Download

1 / 20

200 likes | 210 Views

Join us for the CFA Victoria Society's Annual Forecast Dinner featuring presenter Paul Balfour. Discover Paul's expert predictions for oil, gold, CAD/USD, and the Canadian 10-year bond yield. Gain valuable insights to inform your investment decisions.

E N D

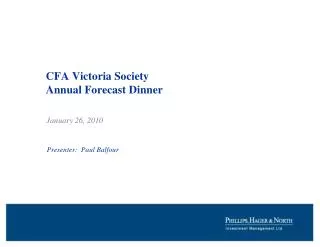

CFA Victoria SocietyAnnual Forecast Dinner Presenter: Paul Balfour January 26, 2010

Tonight’s Guesses, er … Forecasts 1. Oil 2. Gold 3. $CAD / $USD 4. Canadian 10 year bond yield • S&P/TSX Composite • S&P 500

Crude Oil – WTI Spot 120.00 100.00 80.00 60.00 40.00 20.00 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Average daily oil demand worldwide has risen from 76 million barrels in 1999 to about 85 million today. Average daily traded volumes of just NYMEX light sweet crude futures were 609 million barrels per day in 2009 up from 150 million ten years earlier Source: IEA, NYMEX/CME 700,000 600,000 500,000 400,000 Thousands of Barrels per Day 300,000 Nymex Average Daily Volume World Oil Demand 200,000 100,000 0 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Speculation is not an Issue??

Gold (London PM Fix) 1000 800 600 400 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Gold – A Metallurgist’s View! Lead Gold Aluminum Copper Atomic Weight 207.20 196.97 26.98 63.50 Density 11.3 19.3 2.7 8.9 Hardness 1.5 2.5 2.8 3.0 Melting Point 327°C 1064°C 660°C 2562°C Electrical Resistance 208 22.1 28.2 16.8 Price per pound 99¢ $17,600 $1.00 $3.35

U.S. Trade Weight Dollar (DXY) 140.00 120.00 100.00 80.00 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

PPP Valuation USD vs Purchasing Power Parity % Over/Undervaluation, Oct. 2009 160 USD -16.1 PPP 150 -2.7 SEK Average DXY 140 20% bands JPY 6.0 130 7.8 GBP 120 CAD 16.4 DXY Index Level 19.7 NOK 110 CHF 20.7 100 22.9 EUR 90 AUD 26.5 80 27.8 NZD 70 -20 -15 -10 -5 0 5 10 15 20 25 30 1975 1980 1985 1990 1995 2000 2005 2010 Source: Deutsche Bank, Bloomberg Source: Deutsche Bank US Dollar - Getting Undervalued? Source: F:\Group\Econ\Special Charts\DXY (PPP).xls\ DXY bar USD PPP Updated: Jan 4, 2010

1.10 325 USD per CAD (left) 1.05 BoC Commodity Price Index (right) 1.00 275 0.95 Correlation = 0.92 0.90 225 0.85 Index US$ per C$ 0.80 175 0.75 0.70 125 0.65 0.60 75 1995 1997 1999 2001 2003 2005 2007 2009 Canadian Dollar & Commodity Prices Source: Bank of Canada

Canada 10-Year Bond Yield 10.00 8.00 6.00 4.00 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

4.5 4.0 3.5 3.0 2.5 Yield (%) 2.0 December 31, 2007 1.5 December 31, 2009 1.0 0.5 0.0 1 Year 2 Years 3 Years 5 Years 7 Years 3 Mths 10 Years 20 Years 30 Years Canadian Yield CurveHistorically Steep Levels Driven By Low Short Yields Canadian Yield Curves Source: yc…\can & US yield curves Source: yc/can 3mth… 12/31/09

S&P/TSX Composite Index 14000 12000 10000 8000 6000 4000 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

S&P 500 Returns by Credit Rating - 2009 250% 216% 200% 100% 90.8% 150% 80% 105% 100% 56.2% 60% 55% 43% 35.1% 40% 50% 36% 33% 27.9% 12% 9% 20% 0% B+ to B- A+ to A- 0% AAA+ to BBB+ to BBB- AAA- Not Rated (ALL) BB+ to bb- AA+ to AA- CCC+ to C- TSX 60 S&P/TSX TSX Small TSX Composite Cap Venture # of Companies 5 22 131 187 68 9 3 75 Canadian Equity Market 2009Low Quality Outperformed One Year TSX Performance Breakdown (TR) * Credit ratings as of July 7 2009 Source: RBCAM, Bloomberg

Canadian Equity – OutlookTSX Bottom Up Earnings Expectations - 2011 30% TSX Bottom Up Earnings Expectations 25% 25% 22% 20% 18% 2011 17% 15% 14% 15% 13% 11% 10% 7% 6% 4% 5% 0% Health Utilities Energy Telecom Financial Materials Consumer Staples Industrials S&P/TSX Composite Technology Consumer Discretionary Conservative Earnings Recovery Expectations?Cumulative TSX Earnings Recoveries Troughs – First 3 Years 350% 304% 300% 242% 250% 217% 200% 154% 150% 100% 50% 0% 1992-1995 1983-1986 2002-2005 2010-2013E Source: TD Securities – TSX Bottom Up Earnings

Canadian Equities – Lots of Cash Around Canadian Cash (Savings and Money Market Funds) as a % of TSX Market Cap 60 57.0% 55 50 45.8% 45.5% 45 40 35 30 25 20 Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Source: RBC Capital Markets, Bank of Canada, Haver Analytics

S&P 500 Composite Index 1400 1200 1000 800 600 400 200 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

50% 43.9% 45% 40.5% 40% 37.2% 35% 30% 27.2% 26.5% 24.2% 25% 19.7% 20% 15% 10% 5% 0% S&P 500 NASDAQ Russell Top Russell Russell 2000 Russell 1000 Russell 1000 Comp. 200 (Lg-cap) Mid-Cap (Sm-cap) Value Growth Major U.S. Market Indices2009 Returns Three key performance themes played out in 2009. Mid and small-caps outperformed large-caps Growth strongly outperformed Value (third year in a row) Technology beat everything Source: Morgan Stanley

A Big Thanks to my Personal Research Team! “The views presented by Paul tonight do not necessarily reflect those of RBC, RBC Global Investment Management, Phillips Hager & North Investment Management etc., etc … In fact, the opposite is probably the case.” - J. Montalbano

THE END CHEERS!