Download

1 / 1

20 likes | 162 Views

An Artificial Stock Market Martin Sewell mvs25@cam.ac.uk University of Cambridge. Objective

E N D

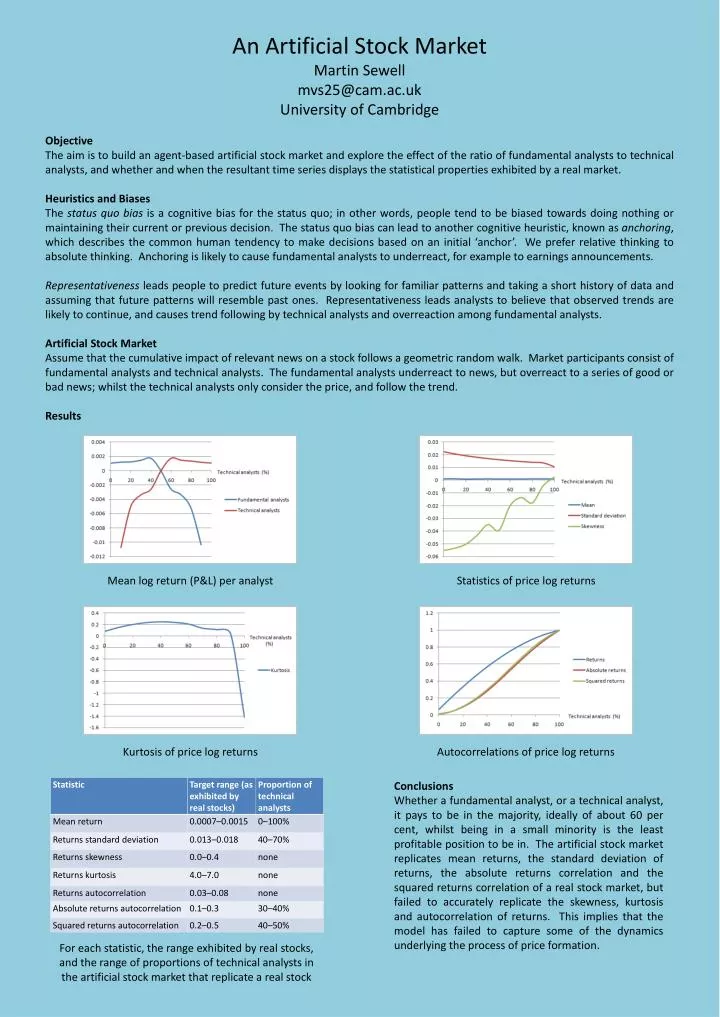

An Artificial Stock Market Martin Sewell mvs25@cam.ac.uk University of Cambridge Objective The aim is to build an agent-based artificial stock market and explore the effect of the ratio of fundamental analysts to technical analysts, and whether and when the resultant time series displays the statistical properties exhibited by a real market. Heuristics and Biases The status quo bias is a cognitive bias for the status quo; in other words, people tend to be biased towards doing nothing or maintaining their current or previous decision. The status quo bias can lead to another cognitive heuristic, known as anchoring, which describes the common human tendency to make decisions based on an initial ‘anchor’. We prefer relative thinking to absolute thinking. Anchoring is likely to cause fundamental analysts to underreact, for example to earnings announcements. Representativeness leads people to predict future events by looking for familiar patterns and taking a short history of data and assuming that future patterns will resemble past ones. Representativeness leads analysts to believe that observed trends are likely to continue, and causes trend following by technical analysts and overreaction among fundamental analysts. Artificial Stock Market Assume that the cumulative impact of relevant news on a stock follows a geometric random walk. Market participants consist of fundamental analysts and technical analysts. The fundamental analysts underreact to news, but overreact to a series of good or bad news; whilst the technical analysts only consider the price, and follow the trend. Results Mean log return (P&L) per analyst Statistics of price log returns Kurtosis of price log returns Autocorrelations of price log returns Conclusions Whether a fundamental analyst, or a technical analyst, it pays to be in the majority, ideally of about 60 per cent, whilst being in a small minority is the least profitable position to be in. The artificial stock market replicates mean returns, the standard deviation of returns, the absolute returns correlation and the squared returns correlation of a real stock market, but failed to accurately replicate the skewness, kurtosis and autocorrelation of returns. This implies that the model has failed to capture some of the dynamics underlying the process of price formation. For each statistic, the range exhibited by real stocks, and the range of proportions of technical analysts in the artificial stock market that replicate a real stock

![Toru Yamamori [University of Cambridge]](https://cdn1.slideserve.com/3537992/slide1-dt.jpg)