Download

1 / 86

860 likes | 996 Views

NS3040 Winter Term 2013 Eurozone Crisis. Outline. Part I – EU/EZ Regional Issues Overview of the EU/EZ -- Macroeconomic Patterns Prelude to the Crisis Current Situation Part II – Country Analysis Greece – Probable EZ Exit Spain – Economic Free-Fall Italy – Recession and Austerity

E N D

Outline • Part I – EU/EZ Regional Issues • Overview of the EU/EZ -- Macroeconomic Patterns • Prelude to the Crisis • Current Situation • Part II – Country Analysis • Greece – Probable EZ Exit • Spain – Economic Free-Fall • Italy – Recession and Austerity • France – Wrong Turn With Hollande? • United Kingdom – Lingering Output Gap • Russia – Increased Vulnerabilities (if time) • Part III -- Final Assessments – • Will the Euro-zone survive? • Implications for security

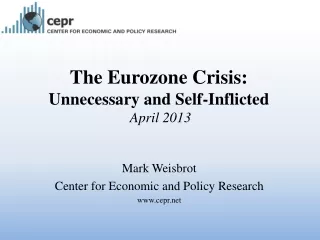

Change in GDP Levels from Precrisis Peak/y-y Growth Q2, 2012

Euro-Zone Crisis Overview • The current crisis in the Euro-zone can be easily traced back to a fundamental flaw in the Zone’s economic model: • The model concentrated monetary policy in the European Central Bank (ECB) while leaving fiscal policy to individual member states – inherently unstable arrangement • It denies member states monetary policy levers with which to help their recoveries • Also makes deficit-funded stimulus harder as monetary policy can be used to keep borrowing costs low. • The EZ is not an optimal currency area – the common monetary authority is likely to act in ways that help some countries but not others. • The ECB has pursued tight monetary policy that may prevent inflation in high-growth states like Germany but could also be worsening the recession in Greece, Spain and other struggling states. • Rigid labor markets prevent adjustments common in the United States. • Also Europe still lacks key elements necessary for a common currency to work – Joint European Bank Regulator and a system for dealing with troubled financial institutions, unconstrained independent, central bank

Lead-up to the Euro-zone Crisis I • Stability and Growth Pact rules broken repeatedly • Italy was the worst offender – regularly broke the 3% annual borrowing limit • Germany the first big country to break the 3% rule • After Germany France followed • Of the big economies only Spain kept within limits (until the 2008 financial crisis hit) • Greece in class of its own • Never stuck to the 3% target and • Manipulated its statistics to look good and get into the euro in the first place • Problem only discovered two years ago

Lead-up to the Euro-zone Crisis II • The big build up of debts in Spain and Italy before 2008, was not by the public sector • Instead it was the private sector – companies and mortgage borrowers where were taking out loans • Interest rates had fallen to unprecedented levels in Southern European countries when they joined the euro • That encouraged a debt-fueled boom • The increased debt helped finance increased imports by Greece, Spain, Italy and France • Meanwhile Germany became an export power house after the EZ was set up in 1999 selling much more to the rest of the world (including southern Europe) than it was buying as imports

Lead-up to the Euro-zone Crisis III • Meant Germany earning a lot of surplus cash on exports – much of which ended up being lent to southern Europe • Bad debts only part of the problem in Italy and Spain • During the boom years, wages rose in the south (and France), but German unions agreed to hold their wages steady • Now, Italian and Spanish workers face a huge competitive price disadvantage • Loss of competitiveness main reason why southern Europeans have been finding it harder to export than Germany • Most of the periphery’s debt and banking problems trace back to their lack of competitiveness.

Euro-zone Crisis I • In sum: -- government borrowing • Which has ballooned since the 2008 global financial crisis • Had very little to do with crating the current Euro-zone crisis in the first place – especially in Spain (Greece another story). • So even if government’s don’t break the borrowing rules this time – won’t necessarily stop a similar crisis from happening all over again • Spain and Italy now facing severe recessions because • No-one wants to spend • Companies and mortgage borrowers are too busy repaying their debts to spend more • Exports are uncompetitive • Now governments whose borrowing has exploded since the 2008 financial crisis – have agreed to drastically cut back as well • Two possible courses of individual country action – neither very appealing

Euro-zone Crisis II 1. Cut spending – pretty sure to deepen the recession • Probably means more unemployment (already well over 20% in Spain) • May push wages down to more competitive levels – history suggests this is very hard to do. • Even so, lower wages will just make people’s debts even harder to repay • Meaning they are likely to cut their own spending even more, or stop repaying their debts • Lower wages may not even lead to a quick rise in exports if other European economies markets are in a recession too • In any case, can probably expect more strikes and protests and more nervousness in financial markets (causing even higher interest rates) about whether you really will stay in the euro

Euro-zone Crisis III 2. Don’t cut spending • Risks a financial collapse • Amount borrowed each year has exploded since 2008 due to economic stagnation and high unemployment • But if economies are chronically uncompetitive within the euro • Markets liable to lose confidence in you – may fear that economies simply too weak to support increasing debt load • Meanwhile other European governments may not have enough money to bail you out, or are legally/politically constrained from doing so • European central bank has said its mandate doesn’t allow it to provide unlimited bond purchases • Clearly only way out of crisis is a coordinated approach involving creditors and debtors and international institutions such as the IMF

Euro-zone Crisis IV • For its part, the European Central Bank (ECB) is making attempts to ease the funding pressures on indebted member countries • The bank is signaling its readiness to buy the bonds of stressed sovereign governments • However, the ECB will by the bonds only of countries that have applied for help from euro zone rescue funds and accepted the conditionally attached • The use of the ECB’s balance sheet to ease funding pressures could be a game charger for the euro-zone, although it will only buy time • However financial market fragmentation still a major problem • Structural issues and competitiveness will still need to be addressed for growth to resume • EIU forecasts Euro-zone GDP to contract by 0.6% in 2012 and grow by only 0.4% in 2013.

Part III Country Analysis • Greece – Probable EZ Exit • Spain – Economic Free- Fall • Italy – Recession and Austerity • France -- Wrong Turn Under Hollande? • United Kingdom -- Lingering Output Gap • Russia – Increased Vulnerability (if time permits)

Greece: Probable EZ Exit I • Greece is in a technical depression – contraction in real GDP of over 10% lasting more than two years • Greece’s real GDP has contracted 23% from its peak in Q3 2006 to Q1 2012 • While Greece has a reputation for not having made any effort to meet terms of its bailout, significant austerity measures have been implemented and will weigh heavily the next few years • The economy is predicted to decline 7.9% in 2012 and 8.4% in 2013 • Wages have fallen by up to 40% in the public sector and up to 30% in the private sector from previous levels • Pensions have been cut by as much as 30% • As the new government is forced to find additional austerity measures to meet terms of its bailout program, the negative impact on consumption will be significant • This will be compounded by unemployment rates of nearly 23% in early 2012

Greece: Probable EZ Exit II • Retail sales volumes declined by 10% in 2011 and by 13.8% y/y in Q1 2012 • The political situation in Greece is highly unstable with a series of coalition governments likely for the near future • The new coalition and the troika (the European Commission, the ECB, and the IMF) may find a compromise regarding the second bailout package because it is in both sides' interest to do so. • However, Greece will likely continue to go through cycles of elections, additional austerity, social unrest and new elections. • A good chance that eventually the electorate will choose a government that sees an EZ exit as a more attractive alternative – possibly as early as the spring of 2013 • Many U.S. firms and banks already making contingency plans for Greek exit from the EZ • Three quarters of the German public feel Greece should leave the EZ

Spain: Economic Free-Fall I • Spain is experiencing the fall-out the bursting of a real estate bubble after a decade of excessive leveraging • Construction and real estate loans grew from 10% of GDP in 1992 to 43% in 2009 and amounted to about 37% of GDP at the end of 2011 • Spanish banks funded their increasing exposures largely from external sources during the period of high global liquidity and low interest rates – rather than through the mobilization of savings • The freezing of wholesale markets and the onset of the Euro-area debt crisis exposed Spain’s vulnerabilities from accumulated domestic and external imbalances • Despite significant consolidation and loss recognition, banks’ access to wholesale funding markets remains limited. • Banks are exposed to further losses on their loan portfolios, notably to the real estate and construction sectors due to weak macroeconomic environment • The deterioration in markets’ perception of sovereign and bank risk has further increased pressure on Spanish banks ability to raise funds – currently large capital outflows from the banks.

Spain: Economic Free-Fall II • Compounding bank problems, the Spanish economy is firmly stuck in recession • The economy is expected to contract by 1.7% in 2012 and a further 2.4% in 2013 • Unemployment continues to increase with joblessness nearly 25% • The South of Spain has especially high rates with over one-third of the labor force unemployed • Youth unemployment is well over 50% with out-migration accelerating • As a result of these developments the country is caught in a vicious cycle: • The government has used taxpayers money to rescue the banks – wakening the public budget position • Increasingly risk adverse banks have stopped lending to many businesses desperately in need of capital • Cutback in credit undermines the economy and thus the government budget position further placing more public borrowing demands on the banks

Spain: Economic Free-Fall III • Spain seems unlikely to be able to reduce its budget defect from the 8.5% GDP (2011) much less met its 2012 target of 5.3% • Debt will increase from almost 69% GDP in 2011 to over 96.5% in 2013, and considerably more if the government has to step in with further bailouts for the banking sector; • Spain has nationalized one large bank, Bankia, and established a “bad bank” for winding down banks with no future – good chance it will sustain significant losses. • At present, 3 possible scenarios: • Base case (60%). A EZ bailout for banks fails to regain market confidence and in absence of growth: • The sovereign needs a bailout from the EZ too. • This buys some time but not enough for Spain to implement structural reforms and return to growth. • When the bailout runs out, Spain restructures its debt (2015)

Spain: Economic Free-Fall IV • Upside (15%): A proactive Spanish bank recapitalization is accompanied by • A policy shift at the EU level to focus on growth rather than austerity • Further liquidity measures by the ECB and government bond purchases by the ECB and/or EFSF • Consequently a bank recapitalization helps to restore investor confidence in Spain and a full blown bailout for the sovereign is avoided • Downside (25%) The Spanish government resists a bailout and, in the meantime, • Contagion takes the crises well beyond Spain to Italy and the core EZ countries • Rather than throw more good money after bad, EZ leaders opt to use the EU-IMF firewall to support an orderly sovereign debt restructuring for several countries, including Spain and to facilitate the exit of some EZ countries in late 2012 at the earliest. • Conclusion: Spain not on life support yet, but patient won’t recover without it.

Italy: Recession and Austerity I Italy’s economy has a number of important strengths: • Italian households have solid balance sheets, and private savings have traditionally been high • Private debt at about 125% of GDP is among the lowest in the euro area. • The public sector, despite having one of the largest levels of debt in the world also has large assets • With net foreign liabilities at around 20% of GDP, Italy’s net international position is more favorable than in other euro area periphery countries • The country’s current account deficit is relatively low • Italy’s exports, though lagging in terms of high value-added content, are among the most diversified in the world. • Despite these strengths, • Italy’s long-run economic performance has lagged behind its peers, • While in the short-run the country is experiencing a serious economic down-turn.

Italy: Recession and Austerity II For the longer-term: • Italian growth averaged less than 0.5% in the last decade • Compares with 1.0% in the EU15 and 1.25% in G7 countries • An important source of growth, total factor productivity (TFP) was negative • Potential growth is estimated to have stalled in recent years or even turned negative. • In the absence of major changes to trends in productivity employment, and investment, potential growth is likely to remain close to zero over the medium term. • Italy’s weak growth performance results from of structural factors • 1. Limited competition – regulatory rigidities have limited competition and kept rents high especially in non-tradable sectors • This has adversely effected the business environment increasing costs for the sectors that need to compete globally and eroding the competitiveness of the economy • With firms unable to grow and benefit fully form economies of scale, the efficiency of the productive system has remained low, innovation has been limited, specialization has not moved sufficiently toward more high-skilled sectors --has led to a loss in export market shares

Italy: Reforms and Austerity III • 2. Labor market rigidities – mirroring these problems, the labor market is marred by • low labor participation, • dualism, and • low educational attainment • 3. Weak public services – deficiencies in the product and labor markets have been accentuated by the • high tax burden, coupled with inefficient public spending, • a inefficient legal system, • limited FDI penetration, • large regional disparities, and • a sizeable underground economy • To overcome these impediments to growth the government has recently undertaken a wide range of structural reforms in product and labor markets.

Italy: Recession and Austerity II • For the shorter-term • Italy has been in a recession since the middle of 2011 • In Q1 2012 the economy contracted (0.8%) for a third strait quarter. • The contraction was led by sharp falls in consumption and investment as concerns about the fiscal outlook and euro area crisis depressed confidence and tightened credit conditions • Household income continued to decline in 2011 while consumer sentiment fell below levels in 2008-09 • The unemployment rate rose to 10.2% in April 2012 – its highest level in more than ten years, with youth unemployment at 35%. • Italy came under intense financial pressures in late 2011, as the euro area crisis pushed 10-year government bond yields above 7 percent. • To restore confidence the Monti government in December announced a third fiscal consolidation plan, bringing the total adjustment for 2012-14 to around 5% of GDP • Still bond markets remain nervous

Italy: Recession and Austerity IV • The economy is expected to continue contracting though the year due to needed fiscal consolidation, tight financial conditions and global slowdown. • IMF forecast – GDP will decline by 1.9% in 2012 and another 0.3% in 2013 • The government’s fiscal adjustment program (austerity) is estimated to reduce growth by 1.5% in both 2012 and 2013. • With revenue increases making up the bulk of the adjustment, growth in disposable income and household spending is expected to remain sluggish. • Reflecting growing demand from trading partners, exports are projected to expand moderately in second half of 2012 • However given the drag from fiscal consolidation and tighter credit, the recovery will lag the rest of the rest of the region • Unemployment projected to reach 11 percent in 2013

Italy: Recession and Austerity V • Assessment: • Monte administration represents the best chance and hope for Italy to resolve its crisis and restore longer term growth • Problem is that the economy is still contracting, given front-loaded fiscal austerity, a still-strong euro, a credit crunch and policy uncertainties • Fears that Italy will follow Spain in requiring a bailout are premature – for now • Austerity measures have eroded Monti’s popularity and his government is less cohesive than several months ago • Against collapsing business and consumer confidence, there is little the government can do given the budgetary constraints it faces – its longer-term structural reforms are increasingly in jeopardy • The uncertainty surrounding the euro-area bailout of Spain’s banking sector is having a knock on effect in Italy, even though its housing market and its banking sector suffer none of the huge defects now visible in Spain

Italy: Recession and Austerity VI • Negative trends are developing • Monti government is being increasingly attacked from both the left – unions are becoming increasingly restless and militant, with more and more strikes and street demonstrations – and increasingly the right • In regional elections a new party led by former comedian Beppe Grillo, was the key beneficiary of the increasing anti-incombent sentiment • His Five-Star Movement is better known for what it is against – traditional parties and politics, austerity, the euro – than for any constructive policies • In this context, fearing that supporting austerity and reform will further reduce its popularity, Berlusconi’s party is now starting to attack the government it had been supporting • At this point not clear the Monti government will survive until the official election in spring 2013 • If this happens, Berlusconi, Five Star Movement and other parties may run in the 2013 parliamentary elections on an anti-euro program

Italy, Recession and Austerity VII • More ominously, many political and economic groups are pushing for Italy to leave the EZ and return to the lira. • These groups include Berlusconi who is using the euro as a way to blame the country’s problem on the center-left government that signed off on Italy joining the euro • The hard right Northern League which represents the interests of small, medium sized and even some larger business is a major euro-skeptic party. • Economic interests driving the movement to return to the lira are clear: many industrial and manufacturing businesses in the traded sector are struggling at the real appreciation in Italy has led to export-market share loses and a flood of import competing goods from abroad • Also many business owners and firms have large euro denominated foreign assets stashed – after decades of capital flight and tax evasion – in bank accounts abroad while their domestic and foreign liabilities are also in Euros. • If Italy were to exit the EZ, these foreign assets in Euros would have a great capital appreciation against the depreciated new lira,

Italy: Recession and Austerity VIII • While their liabilities would be conceivably converted into depreciated Italian liras – resulting in a massive increase in wealth – has happened previously in similar situations • Of course a euro exit would represent a capital loss for lower and middle income households that have most of their savings in local banks • However many individuals would benefit from the increase in growth and jobs that a return to the lira would entail • Not yet a majority in Italy pushing for an exit from the EZ • Still support for euro membership falling: • Since 2007 support for euro membership has fallen from 67% in 2007 to 53% this spring • In 2007, 58% of Italians had a positive image of the EU, but by 2012 that had fallen to 30% -- falling 12% in 2011-12 alone. • However if Berlusconi and other forces were to obtain grater power things could change quickly • Italy is already telling Germany that it has to show much more flexibility on the EZ crisis resolution or anti-euro forces could take charge.

France: Wrong Turn Under Hollande? I • Stronger than expected performance at the turn of 2011-12 ensured France not only avoided a technical recession, but also outperformed all its EZ peers • However fiscal rebalancing and the re-escalating EZ sovereign debt crisis will weigh on output through 2012 • Available Q2 survey data signal contracting private sector activity with the manufacturing PMI falling to a three year low – along with a sharp fall in domestic- and export-oriented new orders • French government cut its 2012 growth forecast from 0.5% to 0.3% and risks missing this. • Similarly its forecast of 1.2% growth in 2013 may prove too optimistic; the IMF expects only 0.8% • Labor costs are considerably above those in Germany, and weak growth in EZ periphery puts pressure on the balance of payments • A tight budget and slow growth will restrict the new government’s ability to cope.