Download

1 / 14

140 likes | 268 Views

Micro Lending in the 21st Century: Approaches for Success in the Egyptian Economy. Dr. Khaled F. Sherif. Background: Egypt’s Economic Strengths and Weaknesses. Large GDP: 50 th in the world (World Bank - 2006) Strong macroeconomic environment: Inflation and fiscal deficits under control

E N D

Micro Lending in the 21st Century:Approaches for Success in the Egyptian Economy Dr. Khaled F. Sherif

Background: Egypt’s Economic Strengths and Weaknesses • Large GDP: 50th in the world (World Bank - 2006) • Strong macroeconomic environment: • Inflation and fiscal deficits under control • Debt profile sound • Continuing growth of exports • High reserves • Large labor force Economic Strengths Economic Weaknesses • Low Gross National Income (GNI) • Significant unemployment • Poor literacy rate • High levels of poverty • Poor perception related to the business environment • Economic reforms are ongoing but not complete

Background • Egypt has introduced a multitude of reforms in recent years to: • Increase levels of competitiveness, • Accommodate job creation needs, • Improve human development needs, and • Sustain GDP growth under stable conditions. • Despite significant progress in a number of sectors, one of Egypt’s most significant challenges remains the lack of access to microfinance and micro lending for entrepreneurs.

Background • For Egypt to effectively confront the challenges of the 21st century, a radical strategy must be pursued to build up microfinance and micro lending. • This presentation seeks to outline a strategy that facilitates this, supported by strong institutions and economic structures at the national-level. • The focus of this strategy is on facilitating access to microfinance at the local level, in order to stimulate intrinsic growth and create enough disposable income for the local population. • The concept is to break the prevailing cycle of poverty that we see in the lower economic classes.

Target Groups • Microfinance efforts would focus on the development of effective Microfinance schemes targeted at the ‘poorest of the poor’ • One component would involve a tie-in to the new mortgage law, seeking to assist with helping citizens own their own homes, with a second component focusing on small and medium enterprise (SME) development • Nobel laureate Mohamed Yunus developed a similar program to the micro-loans initiative in this context, turning $27 in funding into $15 billion in Bangladesh • The initiative would support loans of $500 or less for local populace to help them meet short-term funding needs

Microfinance Short-Term Micro-Loans • The micro-loans program would involve providing SEED capital for small business loans through an existing microfinance agency (social fund, a local state bank, or other) that would assist in the creation of 600 businesses in the pilot governorates selected • These loans would fund small-scale projects that have substantial room for growth, and would be jointly managed by an enterprise development team • These SMEs could include Employee Stock Ownership Plans (ESOPs) at inception, and be owned by the labor force employed • The SMEs created would originate from ideas provided by the local populace.

Microfinance • The managing institution would review these ideas and decide which should go forward. • This institution would have a management team that could assist with legally establishing the business, buying the requisite machinery or equipment needed and in managing the assets for a period of no less than three years to ensure profitability. • The business owners will essentially be its workforce, and the locals that had pushed for its inception.

The Management Team • A major component of the Microfinance strategy is having team, who are also charged with providing management support, advisory services, technical assistance and helping entrepreneurs achieve a threshold of success: The Microfinance Process Government advertises the availability of SEED capital Assistance with creating the business (e.g. incorporating, etc.) Providing funding support to the business Local entrepreneur comes in to propose an idea for a business Business selection process Assistance with business start-up (e.g. selecting/buying machinery, etc.) Business Creation Team helps him/her to develop a feasibility study PROFIT Support for business management (e.g. accounting, marketing, etc.)

MicrofinancePart III The Microfinance Process Business Creation Team Composition 200 Companies per Year Accounting Support Team:15 Individuals Marketing Support Team: 20 Individuals Business Selection Team: 15 Individuals 3 Years (600 Companies Total) Average Capital 50,000 to 100,000 L.E. Production and Training Support Team: 20 Individuals Management Support Team: 15 Individuals Business Start-Up Support Team: 15 Individuals Total Capital of 30 to 60 million L.E.

Management and Ownership • Companies that are established under the microfinance program will be developed under a unique ownership structure– designed specifically to promote wealth creation • Specifically, the ownership structure will facilitate wealth transfers to both the companies owners and its employees, with a portion of the ROI the company generates going directly back into the microfinance program (to support the funding needs of new companies under the microfinance program) • The management team would authorize the salaries of the owners and employees, to ensure that a fair and un-inflated salary is designated to those working for the company • Moreover, this team would be required to approve any and all profit sharing initiatives that would take money directly out of the company

Ownership Structure Owner(s) 55 percent Employees 15 percent Microfinance Funding Vehicle 30 percent Owners who are responsible for developing the business concept and day to day management of the enterprise 15 percent of the company’s shares will be held to be distributed to employees that work for the company to ensure that they benefit from the company’s success 30 percent of the shares will be owned by the funding vehicle, and proceeds from the sale of the company and/or any distributions of its profit would be channeled back to fund new entities • The Business Creation Team would be required, under the legal structure of the company, to sign-off on any and all financial decisions that exceed a certain threshold (e.g. 1,000 L.E.) to ensure that we avoid asset stripping

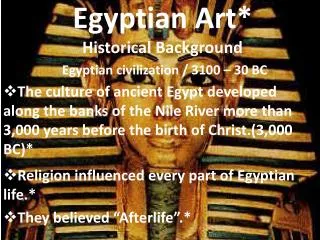

Capital Structure Decision Making • Microfinance institutions today have an increasingly broad range of financing sources at their disposal. This allows for greater funding diversification, but it also makes decisions about capital structure more complex. • The top priority for MFI managers is to obtain the lowest cost funding, but they do not all calculate the fully loaded cost of all debt instruments • Better capital structure decision-making minimized risk, maximize financial flexibility and encourage the long-term solvency needed to provide sustainable access to finance to the poor • Cross-border financiers cognizant of the impact their funding has on the development of domestic markets. The focus cannot be solely on ROI, but also also domestic financial systems that provide a wide range of services for the poor.

Risk vs Return Source: CGAP

Key Lessons from Experiences • Balance of the market function and government role: There is a strong need for the Government to plan when to reduce its role (as the market grows) and when to intervene. • Governments should invest in technology innovation for long-term development • Private investment funds, known as microfinance investment vehicles (MIVs) have been growing significantly over the past four years—many of which are socially responsible investors (with returns close to money market)