Download

1 / 15

150 likes | 156 Views

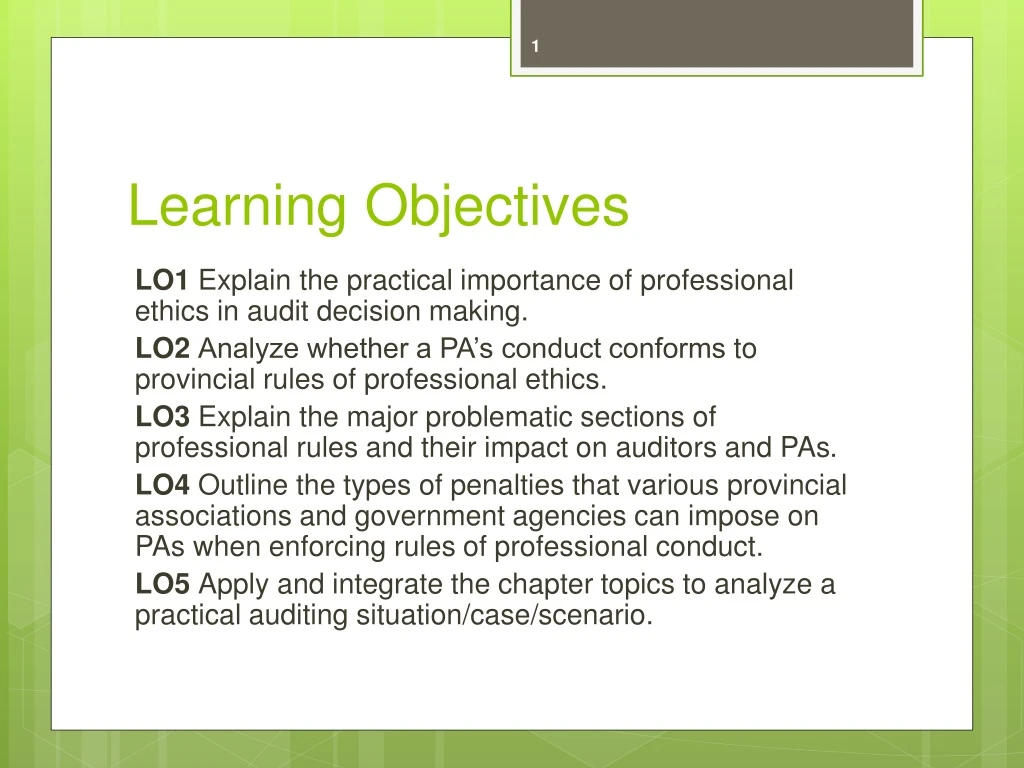

Learning Objectives. LO1 Explain the practical importance of professional ethics in audit decision making. LO2 Analyze whether a PA’s conduct conforms to provincial rules of professional ethics.

E N D

Learning Objectives LO1 Explain the practical importance of professional ethics in audit decision making. LO2 Analyze whether a PA’s conduct conforms to provincial rules of professional ethics. LO3 Explain the major problematic sections of professional rules and their impact on auditors and PAs. LO4 Outline the types of penalties that various provincial associations and government agencies can impose on PAs when enforcing rules of professional conduct. LO5 Apply and integrate the chapter topics to analyze a practical auditing situation/case/scenario.

Permitted Loans The accountant will not be deemed to be in conflict of interest for: • home mortgages, • immaterial loans, or • secured loans made by financial institutions to the accountant under normal lending procedures, terms and requirements. Otherwise, independence would be impaired by virtue of the financial relationship between the auditor and the lender. LO2

Permitted Loans Independence also is not impaired by a member obtaining: • auto loans or leases collateralized by the automobile, • insurance policy loans based on surrender values, • loans collateralized by cash deposits, or • credit card balances, if the loans are made in the normal course of business for the issuer. LO2

Other Issues Related to the Independence Principle Honorary Positions in Non-Profit Organizations: • PAs’ independence is not impaired if the member is an honorary director where criteria are met. Retired Partners: • Retired partners may impair independence after they have left the firm, except where conditions relating to their retirement are satisfied. Accounting Services: • Where PA has appearance of having prepared the statements, independence may be impaired. LO2

Other Issues Related to the Independence Principle Rotation of Partners and Second Partner Review: • Rotation of the lead audit partner and/or the concurring partner is required every five years. • A second partner review is mandated by both SOX and the CPAB. Actual or Threatened Litigation: • PAs are considered not independent when company management threatens or starts a suit against the PA, or when the PA threatens or starts a suit against the company. LO2

Other Issues Related to the Independence Principle Investor or Investee Relationships: • Material investments by the PA and by the client need to be considered. Effect of Family Relationships: • Financial interests of spouses and dependent persons, and some interests of close relatives are attributed to the member. Analysis: • Objectivity and integrity are always required, but the rules concentrate on “conflicts of interest” based on financial measures. LO2

Professional Competence and Due Care Professional competence and due care principles are required under the rules of conduct, as well as under GAAS. • The professional competence and due care principles are a comprehensive statement of general standards that accountants are expected to observe in all areas of practice. These are principles that enforce the various series of professional standards. LO2

Compliance with Professional Standards PAs shall perform professional services in accordance with generally accepted standards of practice for the profession. • Extension and refinement of the due care principle. • Practical effect of the rule is to make noncompliance with all technical standards subject to disciplinary proceedings. • The failure to follow auditing standards, accounting and review standards, and assurance, compilation and professional conduct standards is a violation of this rule. LO2

Confidentiality A member in public practice shall not disclose any confidential information without the specific consent of the client. • This rule does not: • relieve the PA from complying with a valid summons, or • prohibit a member from • complying with applicable laws, • a review of his/her professional practice, or • participating in disciplinary hearings. LO2

Confidentiality Confidentiality is intended to facilitate a free flow of information. • PA will require access to sensitive information to discharge responsibilities. • Creates difficulties over auditors’ obligations to blow the whistle on illegal practices. • In general, PAs are not obligated to do so. • May be required if the client has intentionally associated PA with misleading statements, conduct, or reports. • Seek legal counsel. LO2

Fees Contingency Fees: • PAs shall not offer professional service for a fee contingent on the results of such service. • PAs should not represent that no fee will be charged except in the case of services of a charitable nature. Fee Quotation: • Fees are quoted only when requested by a client or prospective client, and then only when adequate information is obtained. LO2

Discreditable Acts Public accountants will not bring discredit to the profession. • Discreditable acts might include the following: • fraud, false tax returns, • conviction on a criminal offence, • withholding client’s books and records, • employment discrimination, • failure to follow government guidelines in government audits, and • false entries in clients records Rules include expulsion of members. LO2

Advertising and Other Forms of Solicitation A PA shall not seek clients by advertising in a manner that is false, misleading, or deceptive. • Advertising must not include: • unjustified expectations of favourable results, • implied ability to influence officials or agencies or courts, • incorrect fee estimates, or • misleading representations Some liberalization of rules has taken place because of the Canadian Charter of Rights and Freedoms. LO2

Commissions and Referral Fees Prohibited Commissions: • PAs may not receive any referral commissions where the engagement involves assurance services. • PAs may receive commissions on the sale or purchase of an accounting practice. LO2

Form of Organization and Name Form of Organization • The practice shall be under the personal charge of a member who is a public accountant. Name of Organization • Firm names may not be misleading. The name of the firm usually consists of the names of the partners. • Names of past owners may be included in successor firms. LO2