Download

1 / 25

250 likes | 295 Views

Bretton Woods (and its demise). The war’s consequences. Anti-globalization developments: Soviet-imposed communism in Eastern Europe and Cold War Decolonization and dissolution of empires And spread of independent nations, with nationalist policies Ideological changes

E N D

The war’s consequences • Anti-globalization developments: • Soviet-imposed communism in Eastern Europe and Cold War • Decolonization and dissolution of empires • And spread of independent nations, with nationalist policies • Ideological changes • Markets vs planning, free trade vs protection • ECLA, Prebisch-Singer thesis • The reinforcement of import substitution in Latin America and many other developing nations • In Europe, widespread exchange controls and QRs • Pro-openness developments • U.S. Marshall Plan for Western Europe (1947)

The Bretton Woods “consensus” • Policy priority: domestic economic growth and full employment • International economic policy must conform to domestic objectives, not the other way around • Activist monetary and fiscal policies necessary to stabilize macroeconomy • Keynes: economy not self-stabilizing • Capital flows destabilizing • Experience of the 1920s • Fixed exchange rates desirable • Importance to international trade • Need to avoid competitive devaluations as in 1930s • The need to revive global multilateral trade • U.S.: break up Britain’s imperial preferences, and use growing trade to break Franco-German enmities (esp. thru European integration) • Importance of international cooperation • Lessons from the failure of cooperation in 1930s

The political underpinnings of the new consensus • Domestic: the priority of domestic social objectives over international economic integration • Full employment, economic growth, and the welfare state • Driven by • Mass franchise • Unions • Rise of labor-based or social democratic parties • Demands for social protection • The dominance of the U.S. in world economy and its willingness to subsume narrow economic objectives to broader political/strategic goals • The latter driven by the dominance of Northeastern elites in shaping U.S. foreign economic policies • Without which unlikely that multilateralism would have emerged as a cornerstone principle • The impetus for economic cooperation • Early on: US willingness to assist Europe • Later on: Despite frequent complaints, French and German economic cooperation with U.S. in return for the defense umbrella

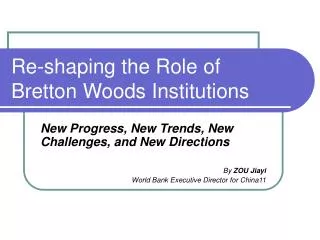

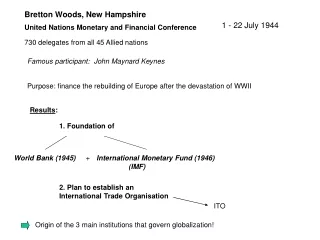

The Bretton Woods conference (1944) In line with the shifting roles of the U.S. and Britain, Keynes argued for larger amounts of BOP financing for the IMF and greater exchange rate flexibility (along with use of exchange and payments controls), while Harry Dexter White wanted pegged currencies and free capital flows. Harry Dexter White and John Maynard Keynes

John Maynard Keynes on the nature of the Bretton Woods regime “To suppose that there exists some smoothly functioning automatic mechanism of adjustment which preserves equilibrium if we only trust the methods of laissez-faire is a doctrinaire delusion which disregards the lessons of historical experience without having behind it the support of theory.” “Not merely as a feature of the transition, but as a permanent arrangement, the [BW] plan accords to every member government the explicit right to control all capital movements. What used to be heresy is now endorsed as orthodox.”

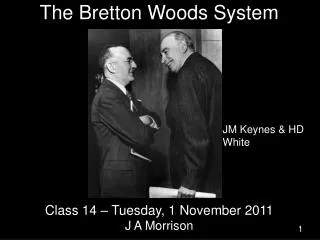

The international macroeconomic policy trilemma Capital mobility Gold Standard Free floating Independent monetary policy Fixed exchange rates Bretton Woods Pick two, any two

What are the advantages and disadvantages of each combination? • What do you give up when you give up • Independent monetary policy (GS, Argentina in 1990s) • Fixed exchange rates (1920s, recently) • Capital mobility

Interactions between domestic monetary policy and capital flows The asset market arbitrage equation In the absence of impediments to capital flows: Domestic interest rate = Foreign interest rate + expected rate of depreciation of home currency + risk premium for domestic assets Therefore capital mobility + pegged exchange rates tie the hand of domestic monetary policy.

How capital mobility and fixed ERs narrows space for domestic policy • Shifts in market perceptions of risk can cause havoc with domestic interest rates • “destabilizing capital flows” • Expectations of a devaluation would raise domestic interest rates, or alternatively, cause massive capital outflows • Again, destabilizing capital flows • The problem of self-fulfilling currency crises • Expansionary monetary policy that is inconsistent with the arbitrage equation would lead to massive capital outflows • Inability to respond to domestic business cycles • Alternatively, countries that want tighter monetary policy would face a massive capital inflows, defeating monetary policy

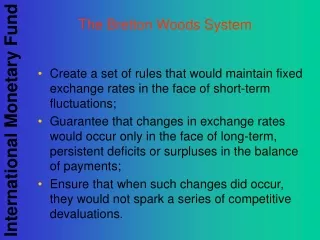

Rules of the game under the IMF • Based on fixed, but adjustable (in case of “fundamental disequilibrium”) exchange rates • But few parity changes in practice in major countries • Exchange controls substituted for devaluations (until 1959) • IMF to monitor national economic policies and make short-term BOP financing available • But no ability to force adjustment on surplus countries • Convertibility of national currencies for current account (after 1959), but not capital account transactions • Capital controls functioned as planned during 1940s and 1950s, but capital controls were part of an extensive set of financial controls at the time, such as interest-rate caps, directed credit, and lending restrictions • Effectiveness diminished subsequently as other controls were relaxed • Note how each of these rules are designed with an eye towards enlarging domestic policy space (relative to what came before)

GATT (I) • Originally part of a larger agreement, ITO • Which included arrangements on commodities, investment, and RBPs • The principle of non-discrimination and MFN • Exception for CUs and FTAs • Focus on tariff reduction • Quotas outlawed • Except for agriculture • BOP exception • MFA, later

GATT (II) • Special regime for “developing countries” • Exempt from reciprocity in tariff negotiations, and allowed use of QRs • Several “safety valves” • BOP exception • Anti-dumping • Export subsidies and CVDs • Safeguards clause • A weak dispute settlement procedure • Note once again the extent of policy space

GATT (III) • Licensing and other QRs rampant during 1950s, under pressure of BOP deficits • Series of multilateral trade rounds, esp. since 1960s (Geneva, Annecy, Torquay, Kennedy, Tokyo, Uruguay, Doha) • A mercantilist logic in trade negotiations? • Liberalize only if your trade partners do the same • Possible economics justification: neutralizing adverse terms-of-trade effects of own liberalization • Liberalization largely limited to manufactured goods (except textiles and clothing) and to developed countries • Agriculture and services not included • Labor services, in particular, highly restricted • Until Uruguay Round (1994), which created WTO

Early road bumps • U.S. as the “structural creditor” nation until late 1950s • European currencies overvalued (“dollar shortage”), necessitating trade and payments restrictions • Sterling crisis of 1947, resulting in the move to convertibility (result of U.S. pressure) to be reversed in six weeks • Devaluation of pound in 1949, followed by others in Europe • Subsequent U.S. willingness to condone discrimination against itself • European Payments Union: speedier liberalization among European countries than against U.S. • Continued use of payments restrictions in the 1950s to deal with BOP problems

Problems of the dollar-exchange standard in 1960s • Growing trade required growing credit and reserve assets to finance it • IMF resources were not adequate • Despite eventual creation of Special Drawing Rights (SDRs) • Dollars became the reserve currency of choice (playing the role that gold played in GS) • But growth of dollar reserve assets held by other countries required U.S. to be running BOP deficits • Which was dynamically unstable since it let countries to question the dollar’s parity vis-à-vis gold (the Triffin dilemma) • De Gaulle: The “exorbitant privilege” of the US—the ability to finance its deficits by printing its own currency (which was in turn willingly held by other countries) • French threats to liquidate her dollar reserves • Parallels with today (and China’s role…)

Collapse of the fixed ER regime • Overvalued dollar • Market prices of gold, and direction of flows (out of dollars) • On August 13, 1971 Nixon suspends convertibility of dollars to gold and imposes a 10% surcharge on imports • Followed by revaluations of DM, Yen, and a few others and widening the band for currency fluctuations (from 1 to 2.25%) • Further currency pressures cause European countries to float their currencies in 1973 • US and Japan continue to float • Attempts to achieve currency stability within Europe: the Snake and the EMS

The ups and downs of the Dollar Volcker’s tight money policies Plaza accord Up = appreciation Down = depreciation Source: blogs.ft.com/maverecon/files/2009/01/chart3.gif

The trade and monetary regimes in 1970s and 1980s: derogation or system maintenance? • “Derogations from liberalism” in trade practices • Multi-Fibre Arrangement (1974 ->) • Voluntary export restraints in 1980s • Spread of AD • A liberal economic order with lots of cheating, or a compromise regime in which departures from liberal principles are necessary to maintain the regime? • A similar question can be posed of the gradual move towards floating in the early 1970s • Is this a case of what Ruggie calls “norm-guided change,” i.e., the ultimate ends and values remain the same, but the policy practices change • The regime is largely intact, if one views it from these lenses

The compromise of “embedded liberalism” (Ruggie) • The Bretton Woods as a distinct regime • Neither fully liberal • Nor mercantilist • Based on a different conception of social purpose and state action • A different balance between markets and society • Priority accorded to domestic policy objectives over international ones • But reflecting a compromise between the needs of domestic stability and the need to revive the multilateral trade and payments system. • “Unlike the economic nationalism of the thirties, [the regime] would be multilateral in character; unlike the liberalism of the gold standard and free trade, its multilateralism would be predicated upon domestic interventionism.” • Multilateralism goes furthest where domestic costs (adjustment and distributive”) are smallest • E.g., intra-industry trade in manufactures

“Power versus purpose” in driving trends in globalization • Is it power? • But power can be used to construct both liberal and mercantilist international economic orders • Dutch mercantilism versus British 19th century liberalism • It can be used to promote international trade and investment or to limit them • Britain and U.S. versus Nazi Germany or USSR • Or ideas? • Ideas about the appropriate relationship between states and markets • Mercantilism versus liberalism versus embedded liberalism • In the presence of strong enough convergence on ideas, can the world economy dispense with a powerful hegemon? • If everyone believes in free trade and free capital mobility, can international cooperation supply the needed institutional underpinnings?

Historical experience with growth 9 GDP per capita growth rate of fastest growing country/region (annual average, %) World GDP per capita growth rate (annual 8 average, %) 7 6 5 4 3 2 1 0 1000-1500 1500-1820 1820-1870 1870-1913 1913-1950 1950-73 1973-90 1990-2005 Western Europe United States Other Western Mexico Norway Japan South Korea China offshoots Economic performance under BW in historical perspective

Why did the BW regime wither away? • Growth of capital flows • Euro-currency markets (dollar deposits held in non-U.S. banks) to evade interest-rate caps in the U.S. • Difficulties of controlling capital flows • Current account convertibility makes it harder for capital controls to work • Over- and under-invoicing trade flows • The relative weakening of U.S. position • U.S. deficits render USD-gold parity less credible • Market price of gold rises above official parity $35/oz in 1960s • Ideas and ideology • The Thatcher-Reagan revolution of the 1980s • The discrediting of inward-oriented development policies, especially after the Latin American debt crisis of 1982 • Even though record is not all that clear (as we’ll see later) • A victim of its own success? • The rapid growth in international trade and investment that it stimulated led to demands for further liberalization

The collapse of the consensus of embedded liberalism • Two key processes that mark the change • Financial globalization • The deep integration agenda within WTO

The World Trade Organization (1995) • A deep integration agenda • Versus the shallow integration model of the GATT • Covers services, investment, agriculture, and intellectual property in addition to manufactures • Discipline over behind-the-border policies: subsidies, TRIMs, TRIPs • A new dispute settlement procedure • Panel and appellate bodies • Veto possible only by consensus • If policy is found to violate rules, must remove it or face retaliation • What is and is not a “trade” issue becomes less clear • U.S.-EU beef hormone case (health and food safety) • Shrimp-turtle case (environmental policies)