Download

1 / 36

360 likes | 503 Views

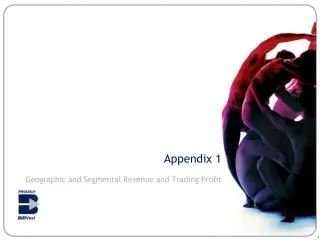

Appendix 1. Geographic and Segmental contributions to Revenue and Trading Profit . Geographic Revenue and Trading Profit splits. Appendix 1. F2008. F2007. SA. Revenue. Asia Pacific. UK & Europe. Trading Profit. Africa. Contribution: Foreign operations

E N D

Appendix 1 Geographic and Segmental contributions to Revenue and Trading Profit

Geographic Revenue and Trading Profit splits Appendix 1 F2008 F2007 SA Revenue Asia Pacific UK & Europe Trading Profit Africa • Contribution: • Foreign operations • SA operations Note: IFRS compliant

Segmental contributions to results Appendix 1 Segment Bidfreight Bidserv International Foodservices Bidfood (SA) Bid Industrial & Commercial Bidpaper Plus BidAuto Corporate

Appendix 2 Detailed segmental results

Bidfreight – Bulk Supplies Appendix 2 Bidfreight Bidfreight • Bidfreight Terminals • Bulk Connections, Island View Storage, Bidfreight Port Operations, Rennies Distribution Services, SACD Freight, SA Bulk Terminals, Naval • International Clearing and Forwarding • Safcor Panalpina • Marine Services • Manica

Bidfreight – Bulk Supplies Appendix2 Results • SABT & Bulk Connections, together with strong contributions from IVS, Marine and BPO, drive a 16% rise in profits • Bulk-category Capex on facilities pays off in recognition by customers, in pricing and in throughputs • Protracted NPA lease negotiations + Transnet unreliability are prejudicial to BVT & national interest • Manica Namibia excluded as of 1 July 2007 – forms part of new Bidvest Namibia • Safcor Panalpina: reduced pre-tax profits, mix reduces margin, higher financing costs • Marine: pre-tax profits, including associates, up 27% driven by containerised exports and exports of vehicles. Additional ships agencies being sought from shipping lines to diversify revenue stream • RDS: a disappointing result but re-focus (disruptive) during F08 will pay off in future years; a new Pallet rental segment established • SACD: profits up 10%, assisted by customer win + additional import volume from quality customers; export volumes pick up whilst overall imports slow; depot capacity constrained Rm Trading Profit 3.1% 3.1% Trading margin

Bidfreight – Bulk Supplies Appendix 2 • IVS: profits up 7% ; new-build of destroyed tanks in progress; maintenance work substantially increased; liquid bulk storage demand at high level • Bulk Connections: upgrades to world-class norms results in substantially increased volumes and good customer service levels; profits double; prolonged Ports Authority lease negotiations frustrates further expansion; • SABT: Maydon Wharf now most efficient terminal of its kind in South Africa and a terminal of first choice; profits up 116%; poor Transnet Rail services impede optimal efficiencies • BPO: profits up 28% as revenues accelerate ahead of budget; volumes slowed Q4 in products such as cement, rice, pulp & paper; steel volumes low; bulk expected to increase its contribution in F2009 • Naval: profits flat due to low coal, citrus, aluminium volumes; strength of Metical a negative; termination of a ferrochrome contract will effect F2009 result • Manica: territories now include SA, Botswana, Malawi, Zambia and Zimbabwe. Profits substantially down, with only Botswana holding its own; region remains variable from a trading point of view Strategic imperatives & prospects • Outlooks vary but the consolidated Freight segment is budgeted to produce profit growth in F2009 at a rate below that of F2008 • Organic growth is immediate focus together with tighter debtor and cash management • Agreement with Ports on new facilities needed to accommodate higher throughputs/ profitability • The Bulk businesses depend on unstinting support from Transnet Freight Rail • Fuel & power costs could place pressure on margin; customer resistance to price increases • Substantial prior capex will continue to pay off, particularly in Bulk • Re-built IVS capacity on stream but higher depreciation likely to restrain the operating result

Bidserv – High Flier Appendix 2 Bidserv • Full range of outsourced services including: • Cleaning • Laundry • Hygiene • Security • Interior and exterior landscaping • Aviation services • Industrial workwear • Travel • Banking and foreign exchange services • Office automation • Supply chain integration • E-procurement and online travel

Bidserv – High Flier Appendix2 Results • Record level of profitability • TMS, Industrial Products, Konica-Minolta, BidAir, Bidvest Bank notable outperformers • Prestige: labour-intensive contract cleaning gross profits by 13.5% as qualitative advantages enhances market share • TMS: profits up 58% as R70m capital investments reinforce specialist cleaning offering for major industrial customers • Laundries: profits up 14% in a price-sensitive market • Steiner: expenses associated with infrastructure improvements resulted in profits easing by 7% • Security: return to profit following strikes but below budget • Global Payment Technologies: in line with prior year. Profits typically cyclical, aligned with banking customer projects • Top Turf: 18% growth in profits masks pockets of underperformance but revived management team set on improving profitability Rm Trading Profit 13.1% 12.6% Trading margin

Bidserv – High Flier Appendix 2 • Industrial: exceptional result with profits up 40%; facilities strengthen competitiveness • My Market: e-procurement solutions, cutting edge travel engine, and group-wide procurement savings make this erstwhile greenfield business comfortably profitable • Office – Konica Minolta & Oce: 45% rise in profits, market position in office automation strengthened in a tightening economy • BidAir: profits +45%, with lounges and cargo performance pleasing. ACSA license effective 1 March 2008 • BidTravel: profits +20% as business responds to prior management actions to right-size for new realities; brands rationalised; manual processes now automated • Bidvest Bank: 41% rise in bank profits assisted by new forex products; Master Currency exceeds expectations • Hotel Amenities: profits +16% on the back of improved hotel occupancies and new customers • Strategic Imperatives and Prospects • Critical mass in soft services plus market reach will enable Bidserv to once again grow profits in a less favourable economic climate • BidAir to focus on realising return on capex spent gearing up for ACSA license • TMS expected to substantially increase profits and returns • Hotel Amenities contract win from a major hotel group opens up Africa potential • Further upside expected in BidTravel following right-sizing and productivity initiatives

Bidvest Europe – Thirst for Foodprofits Appendix 2 Bidvest Europe • 3663 (UK) • Deli XL Netherlands • Deli XL Belgium • Horeca (Middle East)

Bidvest Europe – Thirst for Foodprofits Appendix 2 Results • Total profits up 8% to £59.1m. UK trading profit flat at £46.7m, Netherlands +31% to €16.9m (£12.4m), Belgium +32% to €4.1m (£3m), and Horeca UAE +51% to AED1.5m (£0.2m). Sterling average exchange rate €1.36 (€1.48). Deli XL combined now over quarter of total profits • Accelerating price inflation a feature across all markets; food and fuel inflation well above CPI • Deli XL Netherlands: +31% (€16.9m profit vs. €12.9m); revenue €730.5m (+6%); ROS 2.3% (1.9%); cash generated by operations €25.4m; labour market tight (wage pressures); intensified institutional competition but market share gained in hospitality; small bolt-on’s • Deli XL Belgium: +32% profit (€4.1m) on €239.8m revenue (+14%); ROS 1.7% (1.5%); Kruidenier & Sodexo add to volumes Rm Trading Profit 2.6% 2.5% Trading margin 12

Bidvest Europe – Thirst for Foodprofits Appendix 2 • Horeca: £0.2m profit; ROS 2.6%. Sales in local currency rise 64%; oil induced boom fuels inflation; cost efficiencies & stricter credit policy pays off • 3663: sales 3% up at £1.586bn (6.8% like-for-like excluding MOD); profits flat at £46.7m; ROS 2.9% ; cash generated by ops £63m; capex £31m vs. £25m; overhead 2% below F2007 – tight controls • Multi-Temp grows profits 16%; CD now profitable (£1.1m) • Positive MOD exit • Field sales re-organisation realises substantial cost savings • Pass-thru of inflation + profitable pre-emptive buying will also flow into F2009 • Frozen Fresh & Chilled & Multi Temp combined in single Wholesale business. • Barton Meat under review, with alternatives being explored Strategic imperatives & prospects • GDP growth in all markets decelerating, whilst CPI increases; • Margin to be preserved wherever possible • Balance sheet capacity to profit from inflation • 3663 likely to benefit from customer consolidating their suppliers to reduce costs. • 3663 Genesis IT project to roll-out fully F2009 • 1 July 2008 Dutch smoking ban in public places – impact indeterminate • Bidvest Europe budgets to once again grow profits in F2009 13

Bidvest Asia Pacific – Bonzer Wicket Appendix 2 Bidvest Asia Pacific • Bidvest Australia • Bidvest New Zealand • Angliss Singapore • Angliss Hong Kong and China

Bidvest Asia Pacific – Bonzer Wicket Appendix 2 Results • Largely organic growth in Australia, record returns – 3.5x increase in profits since F2002 • New Zealand performs well in a slackening economy • Angliss (HK & Singapore) proves its worth – first full year contribution exceeds expectation • Australia:sales up 17.5% to A$1,429bn (real growth 10% after food inflation), profits up 25% to A$55,7m; ROS 3.9% vs. 3.7%; GDP growth slows sharply, labour market remains tight, cost pressures • Foodservice sales up 13.5%, profits up 36%; all branches comfortably profitable; facilities and people investment continues; full national coverage attained • Despite its developmental status, Hospitality is a net contributor and enhances overall offering • QSR profits up 50%, assisted by transfer of Subway business; high service levels underpin sustainability in a slowing market Rm Trading Profit 3.9% 3.8% Trading margin 15

Bidvest Asia Pacific – Bonzer Wicket Appendix 2 • New Zealand: sales up 18% (organic) to NZ$384m (real growth 10%), profits up 17% to NZ$16,8m; ROS 4.4%; independent trade sales growth exceeds national accounts growth; NZ$17m spent on capital assets; rising food prices help neutralise higher operating costs in a moribund economy • Fresh sales grow 40%, profits up marginally – management continues to finesse this business for optimum effectiveness • Foodservice profits up 14%; substantial market share gain as total market declines; value-add + service + delivery size focus • Logistics profits double in first full year; valuable complement • Angliss:First time annual trading profit of R97m • Singapore: Sales of S$31,6m, profits of S$10,7m, ROS of 3.3% (incl. forex gains) • Hong Kong & China: Sales of HK$1,4bn, profits of HK$45,5m, ROS of 3.3% • Strategic imperatives & prospects • All markets share similar cost challenges • Australia: small bolt-ons to contribute to F09; cost pressures will impinge on margin but real growth budgeted • New Zealand: strongly positioned in a difficult economy, real growth budgeted • Angliss: bolt-ons; Malaysia foodservice unit start-up; growth opportunities being pursued in Macau and Mainland China 16

Bidfood – Inflating times Appendix 2 Bidfood • Caterplus • Bidfood Ingredients • Speciality

Bidfood – Inflating times Appendix2 Results • Ingredientscopes well with the twin forces of escalating food price rises and raw material shortages • Chipkins Bakery Supplies improves profitability substantially; strong performance from Crown National Group; encouraging result out of NCP Yeast • Divisional restructure successful • Excellent expense control • Caterplus:net revenue up 17% and trading profits up 19%; strict credit policy has reduced volumes but pays off in substantially reduced trading risk and reduced debtors book; restaurant bankruptcies escalate; higher average basket values/spend with good customers • Increased symmetry between buying & sales • Higher gross margin due to buying in ahead of price rises or stock shortages • Theft of inventory is a headache, requiring vigilance Rm Trading Profit 8.1% 7.3% Trading margin

Bidfood – Inflating times Appendix 2 • Speciality: Patleys grew revenue by 22% and trading profits by 28% but diminishing disposable incomes placed increasing strain on trading as the year progressed; price increases pushed through but agency volumes fall as a consequence; own-brand Goldcrest makes excellent progress as do sales to leading retailers; approaching the market with vigor through promotions, stock availability, customer awareness Strategic imperatives & prospects • Deflation (outright reduction in prices) is a possibility after a rapid run up in food inflation. • Deliberate policy to reduce volume in Caterplus rather than risk bad debts may impact rebates • Bidfood will emerge from these taxing trading times far stronger than competitors and fully expects to achieve yet another record result in F2009

Bid Industrial and Commercial Products – Levelling Out Appendix 2 Bid Industrial and Commercial Products • Voltex Electrical Wholesaling • Stationery and Furniture • Packaging Closures • Vulcan Catering Equipment

Bid Industrial and Commercial Products – Levelling Out Appendix2 Results • Profits at record high but rate of growth moderates after a stellar run • Voltex: profits up 5% in a tougher trading environment; copper price recovery in Q4 enabled a partial clawback of opportunity costs in H1; debtor collection drive; both existing and new electricity savings initiatives and products are a focal point • Stationery & Furniture: a better Q4 enabled profits for the year to grow by 7%; cash generation particularly pleasing • Waltons profits up 16%, with Gauteng particularly strong; “back-to-school” sales improved; refurbishments assist growth • Kolok’s trading results improved in H2 with the result that the profit decline for the year was limited to 19%; focus on eliminating low-margin business; expenses contained despite costs of store re-positioning; • Furniture achieved pleasing overall profit growth. The Seating business continues to increase its mix of imported component to remain competitive; market exposure ramped up for all operations Rm Trading Profit 8.7% 8.4% Trading margin

Bid Industrial and Commercial Products – Levelling Out Appendix 2 • Packaging: • Afcom GE Hudson profits up 19%. Higher market share due to new products on offer; factory consolidation continued; strategy to import is bearing fruit • Buffalo Executape profits up 7% despite raw material price pressures - smart purchasing has limited full effects and retained customer loyalty • Vulcan: a broadly flat result, with pressures coming from raw material costs, imported competition, and lately a buoyant used market for catering equipment • Strategic imperatives & prospects • Voltex has both challenge and opportunity: challenge in the form of a declining residential/commercial market and opportunity in the form of infrastructure investment on a broad front, together with a number of energy efficiency initiatives • Office products are facing a pressure in a weakening retail market • Vulcan will capitalise on modernized facilities and new products • Overall growth expected to be modest in the short term

Bidpaper Plus – You win some, you lose some Appendix 2 Bidpaper Plus • Printing and related • Personalisation and Mail • Printing and Conversion • Sales and Distribution • Stationery Distribution • Alternative Products • Packaging and Label Products

Bidpaper Plus – You win some, you lose some Appendix2 Results • Broadly flat results due to absence of profitable Lithotech ad-hoc export project business in the period • Business remains solidly cash generating • Laser & Mail continues to offer profitable opportunity • Lufil and Rotolabel integrated into Labeling & Packaging • Croxley re-branding completed, growing market acceptance • Input cost pressures a constant throughout • E-mail connection business has a fabulous year Rm Trading Profit 12.4% 11.4% Trading margin

Bidpaper Plus – You win some, you lose some Appendix 2 Strategic imperatives & prospects • Lithotech will continue to generate cash and provide necessary expansion funds for e-products • Laser & Mail has enjoyed new contract wins • Expansion of Labels & Packaging range • Stationary expected to yield higher returns following recapitalisation of Siveray/Statmark • Intensified push to secure more export business • Confederation Cup & 2010 World Cup – proactively seeking print opportunities

BidAuto – Diversification Dividend Appendix 2 BidAuto • Motor retail • BMW/Mini, General Motors, Land Rover/Volvo, Mercedes-Benz, Chrysler/Jeep/Dodge/Mitsubishi, Nissan/Fiat/Alfa/Renault, Peugeot, Toyota/Lexus, Volkswagen/Audi/Seat, Suzuki, Chery, Foton • Burchmores • Import and Distribution • McCarthy Vehicle Imports, McCarthy Heavy Equipment, Yamaha Distributors • Financial Services • McCarthy Insurance Services, McCarthy Finance and McCarthy Fleet Solutions • Budget Car and Van Rental • Support Services and Corporate Services • McCarthy Call-a-Car, Club McCarthy, Eliance

BidAuto – Diversification Dividend Appendix2 Results • Considered strategy to diversify away from car retailing bolsters result as boom turns to abrupt bust • Full-year contribution from fleet management acquisition Viamax, heavy equipment and truck sales, used cars, and exposure to leading OEM brands for parts and service business partly supported profits but like-for-like profit declined 26% • Total vehicle sales down 3% to 86 616 units, with used vehicle sales up 10% to 42 182 units and new unit sales down 12% to 44 434 units • National Credit Act, higher finance charges, and worsening affordability resulted in substantial market weakening as the year progressed – and likely to worsen into F2009 • Disconnect between OEM aspirations and immediacy of harsh dealer economic realities • R300m in capex + staff retention and training focus underscores BidAuto’s intention of remaining a leading and sustainable player Rm Trading Profit 4.0% 3.9% Trading margin

BidAuto – Diversification Dividend Appendix 2 • New and used car price differentials widen, with used car prices little different over five years • Burchmores auction volumes and bargain-retail a major success • Chinese mini-bus and pick-up sales disappointing but exclusive Chery arrangement off to a promising start • Budget Car Rental secures third place in the market, boosted by innovations • Yamaha product acceptance remains healthy and despite reduced profits returns were highly satisfactory • Working capital management improved during H2 from earlier inflated levels • Strategic imperatives & prospects • Motor retail market likely to bottom out 25% below 2006 peak • Retail cost bases out of line with reduced volumes – margin pressure • Affordable, fuel-efficient and quality used product holds promise • Fleet Solutions contribution to grow, good returns, fleet renewals • Parts and service revenues a partial compensation for lower new volumes • Crime is a pressing and costly concern • Selected openings of new dealerships will continue (e.g. Suzuki’s return to SA plus additional Ford/Mazda outlets) • Franchise potential for Chinese brands • BidAuto will hold profits at F2008 levels in F2009

Corporate Services – Bricks & Mortar Appendix 2 Corporate Services • Bidvest Namibia • Bidprop • Ontime Automotive • Investment, other income & corporate costs

Corporate Services – Bricks & Mortar Appendix2 Results • Strategic property holdings worth significantly more than stated book value • New property developments for BidAuto, Bidpaper Plus, and Bidfood • Namsov reversed H1 losses on better catches and pricing • All Namibian assets folded into Bidvest Namibia with a view to listing later in calendar 2008 • Ontime Automotive hit by restructuring, fuel price increases, and termination of loss-making volume distribution contracts; Parking Solutions secured a major tender; Prestige Vehicle Distribution traded better than budgeted • Ontime will nevertheless show a sharp reversal of losses in F2009 • 2010 World Cup commercialisation plans in full swing and a minority interest was acquired in MATCH Hospitality AG, a FIFA appointed hospitality services business Rm Trading Profit 11.1% 11.1% Trading margin

Appendix 3 Effects of economic drivers by segment

Economic influencers – various outcomes Appendix 3 * Bidvest is indifferent to any particular ZAR rate of exchange - relative stability is far preferable though to the extremes in valuation that have eventuated periodically

Appendix 4 Historic Performance

Historic Performance -Year to June Appendix 4 5.1% 5.1% 5.1% 5.1% 5.2% 5.2% 5.2% 5.2% 4.6% 4.6% 4.9% 4.9% 4.3% 4.4% 4.3% 4.4% 4.5% 4.5% 4.7% 4.7% 18% CAGR over 5 years 18% CAGR over 5 years

Appendix 5 The Bidvest Business Model

The Bidvest Business Model Appendix 5 An operationally active investment holding company whose core competence is the management of a balance of cash generative and growth businesses Market-leading service, trading & distribution businesses Implementation Strategy • Businesses actively & successfully managed • Decentralised, focused business units • Market leaders in distribution channels: • Critical mass for sourcing & funding • Reaching common customers • Tying the customer in • Own the cash flows • Control distribution channels • A balance of mature & growth businesses • Funds allocated across asset base according to proven return criteria • Vigorous capital management - cash used from mature businesses to fund growth businesses and acquisitions • Identifying acquisitive value • A team of operationally strong, entrepreneurial owner-managers: • Financial disciplines(working capital, managing sustainable returns) • Corporate office frees up businesses to perform • Financial integrity • Proven ability to correct underperformance (incl .organic growth record from acquisitions) • Proven ability to create value in businesses Management Focus