Download

1 / 7

70 likes | 151 Views

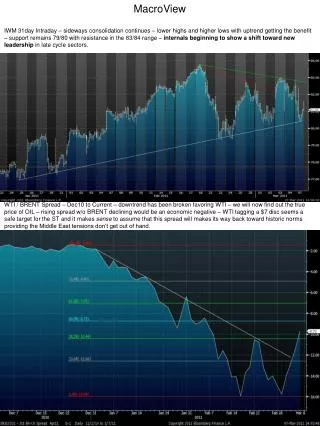

MACROVIEW. XLE – ABSOLUTE VIEW - 06/Current – 40wk MA –up 49.5% since 4q10 - slightly extended and most likely due for a breather – keep an eye on BRENT/WTI spread – further blowout could hit entire energy patch.

E N D

XLE – ABSOLUTE VIEW - 06/Current – 40wk MA –up 49.5% since 4q10 - slightly extended and most likely due for a breather – keep an eye on BRENT/WTI spread – further blowout could hit entire energy patch XLE vs SPX – RELATIVE - 06/Current – 40wk MA – 18% outperformance since 4q10 – trend remains up but most like will see some backing and filling – rotations within CRB theme highly likely

MOO vs SPY – 06/Current – 40wk MA – like the OIL vs SPX view yesterday but regarding AG stocks – Central Banks seem to be of the opinion that rising asset prices shield the people from inflation. But, what happens if the price of NEEDs are rising faster than the prices of those assets? What will the impact be on interest rates? Consumption trends? We’re nearing an answer to these questions. MOO vs XLE – 06/Current – 40wk MA – the world NEEDs food and WANTs oil – recent break ABOVE 30m consolidation begs the question….Is this a SECULAR shift?

GOLD vs AG – YOY – 28% drop in relative performance since Q210 (deflation scare created by EUR 1.19) and we will most likely see a rotation back into GOLD. Should AG prices decline causing economic mkts to reheat we could see a real battle for CBs to keep the inflation fears from spreading. The idea of rising needs actually being a “deflator” of consumption is going to be tested. GOLD vs AG – 1991 to Current – 36M MA

Greece – 2yr – 6.7% YLD Ireland – 10yr – 9.1% YLD

Spain – 5yr – 4.06% YLD Portugal – 4yr - 6.65% YLD

GOLD Priced in CHF – 2003 to Current – If the PIIGS bond levels begin to hit our recent lows we could see a rotation back into GOLD as mkts shift back toward expansionary FX views. Combining FX AND the comment made regarding falling AG prices on consumption, one can possibly begin to see why this “time could indeed be different”. IF any further financial missteps will be met with easy monetary policy it makes sense to fear FX deflation over deflationary growth. Should CBs take the easy money route we could see every more hoarding putting upward pressure on NEEDs and downward pressure on SOV debt. Too early to tell but something to think about. GOLD Priced in EUR – 2003 to Current – watch EURCHF for possible signs of strees coming from EU