations are based on management’s expectations, estimates and projections about ConocoPhillips and the petroleum industry in general on the date these presentations were given. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Further, certain forward-looking statements are based upon assumptions as to future events that may not prove to be accurate. Therefore, actual outcomes and results may differ materially from what is expressed or forecast in such forward-looking statements. Factors that could cause actual results or events to differ materially include, but are not limited to, crude oil and natural gas prices; refining and marketing margins; potential failure to achieve, and potential delays in achieving expected reserves or production levels from existing and future oil and gas development projects due to operating hazards, drilling risks, and the inherent uncertainties in interpreting engineering data relating to underground accumulations of oil and gas; unsuccessful exploratory drilling activities; lack of exploration success; potential disruption or unexpected technical difficulties in developing new products and manufacturing processes; potential failure of new products to achieve acceptance in the market; unexpected cost increases or technical difficulties in constructing or modifying company manufacturing or refining facilities; unexpected difficulties in manufacturing, transporting or refining synthetic crude oil; international monetary conditions and exchange controls; potential liability for remedial actions under existing or future environmental regulations; potential liability resulting from pending or future litigation; general domestic and international economic and political conditions, as well as changes in tax and other laws applicable to ConocoPhillips’ business. Other factors that could cause actual results to differ materially from those described in the forward-looking statements include other economic, business, competitive and/or regulatory factors affecting ConocoPhillips’ business generally as set forth in ConocoPhillips’ filings with the Securities and Exchange Commission (SEC), including our Form 10-K for the year ending December 31, 2005, as updated by our subsequent periodic and current reports on Forms 10-Q and 8-K, respectively. ConocoPhillips is under no obligation (and expressly disclaims any such obligation) to update or alter its forward-looking statements, whether as a result of new information, future events or otherwise. Non-GAAP Financial Measures - This presentation includes certain non-GAAP financial measures, as indicated. Such non-GAAP measures are intended to supplement, not substitute for, comparable GAAP measures. Investors are urged to consider closely the comparable GAAP measure and the reconciliation to that measure provided in the Appendix or on our website at www.conocophillips.com. This presentation (Slide 32) contains an illustrative example calculating a measure, "EBITDA," that is not calculated in accordance with U.S. generally accepted accounting principles (GAAP). The example demonstrates a scenario for just one of the many that were evaluated in the evaluation process, and is an estimate of how costs, and resulting margins, could possibly perform at a given West Texas Intermediate (WTI) oil price. The example estimates the various costs (field operating, natural gas, diluent, transportation) at a $50 WTI example, and then estimates the resulting EBITDA margin that would result from this scenario. EBITDA consists of earnings before interest expense, income tax expense, and depreciation, depletion and amortization. EBITDA should not be considered as an alternative to any measure of operating results as promulgated under GAAP, nor should it be considered as an indicator of overall financial performance. We have included this non-GAAP financial measure because, in management's opinion, it most closely portrays a cash margin, which management believes will be an important measure in an analysis of cash flow consideration for the proposed joint ventures. Since the use of EBITDA is in the context of an illustrative example, a reconciliation to the most comparable GAAP measure (cash flow from operations) is not possible, as the GAAP components excluded from EBITDA were not estimated for purposes of such example. In this presentation, peer group “non-core earnings impacts” include publicly-disclosed gains and losses on asset dispositions, asset impairments, changes in litigation accruals, write-offs, uninsured losses, and restructuring charges, in each case, to the extent such items are in excess of >$249 million as well as all cumulative effect of accounting changes and discontinued operations, regardless of amount. Prohibited Terms - The U.S. Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We may use certain terms in this presentation such as “oil/gas resources,” “Syncrude,” “probable resources,” “inventory,” and/or “Society of Petroleum Engineers (SPE) proved reserves” that the SEC’s guidelines strictly prohibit us from including in filings with the SEC. U.S. investors are urged to consider closely the oil and gas disclosures in our Form 10-K for the year ended December 31, 2005 as updated by our subsequent quarterly reports on Form 10-Q.

Current Environment • High crude oil prices • Strong demand growth around the world • Limited excess production capacity • Instability and supply disruptions in major oil-producing countries • Higher industry costs • Tightness in the global refining system

Access to Oil & Gas Reserves is a Greater Constraint Than Geology(BBOE) NOC reserves(equity access) Reserves held by Russian companies Full IOC accessreserves 270 / 12% 157 / 7% 360 / 16% 1,462 / 65% IOC = international oil company NOC = national oil company NOC Reserves (no equity access) Reserve figures are conventional Billion BOE, 2005 (2249 BBOE) Source: PFC Energy

Rising Costs of Reserve Replacement Marginal cost is defined as the average of the highest 75 cost (or bottom quartile) producers • Higher F&D costs • Wider transportation & quality • differentials • Higher government take 60 45 Dollars per Barrel 30 15 0 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Source: Goldman Sachs

Challenging Environment • Limited resource access • Intense competition • Industry cost inflation • Increased government take • Increased political risk • Energy cost impact to consumers We are responding to these challenges

Corporate Strategy • Build on international scale and integration • Grow E&P portfolio • Grow R&M position • Use Commercial expertise to create valuefrom integration and asset position • Move to AA credit rating • Manage cost and project execution • Utilize strengths in people, technology, and financial resources Creating Shareholder Value

Financial Strategy • Fund Growth Program • Portfolio optimization • Move to AA credit rating • Debt reduction • Equity improvement • Target debt/capital ratioof 15-20% • Annual dividend increases • Share repurchases

Investing in Growth Sunrise Caldita ANS Gas Mackenzie Delta Suban II Bayu-Undan Kerisi / Hiu Brass LNG Qatargas 3 LNG Plataforma-Deltana North Belut Suban III Corocoro I Bohai Phase II Yuzhno Khylchuyu Libya Kashagan II Kashagan Sat’s Corocoro II & III West Qurna Malikai Su Tu Trang Kebabangan Libya Kashagan I Su Tu Vang Gumusut Ketapang Libya West Sak Ekofisk Growth Surmont Syncrude III Alaska WNS Sat’s Britannia Sat’s Alvheim Statfjord Late Life Rivers Field Deep Bossier Hejre Tommeliten Alpha Eldfisk Upside Alaska Sat’s Woodford Shale North America BD Syncrude IV & V Surmont II & III Clair II Thornbury Canada Oil Sands 2006 - 2008 2008 - 2011 2011+

Major R&M Growth Projects Purchased 260 MBD German refinery in 2006, additional investments to increase advantaged crude processing EnCana JV; investment to expand heavy oil processing to 550MBD with total capacity increasing to 600MBD by 2015 Proposed development of a 400MBD export refinery in Yanbu, targeted production date is 2011 Potential development of 500MBD refinery in Fujairah; JV with International Petroleum Investment Company of Abu Dhabi • Wilhelmshaven Refinery • Wood River and Borger Refineries • Saudi Aramco Refinery • UAE Refinery

Strong North American Presence • #1 in gas production & a leading gas marketer • #2 U.S Refiner • Engaged in several LNG and re-gasification projects • Strong positions in Alaskan North Slope gas and Mackenzie Delta gas • Strong Canadian Oilsands position

Burlington Resources Acquisition • Created leading North American gas position • High-quality, long-lived, low-risk gas reserves • Significant unconventional resource plays • Enhanced production growth / N.A. gas supply • Near-term conventional / unconventional • Long-term LNG and Arctic gas • Enhanced business mix • Increases E&P, OECD, and North American gas • Significant free cash flow • Synergies of $500 MM • Access to technical capabilities

North America2005 Gas Production Note: Production figures are based on YE 2005 Filings. COP volumes do not include fuel gas production. CVX pro forma for UCL. 13

ChristinaLake FosterCreek WoodRiver Borger EnCana and ConocoPhillips are creating a long-term integrated North American heavy oil business North American Heavy Oil Partnership • Venture comprised of two 50/50 Partnerships: Upstream Partnership • EnCana’s Foster Creek and Christina Lake projects Downstream Partnership • ConocoPhillips’ Wood River and Borger refineries • Partnerships of equivalent value • Effective date: January 2, 2007

Canadian Oilsands Relative Land Positions (Net Sections) Global Crude Oil Supply Resources (Bbbls) Canadian Oilsands – Largest NA Resource 347.2 262.7 190.1 132.5 115.0 99.0 COP and ECA are both post-transaction positions 97.8 72.3 39.1 35.3 29.4 17.1 14.8 11.2 9.7 4.5 Notes: COP includes addition of 50% of ECA Foster Creek & Christina Lake acreage; and ECA is reduced by same amount; Includes only land associated with the Athabasca Oil Sands Deposit. Source: Alberta Energy and Utilities Board; and Company reports. Source: International Energy Agency; Energy Information; OPEC; BP Statistical Review of World Energy, 2005

Illustrative Integrated Margin EBITDA margin ($/bbl)* Increasing Diff. IncreasesDownstream Margin Downstream Downstream Varying Differential Downstream Decreasing Diff. IncreasesUpstream Margin Upstream Upstream Upstream Participation in both Partnerships provides more certainty in overall margin *Note: Based on information after all project completions; 2006 $ terms; EBITDA Margin defined as: Revenues – Opex – Gas cost/Feedstock cost – Transport.

Total Company Cash Flow2006 $MM Cash & Other 895 Asset Sales 545 Net BR acquisition 1,134 Dividends & Share Repurchases 3,202 1/1/06 Cash 2,214 Debt Reduction 5,059 Capex, Loans & Investments 16,253 CFOA 21,516 Total 25,409 Uses of Cash Sources of Cash Sources of Cash includes the net of cash paid to Burlington Resources shareholders, cash acquired and debt issued associated with the Burlington Resources Acquisition. The Debt Reduction in Uses of Cash is from March 31, 2006.

Full Year 2006 Cash Use Comparison * COP reflects actual results. Peer data estimated by annualizing 9 month actual results.

Debt Ratio Balance Sheet Debt $B Debt-to-Capital Ratio % Equity* $B * Includes minority interests

Summary • Tight supply & demand balance for crude & refined products. • Challenging Environment • Limited resource access • Intense competition • Industry cost inflation • Increased political risk and government take • ConocoPhillips is aggressively investing in new energy supplies for the United States.