Download

1 / 30

310 likes | 489 Views

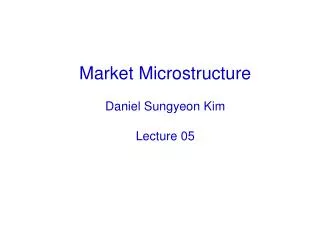

Market Microstructure Lecture 04 Daniel Sungyeon Kim. Transaction Cost Measurement. Request. Request. Request. Order. Order. Order. Fund A Fund B Fund C Manager Manager Manager Selection Order Desk Implementation

E N D

Transaction Cost Measurement Request Request Request Order Order Order Fund A Fund B Fund C Manager ManagerManagerSelection Order Desk Implementation Exchange 1 Exchange 2 Exchange 3 Transaction cost measurement deals with alternative ways of measuring implementation costs

Liquidity and Transaction Cost Measurement Q: What are the major components of transaction costs?

Five Transaction Cost Meas. Methods Five methods for measuring a security trader’s Implicit Transactions Costs. One method also includes the security trader’s Missed Trade Opportunity Costs All five methods have the same general form: One-Way Implicit Cost of Trading for a single trade = (# of shares) (price – benchmark) for buys (# of shares) (benchmark – price) for sells Round Trip Implicit Cost of Trading = 2 * One-Way Implicit Cost of Trading Cost of many trades = Sum of the cost of each trade The five methods differ in what they use as the benchmark

Live exercise in Five Transaction Cost Measurement Methods All are based on the same Trades and Quotes at top Request from fund manager at 10:15: buy 800 round lots You do two trades: 350 and 270, leaving 180 unfulfilled Other traders do two trades: 500 and 220 Now lets compute the cost of trading five different ways

(1) Effective Spread • Benchmark = Midpointat time twhen the trade happens (or when the order is received) =

(2) Realized Spread • Key idea: the trade itself reveals information • Buy implies good news midpoint moves up • Sell implies bad news midpoint moves down • Benchmark should be the post-trade midpoint = Midpoint 5 minutes after the time of trade (or 5 minutes after the time the order is received) • = • Realized spread = market maker’s realized profit margin, net of the midpoint movement = trader’s cost

(3) Implementation Shortfall Benchmark = Midpoint when the request is send to order desk = $31.85 in this example Adds Opportunity Cost = (Shares not bought) * (Closing midpoint – Request midpoint)

(4) Volume-Weighted Average Price (VWAP) • VWAP = sum (trade price * volumes traded)/total traded volume • Problem: VWAP can be gamed, if the order desk can choose what day to trade on • If prices are falling, buy today • If prices are rising, buy tomorrow

(5) Closing Price Method Benchmark = closing price of the day = same as reported on the web or in the newspaper when the exchange is closed = $33.41 in this example

What Method for Informed? Q: Focusing on trade midpoint of effective spread vs. request midpoint of implementation shortfall, which is the best to use if you are an informed trader?

What Method for Uninformed? Q: Regarding the trade midpoint of effective spread vs. request midpoint of implementation shortfall, which is the best to use if you are an uninformedtrader?

In Example #2,the benchmarks under effective spread for your first and second trades are: • $45.24 and $44.99 • $45.27 and $45.01 • $45.64 and $45.62 • $45.23 and $44.96

One way effective and realized spreads? Add Demo Notes

In Example #2the benchmarks under Realized Spreadfor your first and second trades are • $45.24 and $44.99 • $45.27 and $45.01 • $45.64 and $45.62 • $45.23 and $44.96

In Example #2, the benchmarks for the implementation shortfall and closing price methods are: • $45.72 and $44.87 • $45.95 and $44.87 • $45.95 and $45.01 • $45.72 and $45.01

What is the implementation shortfall? Add Demo Notes

Credit Suisse Tool “ExPRT” = Credit Suisse transaction cost model Core is Implementation Shortfall; cps = cents per share; bps = basis points per share; 1 basis point = 1/100 of 1% 16 basis points = 0.16% = .0016

Credit Suisse Tool Implementation Shortfall = Execution Price – Arrival Price Where “Arrival Price” = “Request Midpoint” Their version = no opportunity cost component What is the participation rate? Participation rate = (your $ volume in a time period) . / (total $ volume in same time period) Why break down the analysis by participation rate? Tells you how rapidly the whole trading request is filled Ex: 1% of volume = slow = little impact on price Vs. 30% of volume = fast = major impact on price (Notice that “Impact Cost” gets bigger (more negative) for larger participation rates)

Time periods • During period = starts when the request arrives and ends with last execution = same as Implementation Shortfall • What is the Before period? • Before request arrives • What is the After period? • After last execution • No matter if you are buying or selling, the convention is: • positive values = profit = good • negative values = cost = bad • Implementation Shortfall is broken into three component as explained in more detail on next slide

Three Components of Implementation Shortfall • Implementation Shortfall = Execution Price – Arrival Price • Trading Alpha = Execution Price – VWAP • If positive, you beat the market • If negative, the market beat you “Your trading skill” • Impact Cost = VWAP – Adjusted VWAP = (Your % participation) * (Trend cost) = How much you moved the price against yourself Always negative cost • Trend Cost = Adjusted VWAP – Arrival Price • If you are buying, price uptrend is negative buy at higher price .vs. downtrend is positive buy at lower price • If you are selling, price uptrend is positive sell at higher price .vs. downtrend is negative sell at lower price “How lucky your timing was”

Before and After Portfolio manager (PM) delay could be costly if some of the same information comes out overnight (“gap cost”) or daytime before the request (“delay cost”) Aggressive trade moves the price against you; could show up when stock price reverts (“reversion cost”)

More Before and After Why keep track of what happens to the stock price all the way out to T+5? If positive trend out to T+5, then trade slower If negative trend out to T+5, then trade faster If flat out to T+5, then it doesn’t matter

Exhibit 15 • Results: • What happens to Average Shortfall Cost as Trade Size is increased? • What happens to Average Shortfall Cost as Aggression % is increased? • Two dimensions are: • Trade size = (your share volume) / (Average Daily Share Volume) = How difficult whole trading program is • Aggression % = Participation rate = (your $ volume in a time per.)/(total $ volume in same time per.) = How rapidly the whole trading program is filled