Download

1 / 6

60 likes | 64 Views

Depending on the laws for your state, you may want to file bankruptcy to protect your home. At that point, the judge can order you to give up your property or other possessions as payment toward your debt, based on the type of bankruptcy you pursue.<br>

E N D

Money Matters Consequences of Ignoring Credit Card Debt https://flyerfunnel.com/

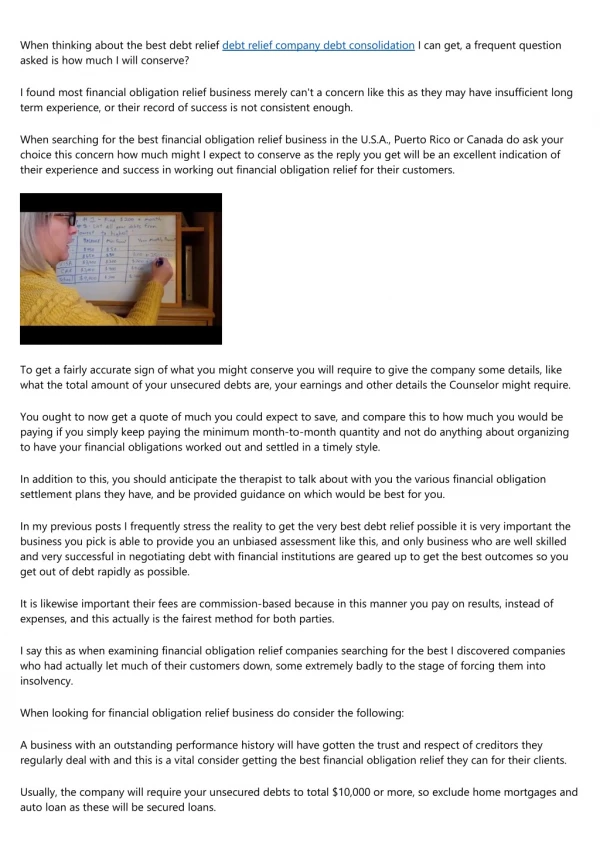

Q: My husband, Todd, and I have gotten into some trouble with credit card debt. We owe over $6,000 on one credit card and about $18,000 on another card. We were barely able to keep paying the minimum monthly payments, and then Todd’s company closed down 2 months ago.Since then, we paid the monthly minimums for both of them the first month he had no job. The second month just passed and we were unable to pay. I don’t see any hope that we can ever pay even one of these minimum payments until Todd finds another job, and that’s not looking good right now.I guess we were hoping that, since so many people out there are in the same fix as we are, that no one would notice that we were no longer paying these bills. We’d like to just walk away from these debts. We’re sorry we charged these cards up so high. We’d intended to pay it at the time, but now, we most likely never will.What exactly will happen to us because we stopped paying these two credit card bills?

A: Unfortunately, many people are in the same boat as you and Todd. Even so, there’s no real chance that you’ll get away from nonpayment for these two bills scot-free. After your 30 days past due, most debtors will make efforts to contact you by phone or mail and ask you to pay your bill.Your best course of action would be to contact your debtor before the company contacts you and let them know your situation. In fact, if you call them before the payment you’re about to not pay is due, that’s the best plan of all.Your goal should be to try to work out a reduced payment plan that you can realistically stick with.

CollectionsWhen you’re 2 months overdue: calls and contacts from the debt company will be less pleasant. It’s likely the company will turn your account over to Collections. This isn’t good news. Collections will try to pressure you to pay your bill.Plus, more fees will be piled on to what you owe (such as late fees and additional interest costs). If there’s good news, it’s that you can still directly contact the debt company and try to work out a payment plan.Once you’re past due by 90 days: the account will most likely be shut down and collectors will be quite aggressive in their efforts to get you to pay. Some experts actually recommend never paying the collections companies and insist you go back to the original debt company.The 90 day mark tends to be the window during which the debtor will report your non-payment to the credit bureau. Still more late fees and interest fees are being added at this time.After this stage, you can try to negotiate a reduced amount to pay back. For example, for the $6,000 bill, you can offer to pay back in total $3,000. If the company accepts your offer, you must pay it off right away.

LawsuitsIn the event you continue not to do anything about the bills, the credit card companies can sue you for non-payment. Then you’ll end up in court and the creditors may win judgments against you and even put liens on your home if you’re the owner.Depending on the laws for your state, you may want to file bankruptcy to protect your home. At that point, the judge can order you to give up your property or other possessions as payment toward your debt, based on the type of bankruptcy you pursue.Your Best BetIn essence, your very best plan is to contact the individual debt companies immediately and work something out. Otherwise, these companies are simply going to keep piling on fees making it more difficult for you to ever pay off the quickly-rising balances and preserve your good credit. Good luck!

Sign up Today https://flyerfunnel.com/