Download

1 / 3

30 likes | 163 Views

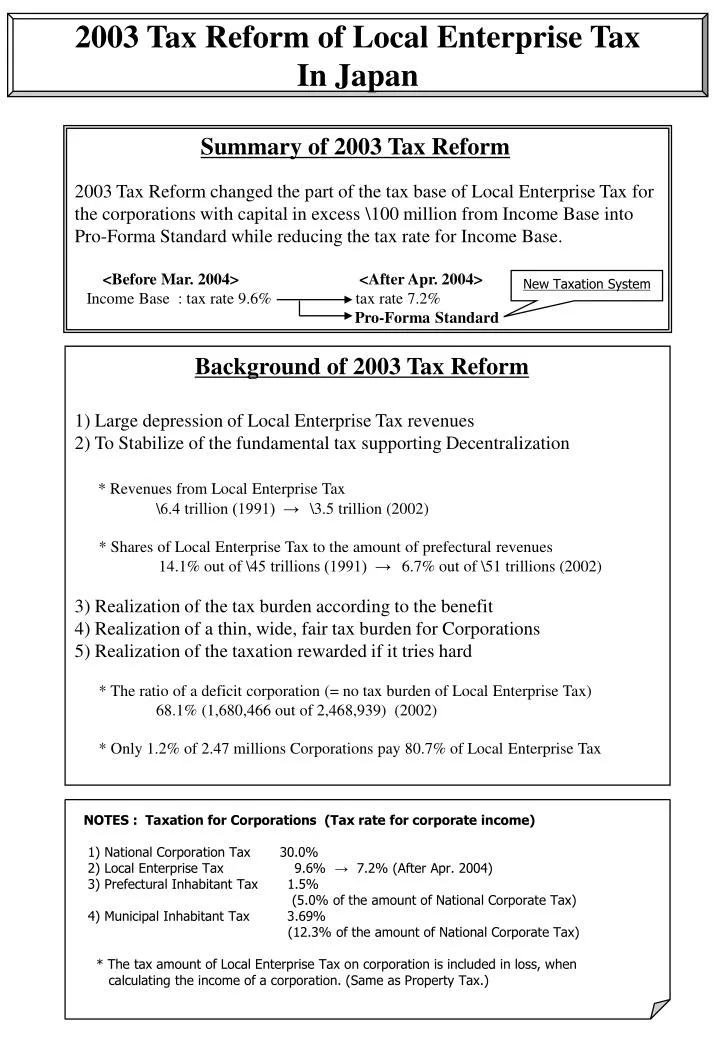

2003 Tax Reform of Local Enterprise Tax In Japan. Summary of 2003 Tax Reform 2003 Tax Reform changed the part of the tax base of Local Enterprise Tax for the corporations with capital in excess 100 million from Income Base into Pro-Forma Standard while reducing the tax rate for Income Base.

E N D

2003 Tax Reform of Local Enterprise Tax In Japan Summary of 2003 Tax Reform 2003 Tax Reform changed the part of the tax base of Local Enterprise Tax for the corporations with capital in excess \100 million from Income Base into Pro-Forma Standard while reducing the tax rate for Income Base. <Before Mar. 2004><After Apr. 2004> Income Base : tax rate 9.6% tax rate 7.2% Pro-Forma Standard New Taxation System Background of 2003 Tax Reform 1) Large depression of Local Enterprise Tax revenues 2) To Stabilize of the fundamental tax supporting Decentralization * Revenues from Local Enterprise Tax \6.4 trillion (1991) →\3.5 trillion (2002) * Shares of Local Enterprise Tax to the amount of prefectural revenues 14.1% out of \45 trillions (1991) →6.7% out of \51 trillions (2002) 3) Realization of the tax burden according to the benefit 4) Realization of a thin, wide, fair tax burden for Corporations 5) Realization of the taxation rewarded if it tries hard * The ratio of a deficit corporation (= no tax burden of Local Enterprise Tax) 68.1% (1,680,466 out of 2,468,939) (2002) * Only 1.2% of 2.47 millions Corporations pay 80.7% of Local Enterprise Tax NOTES : Taxation for Corporations (Tax rate for corporate income) 1) National Corporation Tax 30.0% 2) Local Enterprise Tax 9.6% →7.2% (After Apr. 2004) 3) Prefectural Inhabitant Tax 1.5% (5.0% of the amount of National Corporate Tax) 4) Municipal Inhabitant Tax 3.69% (12.3% of the amount of National Corporate Tax) * The tax amount of Local Enterprise Tax on corporation is included in loss, when calculating the income of a corporation. (Same as Property Tax.)

Pro-Forma Standard Taxation on Local Enterprise Tax Before Mar. 2004 After Apr. 2004 Value-Added Levy (0.48%) 2 Income Levy Income Levy (Tax Rate: 9.6%) (Tax Rate: 7.2%) Capital Levy (0.2%) 1 Income : Pro-Forma 3 : 1 Effective Tax Rate for Cooperate Income (including national and local tax) 40.87%* 39.54%** * (30+1.5+3.69+9.6)/(100+9.6)=0.4087 * *(30+1.5+3.69+7.2)/(100+7.2)=0.3954

425 billion 300 billion 100 billion Calculation of Tax Base for Pro-Forma Standard Taxation Addition-type Value-Added Levy(Tax Rate:0.48%) Distribution of Earning Profit and Loss Tax Base for Value-Added Levy = ± Payrolls + Net Interest Paid + Net Rent Paid Wages, bonuses, fees, Interest paid minus Rent paid minus Single-year Profit and Loss for taxable year retirement payment interest received rent received Single-year loss can deducts from the amount of the distribution of earning. Distribution of Earning = 130 Deduction for employment stabilization The amount of payrolls exceeding 70% of the total amount of the distribution of earning can deduct from the tax base Profit 10 Net Rent 5 Net Interest 5 * Deduction 29 120 - (130 × 0.7) = *29 Payrolls 120 Tax Base for Value-Added Levy = 111 = Distribution (130)-Deduction (*29)+Profit(10) Capital Levy(Tax Rate:0.2%) Tax Base for Capital Levy Paid-in capital or Amounts invested + = Capital surplus Amount of capital Gross asset *1 Deduction for Holding Companies The amount of capital of certain holding companies can be reduced by the portion of the amount of stocks of subsidiaries to the total amount of gross assets of the holding company. Stocks of Deduction subsidiaries Tax base Other assets Capital *2 Deduction for Huge Capital Companies In calculating the tax base, capital in excess \100 billion can be reduced. No part of capital in excess \1,000 billion can be included. 1 ,000 billion Tax base x 25% 500 billion x 50% 100 billion 100%