Download

1 / 41

430 likes | 811 Views

Online Banking. Take Charge of your Finances. Checks – Demand Deposits. What Does Demand Deposit Mean? An account from which deposited funds can be withdrawn at any time without any notice to the depository institution.

E N D

Online Banking Take Charge of your Finances

Checks – Demand Deposits What Does Demand Deposit Mean?An account from which deposited funds can be withdrawn at any time without any notice to the depository institution. • This account allows you to "demand" your money at any time, unlike a term deposit, which cannot be accessed for a predetermined period (the loan's term). • Most checking and savings accounts are demand deposits, accessible by the account holder at any time.

FORMALFINANCIAL SERVICES • Accounts • Credit cards • Loans • Investment vehicles • Direct deposit • Wire transfers/ remittances • INFORMAL • FINANCIAL • SERVICES • Payday lenders • Check cashing services • Rent-to-own stores • Pawn shops • Title lenders • Loans from family/friends • Cultural savings clubs • Remittances offered through nonfinancial institutions 3 Slide 1 – Formal and Informal Financial Services Lesson Reference: Introduction to Financial Services, Activity 2 – Overhead 1

Slide 1 - Placesto Save MoneyLesson Reference: Introduction to Financial Services, Activity 2 – Overhead 1 • PLACES TO SAVE MONEY • Would you save your money in any of these places? Why? Why not? Can you think of other places to save money? • Bed & Mattress • Cookie Jar • Pillow • Wallet • Money Belt • Small House Safe 4

Slide 2 - Alternative Financial Services Lesson Reference: Introduction to Financial Services, Activity 1 – Handout 1 • ALTERNATIVE FINANCIAL SERVICES • Check-Cashing Services • Check-Deferrals, Cash Advances, Payday Loans • Pawn Shops • Rapid Tax Refunds • Rent-to-Own • Other Financial Services 5

Check-Cashing Services • To cash a paycheck or government check, these businesses charge a percentage of the amount of the check as a fee. • For example, cashing a $200 paycheck could cost as much as $8 each week. In a year, that adds up to $416.

Check-Deferrals, Cash Advances, Payday Loans • Whichever name is used, these are considered short-term, high interest-rate loans. • The customer writes a personal check, including a fee (interest rate). The lender cashes the check for the customer and agrees to hold the check until the next payday. • Oftentimes, the borrower will need to take out additional loans to cover the fees and to make it through to the next payday. This can lead to a vicious cycle of debt that can be difficult to pay off.

Pawn Shops • Here you can get loans at very high interest for the value of goods, including electronics and jewelry.

Rapid Tax Refunds • To get your tax refund early from someone you pay to prepare and receive your tax return, you may have to pay a significant portion of your refund for the service.

Rent-to-Own • Renting items such as home appliances or entertainment systems before buying them from the same business can add up to fees much higher than the cost of using credit to pay for the same items.

HOW A BANK CAN SAVE YOU MONEY Monthly Fees without a Bank Monthly Fees with a Bank* • $0 to directly deposit paycheck • $0 to get cash from bank's ATMs or make debit card purchase • $0 to pay monthly bills using electronic bill payment • $5 to send money to family • Monthly cost: $5.00 • Annual cost: $60.00 • $80 to cash paychecks • $3.81 on money orders and stamps to pay bills • $15 to send money to family with a wire transfer company • Monthly cost: $98.81 • Annual cost: $1,185.72 Annual Savings by Using a Bank: $1,125.72 12 Slide 2 – How a Bank Can Save You Money Lesson Reference: Introduction to Financial Services, Activity 2 – Handout 2

Cashier’s Check • a check written by a bank on its own funds • Check over 6 months old may not be honored by a bank

Certified Check • A personal check that the bank guarantees to be good.

Safe deposit box • Important papers – • Mortgage • Insurance Policies • Stocks and Bonds • Deed • Birth certificates • Do NOT keep cash

Slide 3 - Financial Services Modernization Act Lesson Reference: Introduction to Financial Services, Activity 3 – Overhead 3 • FINANCIAL SERVICES • MODERNIZATION ACT (1999) • Transformed the banking industry. Eliminated many • restrictions among companies in the securities, • banking, and insurance industries. • Results? • Banks may offer some insurance and investment services. • Investment and insurance companies may offer some traditional banking services. Investments are not insured by FDIC. 16

1 2 3 4 5 9 8 7 6 10 11 Check Details Click the numbers This is just your check number again (see above right). Enter the date you write each check. Put your personal signature here. Here is the number of this Check. Here is where you write the name of the party you are writing your check to (the payee). Be sure to write or print legibly! On the lower line, write out the amount like this. Legibly print the amount of money this check is for. Place to add any information you want to related to this check. Make sure your personal information on the check is correct. This is the Routing Number for your bank (used for electronic transfers of funds from your account to the payee’s account) This is your Account Number. (Note that sometimes these two numbers are the reverse of what is shown here.) 5-F

581 ARDYS JOHNSON Phone: 555-0100 4250 West 18th Avenue Chicago, IL 60601-2190 2-74 710 DATE PAY TO THE ORDER OF DOLLARS For Classroom Use Only SKY CENTRAL BANK Chicago, Illinois MEMO 071000741 08 40 856 0581 Parts of a Check ABA Number Payee Drawee Drawer July 1, 20-- 36.12 Food Mart $ Thirty-six and 12/100 Ardys Johnson groceries

Checking Account • Check - A written order to a bank to pay a stated amount to the person or business named on it. • Demand deposit -Money on deposit in a bank that can be withdrawn at any time • Canceled check -A check that bears the bank’s stamp, indicating that it has cleared • Overdraft - A check written for more money than the writer’s account contains • Floating a check - Intentionally writing a check on an account without sufficient funds in the hope of making a deposit before the check is cashed.

3 1 2 Keep a Record Click Here Deposit 1/11 Deposit to Checking 200 00 200 00 200 00 Auto 1/11 Charge for Personalized Checks 20 00 20 00 WD 180 00 23 11 100 1/15 Fine Foods 23 11 Groceries 156 89 5-G

Slide 4 - Making a Deposit - Completing a Deposit Slip Lesson Reference: Basic Banking Services, Activity 6 – Handout 2 MAKING A DEPOSIT - COMPLETING A DEPOSIT SLIP 21

Slide 3 - Making a Deposit - Endorsing a Check Lesson Reference: Basic Banking Services, Activity 6 – Handout 2 MAKING A DEPOSIT - ENDORSING A CHECK The Back Side of a Check Restrictive Endorsement (most secure) Blank Endorsement(least secure) Endorsement to a third party 23

Online Banking • In the year 2006, 63 million Americans reported that they used online banking • 43% of internet users in the United States bank online

Online Banking • Online banking – also known as internet banking, allows consumers to complete transactions with wireless technology. Wireless technology includes: • Personal Computers (PCs) • Personal Digital Assistants (PDAs) • Cellular phones

Online Banking • Consumers can access account information and statements

Online Banking • Consumers can transfer funds

Online Banking • Consumers can manage bills and apply for credit

Online Banking • Advantages of online banking include: • Decreased cost of paper and postage • Storing all statements online instead of keeping a paper copy • Convenience • Paying bills online • Ability to access account anytime • No waiting for a monthly statement • Disadvantages of online banking include: • Not as personal • Not able to access without technology • Decrease in safety features • Increase in risk for fraud

Online Banking Advantages Disadvantages Not as personal Not able to access without technology Decrease in safety features Increase in risk for fraud • Decreased cost of paper and postage • Storing all statements online instead of keeping a paper copy • Convenience • Paying bills online • Ability to access account anytime • No waiting for a monthly statement

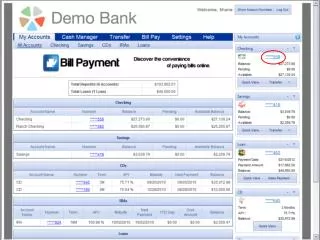

Online Bill Payment • Online bill payment – allows consumers to send money from one account to a vendor • Usually occurs automatically • Consumers need to check with the vendors regarding their policy of when the payment will be processed

Online Bill Payment • Examples of companies that use online bill payment include: • Retailer banks • Credit card companies • Insurance companies • Energy and utility companies • Health care • Transportation companies • Education expenses

Online Bill Payment • Important financial aspects include: • Checking with the vendor or company to understand their policy of when transactions are complete • Confirming there are enough funds in the account to cover the expense of the bill • Confirming bill will be paid, money will be taken out of the account, and the transaction will be completed • Their financial information is secure and it is safe to make online transactions

Determine Security • The Uniform Resource Locator (URL) ends in “s” which stands for secure • A closed lock to the right of the URL or in the bottom right hand corner of the web browser to indicate a secure site

Insecure Practices • Email accounts are not secure • Do not send important information such as: • Social security numbers • Bank account numbers • PIN numbers

Consumer Protection • The Federal Bank of Chicago suggests the following: • Passwords are a combination of letters and numbers • Change passwords once a month • Keep all receipts and compare them to bank statements monthly • Log out of depository institution Web sites immediately after you finish working • Contact the depository institution directly with any questions or concerns

Recurring Payment • Recurring payment – bills are set to be paid on the due date or a previous date set by the consumer • Payment will happen automatically electronically • Advantages of recurring payment include: • Save money on postage • Saves time for the consumer • Bills are paid on time

Regulation E • Regulation E – covers all electronic fund transfers including transfers occurring through an electronic terminal, computer, telephone, or magnetic tape • The transfer must be conducted with the purpose of authorizing a depository institution to debit or credit a consumer's account

Consumer Protection • Privacy Policy outlines how a consumer’s information will be used and protected • Opting out of a financial policy allows a consumer to request a depository institution to share only a limited amount of personal information

Conclusion • Review • Define online banking • Review what transactions can be completed through online banking • Discuss advantages and disadvantages of online banking • Discuss online bill payment • What are secure and insecure online banking practices? • Any questions?