Download

1 / 16

160 likes | 376 Views

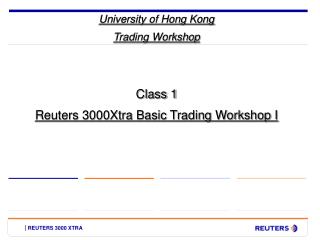

University of Hong Kong Trading Workshop. Class 4 Treasury Workshop II FX Option Markets. David Lo. Buy a House. Buy USD agst CHF. Guarantee. Quantity. Guarantee. Nominal . 1 month. 1 House. 1 month. Amount. USD 1 mio. $ 1,200,000. 1.4800. What is OPTION?. Options.

E N D

University of Hong Kong Trading Workshop Class 4 Treasury Workshop II FX Option Markets David Lo

Buy a House Buy USD agst CHF Guarantee Quantity Guarantee Nominal 1 month 1 House 1 month Amount USD 1 mio $ 1,200,000 1.4800 What is OPTION?

Options • The right, but not the obligation, • to buy or sell a predetermined amount of underlying asset • against a fixed price • until a fixed, future date

“Right to BUY” “Right to SELL” CALLOption PUTOption Call & Put Options - Vanilla options USD Put / JPY Call Right to sell USD USD Call / JPY Put Right to buy USD

Currency (FX) Option • A currency option is a contract where the option buyer pays a premium to the option writer to obtain the right, but not the obligation, to buy (call) or sell (put) a specified amount of foreign currency (or a currency futures contract) at an agreed exchange rate, on or before a specified future date. • How to price the FX Option? • >Implied volatility is the volatility which, if input into the relevant option pricing model, will give an option price equal to the current market premium, i.e., the level of volatility that buyers and sellers seem to have accounted for in the current market price. Option greeks measure the sensitivity of the price of an option to changes in key variables. Delta, gamma, theta, vega and rho are all examples of option greeks.

Exotic Options • Single barrier options - single barrier option types: • knock-in • knock-up-and-in • knock-down-and-out • knock-out • knock-up-and-out • knock-down-and-out • window-knock-in • window-knock-up and in with an early end date or a forward start date • window-knock-down and in with an early end date or a forward start date • window-knock-out • window-knock-up-and-out • window-knock-down-and-out • knock-out-with-rebate

Exotic Options • Double barriers & binary options • Average or asian options • Lookback options • Compound options • Premium Deposit / Structuring Notes

Currency Options Models • The Currency Options worksheet allows real time pricing of vanilla currency options. A separate worksheet exists for FX Exotic options. The calculations available on this worksheet include swap points for cross currency deals together with deposit rates for the two currencies. The worksheet allows the simultaneous pricing and analysis of up to nine separate options. Both real time and user amended pricing is available. • The Currency Options model prices vanilla FX options. • Features • Using this model you can: • Obtain real time pricing of Vanilla options. • Use the Black and Scholes calculation model. • Benefits • Fully flexible vanilla option pricing. • Portfolio available for 9 different strikes.

FX Exotic Options • FX Exotic Options enables you to calculate foreign exchange currency options. You enter the standard terms of the option, and the model retrieves realtime pricing information, including strike. The model calculates the premium, implied volatility and sensitivities. • Features • The model calculates the following data for each option type: • premium in four way: • in FX points, in base or quote currency • percentage of the spot rate , percentage of the strike • implied volatility for the premium • calculates the sensitivities of the option for both the bid and ask side: • Delta ,Gamma, Rho, Theta, Vega • compare implied volatility from a known premium against the market quoted realtime volatility • hedge your option using sensitivities

Q & A DAVID_HKU@YAHOO.COM