Download

1 / 32

330 likes | 530 Views

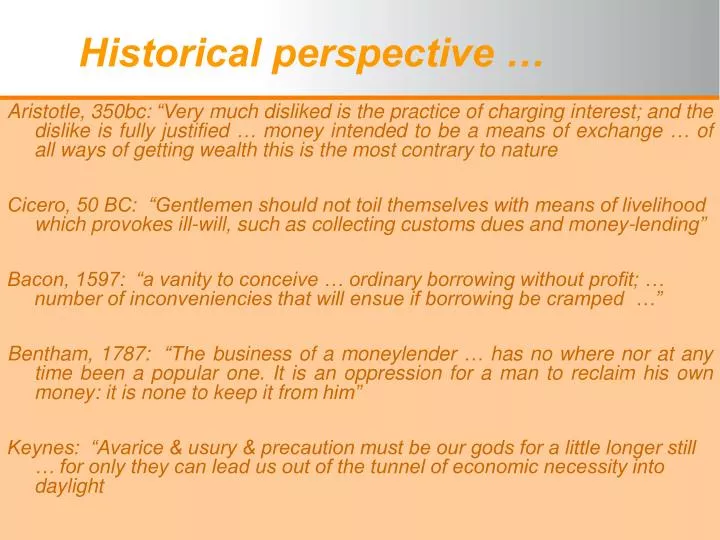

Historical perspective …. Aristotle, 350bc: “Very much disliked is the practice of charging interest; and the dislike is fully justified … money intended to be a means of exchange … of all ways of getting wealth this is the most contrary to nature

E N D

Historical perspective … Aristotle, 350bc: “Very much disliked is the practice of charging interest; and the dislike is fully justified … money intended to be a means of exchange … of all ways of getting wealth this is the most contrary to nature Cicero, 50 BC: “Gentlemen should not toil themselves with means of livelihood which provokes ill-will, such as collecting customs dues and money-lending” Bacon, 1597: “a vanity to conceive … ordinary borrowing without profit; … number of inconveniencies that will ensue if borrowing be cramped …” Bentham, 1787: “The business of a moneylender … has no where nor at any time been a popular one. It is an oppression for a man to reclaim his own money: it is none to keep it from him” Keynes: “Avarice & usury & precaution must be our gods for a little longer still … for only they can lead us out of the tunnel of economic necessity into daylight

National Credit Act • To promote a fair and non-discriminatory marketplace for access to consumer credit • To promote responsible credit granting and use and for that purpose to prohibit reckless credit granting; • To provide for debt re-organisation in cases of over-indebtedness Gabriel Davel November 2009

Until end 1980’s, limited access to finance for black South Africans. Mainly furniture finance and in government-supported housing finance. Latter geared to broadening ‘black middle class’, getting support for the capitalist system! Sunnyside Group initiated various exemptions: Group of academics & practitioners lobbied for exemptions to remove legal constraints. Usury Act Exemption for small transactions & change to Pension Funds Act, allowing benefits to be used as security for home loans. Also facility to deduct loan payments from salaries. Period of strong growth. Exemptions aimed at housing market. Massive growth in consumer lending. Predatory & abusive lending practices by both commercial lenders & NGOs who commercialized Dual structure from 1999: Micro Finance Regulatory Council established, maintaining exemption, but improving consumer protection. Larger transactions remain under Usury Act & Credit Agreements Act – dated & inappropriate legislation. Personal insolvency totally inappropriate. No regulation of credit bureaus. Limited access to banks, savings or loans, but continuing growth in ‘exempted loans’. Mini banking crisis in 2002 / 2003: Lending practices and governance failures both contributed. Highlighted need for reform. MFRC research highlighted problems. Initiated credit law reform project in 2002. Govt sponsored Task Team established. Drafting started in 2004. NCA adopted in 2005, effective 2007. Executive Summary - 1Historical perspective

Extensive empirical research, To define (a) market practices, (b) quantify reckless lending & indebtedness, (c) quantify cost of credit, (d) get consumer views, (e) get industry & expert views. To gather evidence on what is wrong in the market, quantify the cost of doing nothing; Research on international dispensations To evaluate options, ensure equivalence – assess rationale / theoretical basis for different approaches. Build case for reform. Extensive consultation with local & international experts. Public briefings & consultation in all provinces.Strong public support. Rationale for intervention clear. Opponents started backing down. Parliamentary process: Extensive briefings on research & on specific sections. Huge support from all parties, despite lobbying.Public hearings, direct engagement between technocrats & industry. Extensive scrutiny and amendments. Defense against counter-revolution: Arguments: ‘unintended consequences’, ‘cost of compliance’, ‘increased cost of credit’, ‘regulatory burden’, ‘decreased access’. Also personal attacks. We did detailed research on each of these topics. Approach: Speed, big bang, not piecemeal. Executive Summary - 2 Process: extensive research, consultation & awareness of problems

Research into credit supply MFRC investigations & research reports “Cost, Volume & Allocation of Consumer Credit”, Dr Hawkins, FEASibility Consumer views Focus group discussions by market research company Industry & Stakeholder Views Comments from range of stakeholders on their assessment of problems Comparison of SA & International Legislation Theoretical basis for reform & assess alternatives Regulation of Payday Lending in US, Partick Meagher, University of Maryland (IRIS) Interest Rate Regulation (Prof Dympski, University of California, Prof Schierenbeck, Basle University; Dr Falkena, SA Reserve Bank; Prof Llewellen, UK Legislation in SA, Rudolph Willemse, Hofmeyr, Herbstein, Ginwala Workshops with SARB, Treasury et al with local & international ‘experts’ to confirm statistics & discuss conclusions with international experts in London … policy & Bill The process: Through MFRC investigations & Credit Law research, increasing understanding of problems, Extensive consultation with all stakeholders. Evidence to support reform.

Not an attempt to maximise consumer protection.Rather: Deal with consumer credit market, as a market in which 1000’s of credit providers, debt collectors and others engage with millions of consumers to originate millions of transactions; The manner in which this market functions determines consumption patters, allocation of income and social welfare. Evaluate the legal system within which these transactions take place; To evaluate the “rules” which the legal system creates; to assess whether these rules create incentives for particular behaviour by credit providers & consumers Expand the regulators’ duties, or change the underlying legislation? Employ more cops, or change the rules of the road? If the rules of the road are inappropriate and encourages reckless and predatory driving, regulators cannot solve the problem. Impact of reckless, predatory or misleading practices on competitors (supply): (a) cautious & low cost providers lose market share; (b) predators set standards; (c) increase cost and risk for all participants on consumers (demand): (a) unable to evaluate options, bad choices; (b) inflated finance cost reduces wealth; (c) lose homes, unable to meet social obligations on society: sub-optimum allocation of resources; biased against efficient finance options; social welfare resources diverted to debt payment & financial sector Therefore, have to review all aspects of credit legislation,to remove incentives for adverse behaviour, prevent participants from passing cost of adverse behavior on to competitors or society. Assess systemic implications of transactional incentives. Create a sound basis for the contractual engagement between credit providers & consumers. Executive Summary - 3Philosophy & analytical framework “if a system produces unacceptable outcomes, cannot expect outcomes to change until we change the system”, Niccolo Machiavelli

Disclosure Too late to affect purchase decision / misleading, undermine price comparison benefit high cost suppliers / complex disclosure on complex products undermine consumer ability to make informed choices. Negative option marketing & automatic increases in credit limits Undermine choice, comparison of cost, competition. Increase debt stress. Add-on fees & credit life insurance inflate cost, undermine disclosure & product comparison. Favour predatory operators & undermine competition. Early settlement penalties, penalty fees, debt collection fees Not transparent, subject to price comparison. Reduce switching & competition. “Debt farming” based on penalty fees & debt collection fees, benefit predators & increase default by vulnerable consumers Preferential collection mechanisms & easy access to court orders for debt collection Encourage predatory lending & over-indebtedness APR disclosure & deregulated interest APR biased against small transactions; High i% abused in marginalised market segments Credit bureaus Weak, incomplete & biased credit information. Undermine creditors’ client selection & risk management. Insufficient debt rehabilitation mechanisms Increasing pool of marginalised & debt stressed consumers. Increasing risk & fraud. Weak regulation (monitoring & enforcement) Undesirable practices & trends not detected. Allow predators to set standards. Executive Summary - 4Incentives for adverse behaviour

Weak, misleading & manipulative disclosure + adverse incentive structures prevent credit market to function in an optimal manner Market segmented into ‘shark pool’ and main stream. Lower standards for low income market, discourage main stream suppliers from serving low income market. Even when entering, following pricing of existing suppliers. Reduced supply & competition & increase cost. Disclosure not reflective of true cost or risk. Consumer unable to make choices that would drive optimal outcomes Low income consumers have little access for to home loans & main stream credit. Excluded from asset growth. “… every individual … can, in his local situation, judge much better than any stateman or lawgiver can…” Adam Smith

Results, MFRC & Credit Law Research:-Levels of debt stress & the cost of doing nothing • Credit Law Review:- increasing debt stress, as result of (a) reckless credit extension, (b) little attention to affordability assessment, (c) 1000’s of lenders not using credit bureaus, (d) vehicle & other lenders focus on security, rather than affordability, (e) collection preferences, (f) easy access to courts for debt enforcement, even on loans granted recklessly.

MFRC & Credit Law Research:-Cost of Credit - impact on consumers, cost of doing nothing: Credit Law Review:- cost for low income credit very high, 100%+ not unusual; in prime markets, actual cost also far above usury cap; huge impact of additional fees & credit life insurance; actual cost well above disclosed interest rates; disclosure meaningless & competition dysfunctional; cost ( & risk) reduction from economies of scale or collection preferences not passed on to consumers; no integration between main stream & low income markets; cheaper main stream products such as credit cards not available to low income market … low income consumers marginalised!

Question: What are the causes for such significant market failure?

Disclosure: standardized, comparable, early. Prescribed content & format. Enable price comparison. Negative option marketing prohibited, automatic increases in credit limits curbed. Reckless credit: Require affordability assessment. Define reckless credit, affects enforceability. Protect responsible lenders. Interest rates & fees: Change basis of disclosure. Upper limits on interest & fees. Limit add-ons. Early settlement penalties removed. Debt collection fees regulated. Curb incentives for ‘debt farming’. Preferences & anti-competitive conduct prohibited, monitored. Agents & brokers, different disclosure requirements. Debt counselling to restructure income, rehabilitate consumers. Credit bureaus, registered, monitored … regulated. Dedicated regulator, to monitor & enforce. Compliance reviews by auditors; investigations; market practice reviews, compliance notices. penalties through Tribunal (“special court”). Executive Summary - 5Changes implemented through Credit Act

Interest, fees & credit life insurance Reckless lending rules Marketing & sales practices National Credit Act Enforcement & debt collection Agreements & quotes Unlawful agreements, provisions Debt counselling Regulate Credit Bureaus Create National Credit Register

Intention Provide information on credit cost at early stage of purchase cycle. While consumer is ‘shopping around’. Improve comparability. Greater honesty in advertising Consumer must agree, before an agreement can come into effect Increase agent & broker transparency & accountability How Negative option marketing & automatic limit increases prohibited = unlawful agreement Prescribed pre-agreement quote, binding for 5 days Prescribed info in credit adverts Opt-outs on telemarketing campaigns, information on-sold Limits on marketing & sales @ home & work Prescriptions on agents & brokers (ID in contracts, fee disclosure, liability for credit providers) “… curb undesirable marketing and sales practices & practices of credit intermediaries” S74 – S76, 89(1)b, 119(4)

Intention Reduce reputational risk which APR disclosure impose for main stream suppliers providing small loans, Payday lending: penalties for roll-overs, for incremental increases in loan sizes Curb ‘debt farming’ on small loan defaults, from collection fees & penalty interest How Disaggregate interest from initiation and monthly fee, impose limits on each Prohibit penalty fees and penalty interest Curb early settlement penalties Prohibit ad-hoc interest rate variations (e.g. teaser rates) Codify “in duplum rule” – (interest + fees post default limited to 100% of capital) Single premium credit insurance prohibited, only monthly premiums on declining loan balance “… usury limits & APR disclosure segments market into ‘‘prime market’’ and ‘‘marginal market’’ … regularly circumvented … misleading disclosure … little benefit to majority of population …” • S100 – S106

Interest & fees disaggregated, with structured limits depending on product type Credit facilities Mortgages Other secured credit Unsecured Short term Development credit Interest = RRx2.2+x% Initiation = R150 + m x loan < max limit ($125 / $625) Service = single monthly amount < $6

“… focus to shift from price control to protection against over-indebtedness + penalties on predatory lending practices” Intention Penalise predatory lenders Assist consumers who are in desperate positions Protect responsible credit providers from impact of reckless operators “Normalise” low income credit market … often a marginalised shark-pool S78 – S88, S130 How Reckless credit • Over-indented = “per available information, consumer will be unable to satisfy in a timely manner all the agreements to which the consumer is a party” • Reckless = (1) no assessment; (2) consumer did not understand obligations; (3) agreement made consumer over-indebted • Subject to consumer “fully & truthfully disclose” If reckless, impact on court • No court orders for debt recovery; Court may suspend or reduce obligations Debt counselling • Registered debt counsellors, with statutory debt restructuring process • Recommend debt cancellation or restructuring for review by court Prohibition of preferences most important

Requirements of NCA Credit bureaus registered Statutory obligation & liability for data quality Compliance audits Consumer access to records, complaints process, data removal for credible complaints Intention Efficient effective access to credit information, particularly, for low cost provision of small loans Pro-active regulation of bureaus to ensure credibility Privacy laws inappropriate, credit market requires accurate & efficient credit information “credit bureaus critical for credit assessment, to prevent credit bubbles, to curb debt stress. Not sufficiently regulated”

Requirements of NCA Courts powers substantially increased to assess compliance in case of legal action Intervene if reckless or over-indebted Regulator Registration; Monitor market conduct (& report to parliament); Compliance; Redress Instruments: Notice of non-referral; ‘undertakings, resolutions & agreements’; compliance notices, Tribunal action Tribunal Status of “specialised court”, subject to appeal to high court; Significant fines & deregistration Intention Prevent non-compliant lenders gaining a competitive advantage, setting the standard Legal cost means reliance on consumer litigation totally inappropriate Enforcement, to change conduct, ensure interventions have the intended impact “effective enforcement critical, to change market conduct of participants” S13-16, S54/55, S129/130, S138

Dramatic change in all aspects of market behaviour, impacting both on prices & debt stress Some examples only Reduced cost in most high cost segments, + reduced credit life insurance Disclosure resulted in price reduction, both as result of consumer pressure and comparison between credit providers Without negative option marketing, greater debt run-off Removal of preferences & reckless rules – greater focus on affordability Change in mortgage & motor vehicle lending, to consider debt burden (not only credit record & repayment as % of income) Debt collection practices much more restrained, increased economic basis, less predatory Dramatic change in court’s treatment of cases for debt enforcement Scrutiny of credit provider behaviour; Repossessions; Default judgments; Reckless lending practices Debt Counselling create statutory mechanism to deal with impact of fin crisis; In response to fin crisis, credit providers consider debt restructuring as 1st choice, rather than repossession NCR monitoring & enforcement action Against credit bureau - audits revealing massive weaknesses in data management against predatory lending to strip housing equity against “loan sharks” supporting debt counselling NCR statistics allowed more detailed assessment of impact of fin crisis; NCR focus on consumer credit market enable pro-active response Executive Summary - 6Impact since implementation

Impact of the Act On credit granting practices On credit marketing & disclosure On debt enforcement On the contractual relationship between credit providers & consumers

Consumer Credit Market in South Africa 17,8 million Credit Active Consumers Credit Providers US$142 bn consumer credit 3,971 credit providers 32,311 branches 1,252 Debt Counsellors

Credit Bureau StatisticsDebt stress & defaults Through credit bureau statistics, monitor trends in credit market performance Audits & compliance notices, quality of data improved, political pressure diminished Information critical to combating over-indebtedness; critical to efficiency of credit market … must be regulated!

Job losses by LSM – severe impact Monitoring the impact of the financial crisis

The NCA changed the consumer credit market in a number of ways … Integrating previously capped Usury market with exempt market for micro-loans Price reductions in most segments, biggest in micro-loans & furniture finance Improved quality of access for the low-middle income consumer Increased transparency & competition Furniture Finance – R5,000 Store Cards – R1,500 Impact of the Act on cost of credit Feasibility Consulting

Impact of the Act Debt Counselling, debt enforcement • 1,036 debt counsellors registered, with independent payment distributors. Extensive monitoring + support mechanisms + investigations & enforcement. • 116,000+ applications cumulatively, growing at 9,000 pm. Monthly distributions to creditors now above R100 m • Despite challenges, debt counselling already playing a huge role in mediating between debt stressed consumers and credit providers. Resulting also in change in credit provider behaviour towards debt-stressed clients • Massive change in approach of courts, using requirements of Act to intervene in cases

Debt Counselling Case studies to illustrate profile of consumers

Concluding observations:- • Impact of NCA: curbed excesses, creating basis for lower but more sustainable credit growth – without courts acting as debt collectors, curbing social cost of reckless lending • Debt counselling – reconcile claims of different credit providers, creating sustainable repayment stream on non-performing consumer • While minimising social cost, • And, lets not forget the hard-selling that took place in the good times! • BUT, significant implementation challenges • Fall-out from debt stress still increasing, driven by loss of variable sources of income as much as loss of employment. • On-going external impact of financial crisis, with risk of 2nd fall post stimulus • In response to crisis, important to focus not just on protection of industry, but also on protection of households, • noting that crisis impacts differently on different consumer groups • loss of income & loss of employment each have an impact • the longer the downturn lasts, the more households with high debt burdens run out of options

Thank You ! www.ncr.org.za