Download

1 / 13

470 likes | 966 Views

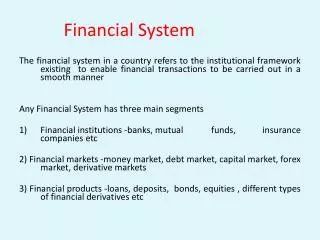

FINANCIAL SYSTEM. FUNCTIONS. Collection of savings & their distribution for investment. Stimulating capital formation. Accelerating the process of economic growth. Hence a linkage between savers and investors.

E N D

FUNCTIONS • Collection of savings & their distribution for investment. • Stimulating capital formation. • Accelerating the process of economic growth. • Hence a linkage between savers and investors. • Made up of all those channels through which savings become available for investment.

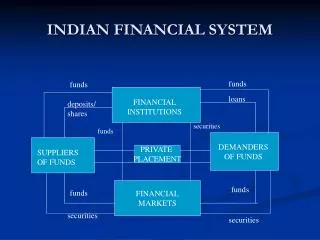

ORGANISATION OF FINANCIAL SYSTEM THREE INTERRELATED COMPONENTS: • Financial Intermediaries • Financial Markets • Financial Assets/ Instruments (Securities)

Financial Intermediaries • Represent a significant change in the whole process of transfer of choice of investment from an individual saver to an institutional agents. • Convert primary securities with a given set of characteristics, into indirect securities with very different features. • The ability of FIs to transform a primary securities into an indirect security makes it more attractive to both the borrowers and the lenders thereby adding a number of indirect and derived benefits that add greatly to the effectiveness and efficiency of the saving investment process.

Benefits of the Process Benefits with the tailoring of Financial assets according to the desires of savers and investors are • Convenience in terms of denomination & liquidity • Lower risk due to diversification • Expert management • Lower cost

Structure of Financial Institutions A diversified structure of FIs in a matured and sophisticated system consists of : • Banks • NBFCs • Mutual Funds • Insurance organizations and so on.. These are able to mobilize saving from the widest section of the investing public and channelize them to a cross-section of the economic/ industrial enterprises.

FINANCIAL MARKETS A significant component- not a source of funds, but they act as a facilitating organization and link the savers & investors, both individuals as well as institutional. Provide a wide variety of specialist institutional facilities classified as • Money Markets • Capital Markets

Money Market • Market dealing in monitory/ financial assets of a short term nature, generally less than one year Broad Objectives: • A equilibrating mechanism for evening out short surpluses and deficiencies in the financial system. • A focal point of central bank (RBI) intervention for influencing liquidity in the economy through a variety of instruments. • A reasonable access to the users of short-term funds to meet their requirements at realistic/ reasonable price/ cost. The money market organization comprises of a no of interrelated sub-markets such as • Call markets • T-Bills Market • Commercial Bills Markets • CP Market • CD Market • REPO Market and so on

Capital Market Market for long term funds having two segments: • Primary/ new issue Deals in new securities offered to the investors for the first time through triple-service functions at different stages of issue namely Origination, Underwriting and Distribution • Secondary Stock Exchange Market Stock exchange is the market for existing securities and discharges three vital functions like acting as nexus between saving and investments, providing liquidity to investors through its platforms and helps in continuous price formation.

Financial Assets Claim on stream of income and/ or assets of another economic unit and is held as a store of value and for the expected return Types of financial assets: • Primary/ Direct Security issued by a non financial economic unit such as ordinary/ preference shares, debentures/ bonds and innovative debt instruments including participating, convertibles, warrants and so on.. • Indirect Security Securities such as units of mutual funds securities receipts of securitization /asset reconstruction companies and securitized debt instruments of SPVs. The pooling of funds by an FI and converting a primary security in to an indirect security is associated with the no of benefits like convenience, diversification, expert management and lower cost.

Derivatives Includes • A security derived from a debt instrument, share, secured or unsecured loan, risk instruments, contract for differences or any other form of security. • A contract which drives its value from the prices/ index of prices of underlying securities. It is an instrument of risk management.

Common Derivatives • Forward contract An agreement to exchange an asset for cash, at a predetermined future date specified today. At the end of the contract, one can entre into an offsetting transaction by paying in the difference in the price. It is settled by the delivery of the asset on the expiration date. • Future contract: Contracts are transferable specified delivery forward contracts. They are the agreements between two counter parties to fix forward the term of an exchange/ lock in the price today, of an exchange that will take place between them at some fixed future date, ranging between 3 to 21 months. Depending upon the underlying asset, future contracts could be stock futures or index futures.

Options Give the holder the right (but not the obligation ) to buy (call option) or sell (put option) securities at a pre determine price (strike/exercise price) within/ at the end of specified period. In order to acquire the right of option, the buyer pays to the seller, an option premium as the price for the right. He can lose no more than the option premium paid but his possible gain is unlimited. The sellers' possible loss is unlimited but his maximum gain is restricted to the option premium charged by him.