Download

1 / 16

160 likes | 247 Views

Food Security and Mealie Meal Prices Dynamics - (What are the Medium and Long Term Solutions?). Presented by Eric Chipeta, FAO Representation in Zambia. Presentation Outline. Introduction : Historical Perspective and Status of Maize Stocks in Zambia

E N D

Food Security and Mealie Meal Prices Dynamics - (What are the Medium and Long Term Solutions?) Presented by Eric Chipeta, FAO Representation in Zambia

Presentation Outline • Introduction :Historical Perspective and Status of Maize Stocks in Zambia • Maize Meal Price Spikes and Maize Pricing Issues in Zambia • Production costs/ Supply side • Demand Side Factors • Transparency in Millers’ Pricing Model • Role of FRA • Policy implementation on maize exports and imports • Solutions- Medium Term and Long Term • Conclusion

Introduction :Historical Perspective and Status of Maize Stocks in Zambia • Food security dimensions are physical and economic access, frequency, quantity • Fluctuations in prices have been common since 1980s • Mealie meal Price decontrol in 1987 resulted in increases in prices and riots • Liberalization policies in the 90s brought its own challenges and opportunities • Government responded to challenges by setting up FRA.

Introduction :Historical Perspective and Status of Maize Stocks in Zambia • Zambia has the stocks of maize according to the balance sheet (1,661,626 metric tones) • The maize stocks at the time of reporting could carter for the national requirements (1,300,000 metric tones) and leave a good surplus (361,626 metric tonnes). • Bumper harvests have been recorded for the past 3 consecutive seasons (2009/2010, 2010/2011, 2011/2012) 2,795,483, 3,020,380 and 2,839,157 metric tons respectively (CSO Bulletin 2009 and 2012).

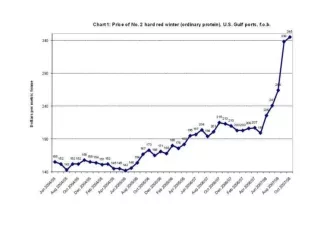

Maize Meal Price Spikes and Maize Pricing Issues in Zambia • Demand and supply affect pricing. • During times when maize is in short supply mostlybetween November and April, prices are higher. • Notably, last quarter of 2012 there was an increases far beyond the seasonal price changes from about ZMK40,000 to about ZMK80,000 which was close to 100% increase • This has been a source of concern • The government finds itself in an awkward position as it makes effort to give farmers a good price while striving to ensure that consumers access the Mealie meal at a low price. • This has resulted in substantial hemorrhaging of huge financial government resources.

Production costs/ Supply side • 50kg maize bag pricing could be comfortably pegged between K40,000 and K45, 000 • Evidence from FSRP/IAPRI indicates that setting of floor price has not benefitted from national farm survey evidence on production costs. • It is also notable that production costs vary from one area to another which makes it more costly in certain places to produce maize than in others. • For instance, while FRA price was pegged at ZMK65, 000 per 50 kg bag in 2010, the average production cost of maize in Eastern and Northern Province was at ZMK 34,000 while Copperbelt and Western Province stood at ZMK 53,000. • It therefore goes without saying that the pan territorial pricing that FRA sets need to benefit from evidence generated by surveys carried out by research institutions. • Huge investments through FISP not bearing as much fruit given that most small scale farmers still remain at productivity of about 2 mt per ha

Demand Side Factors • Use of grain as stock feed, breweries and other products has exerted pressure on the maize stocks. • In spite of the third successive bumper harvest with about a million metric tonnes above the national requirement, the strong demand from neighboring countries such as DRC and Tanzania supported by gradual depreciation of the Kwacha has put upward pressure on prices. • This has been reported several times through the media over the years and particularly this season (2012/2013)

Role of FRA in the market • FRA has consistently gone beyond its mandate to ensure that the strategic grain reserves are maintained at 300, 000 at any given time as strategic reserves • Offloading of FRA maize as a price stabilization mechanism tends to distort the market prices to some extent • Benefit transmission to consumers of the offloaded maize is not assured • Untimely/Unclear pronouncements by government in some cases, millers decide to hold on to their stocks of maize since offloaded maize from FRA could be cheaper which could bring confusion to the millers

Medium Term and Long term Solutions/Way forward Government to work with stakeholders on floor price setting for maize. When the option of leaving price to be determined by demand and supply equilibrium, safety nets should be in place to safeguard the part of the population that would be negatively affected based on the vulnerability assessment. There is need to have a strong mechanism that encourages FRA, millers and other stakeholders to report maize and Mealie meal stocks. FRA’s offloading of its grain on the market to be according to agreed guidelines and triggers that do not stifle private sector participation in the market. Maize export predictability in the context of good estimates of expected export levels to determine export quota allocations, enforcement and M & E. The demand in neighbouring countries is an opportunity that Zambian farmers can exploit by increasing production and productivity that supplies local markets as well as export markets.

Medium term solutions cont... • Coordination mechanism that facilitates dialogue of different players and government in maize market sector. • Private sector including cooperatives to be given more space in maize market in the country • FRA to restrict its operations to areas where private sector participation is not profitable. • In addition, pan territorial pricing need to be removed to ensure pricing reflects different average production costs that obtain in different regions. • Millers to enhance their storage capacity through mechanism that include PPP. • Stock management and information system that provide real time and credible information on request to be developed and deployed. • There is need to promote resilience in the farming systems through use of conservation agriculture, crop diversification and early warning systems.

Long Term Solutions • Work of FRA operations to be within the mandate of procuring the strategic grain reserves to avoid market distortions and crowding out of private sector • FRA to incrementally reduce its marketing activities to allow private sector respond to emerging opportunities • There is need to have a coordination mechanism that facilitates dialogue on actions that need to be taken by different players in the maize market sector especially on matters such as export bans, offloading of FRA maize to the market and benefit transmission mechanisms to ensure that lowly priced maize reflects in consumer prices.

Long Term Solutions cont. • There is need for more transparency and coordination in the manner that FRA makes its decision. • Strengthen cooperatives to effectively participate in the marketing of grain in Zambia • Promotion of substitute cereals apart from maize driven in part by promotional campaigns to support processing & consumption of other food crops • Processing and value addition of other crops to reduce postharvest losses and increase the wealth creation opportunities. • Enhanced cross border maize trade surveillance protocols and programme/system • There is need to develop and introduce compulsory market and trade information reporting for all market players • Private sector including the cooperative movement to be given more space in maize marketing space in Zambia

Long Term Solutions cont.. FISP to be reformed to address targeting, governance, complimentary extension service, timeliness in delivery of inputs and participation of more goods and service providers. This could be facilitated using e voucher as an input delivery mechanism, involvement and empowerment of local leaders, updated farmer registers. Government and private sector to move from adversarial relations to partnerships that foster trust and predictability in the markets Productivity needs to be enhanced for small scale farmers to be competitive so as to achieve food security, wealth creation and access to financing opportunities to graduate to higher levels and modernize agriculture Invest in infrastructure on storage and roads

Concluding Remarks • The problems and solutions are by and large understood and agreed by stakeholders. • There is need to take decisions that will assist move the country from vulnerability (food insecurity shocks) to prosperity and stability. • Stakeholders and government need to work together to address the issues in the sector so that food security and wealth creation is optimized. • Politicization of the issues surrounding food security must be set aside so that beyond political affiliations, actions that support progress are taken. Time to act is now! • Thank you for your attention

References • Arimond M and Ruel T M, (2004). Journal for Nutritional Sciences 2004) • Burke, W.J. et al (2011) The Cost of Maize Production in Zambia FSRP Lusaka • Carlo del Ninno, , Paul A. Dorosh, KalanidhiSubbarao (2007). Food aid, domestic policy and food security: Contrasting experiences from South Asia and sub-Saharan Africa. The World Bank, Safety Nets, Social Protection and Labor, 1818 H Street, NW, Washington, DC 20433, United States • Chapoto A (2012) The Political Economy of food Price Policy- The Case for Zambia IFPRI / United Nations University • Dorosh, P.A. 2007 Alternative Approaches for Moderating Food Insecurity and Price Volatility in Zambia FSRP Lusaka • FAO 2012 A Brief Assessments of The Agriculture Market and Trade in Zambia, Lusaka • FAO (2012) Maize Marketing in Zambia- Support to the FRA Activities, Lusaka • FAO (2012) Media Questions Regarding Food Prices Increases, Rome • FAO (2012) High and Volatile Food Prices- FAO Support to Country Level Contingency Planning Rome • FAO (2008) Rising World Food Prices Implications on the Zambian Economy, Lusaka • Timmer Peter N, (2008). Causes of High Food Prices. ADB Economics Working Paper Series No. 128 • FSRP (2005) Zambia’s 2005 Maize Import and Marketting Experiences: Lessons and Implications FSRP Lusaka • FSRP (2002) Markets need Predictable Government Actions to Function Effectively: The Case of importing Maize in Times of Deficit FSRP Lusaka • Henk-Jan Brinkman, Saskia de Pee , IssaSanogo , LudovicSubran , and Martin W. Bloem. 2010. High Food Prices and the Global Financial Crisis Have Reduced Access to Nutritious Food and Worsened Nutritional Status and Health. J. Nutr. January 2010 vol. 140 No. 1: 153-161 • Mason, M.N & Myers, R.J The Effects of the Food Reserve Agency on Maize Market Price in Zambia FSRP Lusaka • Minot Nicholas, (2010)(IFPRI). Food price stabilization:Lessons for eastern & southern Africa. Presented at the Comesa policy seminar “Risk Management in African Agriculture” on 6-7 September 2010 in Lilongwe, Malawi under the Comesa-MSU-IFPRI African Agricultural Markets Programme (AAMP)