Download

1 / 62

650 likes | 1.02k Views

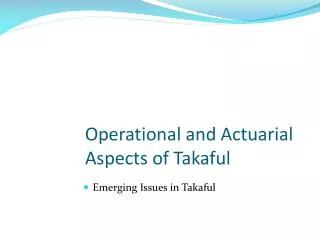

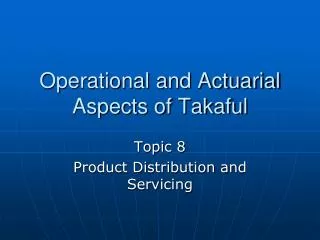

OPERATIONAL AND ACTUARIAL ASPECTS OF TAKAFUL. Development of Insurance and Takaful and its Regulatory Aspects. TAKAFUL OVERVIEW. Participants. Actuary Monitor & Review Pricing Valuation. Shariah Advisors Shariah Compliant of Operations & Governance. Operator Scheme Design

E N D

OPERATIONAL AND ACTUARIAL ASPECTS OF TAKAFUL Development of Insurance and Takaful and its Regulatory Aspects

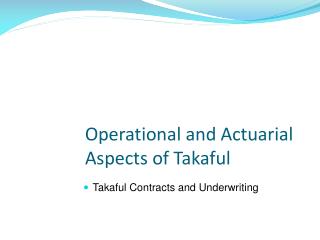

TAKAFUL OVERVIEW Participants Actuary Monitor & Review Pricing Valuation Shariah Advisors Shariah Compliant of Operations & Governance Operator Scheme Design Administration Distribution Collections Underwriting Investment Claim payments Risk management Retakaful Contributions $$$ Wakalah Fees Tabarru’/Donation Mudarabah Takaful Fund Investment & Returns Claims & Benefit Payments Taa’wun/Mutual Assistance Regulators Licensing Regulation Supervision Standards Setting Customer Protection Promotion Surplus/Deficit Participants top up and shares Operator advances and shares

INTRODUCTION • Risk a major component of our environment; human is surrounded by innumerable risks from birth to death; human learned to improve after experiencing misfortunes; quest for security evolved since the dawn of man’s existence; • According to Braise Pascal : “As each generation progressed they will learn at least a part of what their earlier generations had learned”. • Abraham Maslow’s hierarchy of needs: • Survivable • Security • Love and Belongings • Self esteem • Self actualization

Definition of Insurance The term Insurance in its real sense, is community pooling, to alleviate the burden of the individual, lest it should ruinous to him: “the simplest and most general conception of insurance is a provision made by a group of persons, each singly in danger of some loss, the incidence of which cannot be foreseen, that when such loss shall occur to any of the, it shall be distributed over the whole group”. In sum, the aim of all insurance is to make provision against the dangers which beset human life and dealings. [1] Insurance in Encyclopedia Britannica(eleventh edition) Vol 14.p.656

HISTORY OF INSURANCE & TAKAFUL DEVELOPMENT (a) Early Insurance Development : • Introduction of the contract of Bottomry by the merchants of Babylon about 4000-3000 B.C.; • Code of Hammurabi, 2250 B.C.; • Bottomry Contract adopted by the Phoenicians 1600-1000 B.C.; • The Greeks adopted it around 4 B.C; • Later adopted by the Romans; • Thomas Gresham established the first Royal Exchange, 1570; • Life insurance first practical in 1583; • Lloyds of London established 1688; Lloyds Act passed in 1871;

(b) Takaful (early evolution) : • Diyat; pre-islamic; pagan Arabs; aqilah system • Adopted by Prophet; two situations: • Dispute between the two women from the tribe of Huzail; • Constitution of Medina, between Muhajirin and Ansar; • The aqilah system was utilized; • A fund known as ‘Al-Kanz’ was created to be used to pay compensation on behalf of members who are liable to pay diyat; • During the time of Umar the second Caliph, he ordered preparation of registers (diwan) in all parts of the Muslim State; names in the diwan owed one another mutual assistance;

Ibn’ Abidin (1784-1836) a Hanafi lawyer, became the first Islamic Scholar to come up with the meaning, concept and legal basis of an insurance contract; ( c ) Takaful in the Modern Era • The first modern Islamic insurance was formed in the Islamic State of Sudan in 1979; the company was based on the concept of cooperative i.e., The Islamic Insurance Company of Sudan; • As of 2008, there more than 150 takaful operators globally; • Growth expected to be between 15% and 20% annually; revenue expected to reach USD 7.4 billion by 2015;

(d) Development of Takaful in Malaysia : • Evolutionary phase; • Nurturing phase; • Consolidation phase; (e) Performance of the Malaysian takaful business: • The industry is about 25 years in operation; • 8 (+1) Takaful and 2 Retakaful operators in the market; • More than 40,000 agents are utilized; • Net contribution exceeded RM 2 billion; • Total Takaful Fund Asset exceeding RM 8 billion; • Almost 3,000 employees.

(f) Definition of Takaful : • The word ‘takaful is derived from the Arabic verb kafala which means to guarantee one another; to help; to take care of one’s needs; • “ A scheme based on brotherhood, solidarity and mutual assistance which provides for mutual financial aid and assistance to the participants in case of need whereby the participants mutually agree to contribute for the purpose”. (Takaful Act 1984) • Based on the principle of Ta’awun (mutual assistance) and Tabarru’ (voluntary contribution); • The operation of the concept must be within the spirit of Shariah;

(g) Muamalat in Takaful : • Nature of Takaful Contract; • Based on the concept of ta’awun and tabarru’ • Syariah compliant; • Element of Mudarabah; • Based also on the principle of al-Musahamah; • Scope of takaful contract; • Wide and flexible covers life, health and non-life risk • Subject to underwriting; • Regulated and supervised by the authorities; • Rational outlook of takaful; • Provide material assistance against unexpected financial losses; • Reduction of poverty in society; • Ensure security and produces a self-reliant society;

SHARIAH VIEWS OF INSURANCE: (a) Opinion of Scholars : • Majority of scholars are of the opinion that the conventional insurance practiced today is not Shariah compliant ; • However, many do not object to the concept of insurance per se but rather the contract ; • According to Dr. Yusuf Qardhawi :

“Our observation that the modern form of insurance companies and their current practices are objectionable Islamically does not mean that Islam is against the concept of Islam itself ; not in the least – it only opposes the means and methods. If other insurance practices are employed which do not conflict with Islamic forms of business transaction ; Islam would welcome them”. “The Lawful & the Prohibited in Islam” (pg. 276) • A Fatwa issued by a committee comprising of leading scholars for the Saudi Arabia Government have said :

“From the point of view of most Muslim jurists, cooperative (or mutual) insurance is not only permissible by the Shariah but also encouraged especially when looked at from the aspect of cooperation towards welfare. As such it is permissible for a bank to set up a cooperative (mutual) insurance company to function for the benefit of many activities but there is a need to state as clearly as possible in the contract of insurance that the amount of money to be paid by the participant is on the basis of donation to the said company which can be used for the purpose of assisting fellow participants who require assistance according to the terms agreed as long as these terms are not in conflict with the Shariah”

The National Fatwa Committee Malaysia deliberated on the question of life insurance (15th. June 1972) and below is a translation of an extract from the minutes recorded : “Life insurance as presently practiced by insurance companies is a fasid transaction as it is contrary to the Shariah principles of contract because it contains the following elements : • Gharar ; • Maisir ; • Riba As such from the Shariah point of view, insurance is haram”.

According to the late Tan Sri Prof. Ahmad Ibrahim in his paper “Towards an Islamic System of Insurance” (1982): • “The practice of insurance presently follows the western style of management and is therefore not in line with the teachings of Islam in a number of ways : (a) Many insurance contracts contain usury ; as it promises to pay more than the premium paid ; (b) Insurance companies invest the premiums which they have collected, in interest bearing investments; (c) The western method of insurance is a kind to gambling as one can lose the premium to insurance companies ;

(d) The western method of insurance contain the element of gharar and the contract is uncertain ; (e) Western insurance companies can earn profits or loss as a result of death or accident or risk to people”. • The above is a translation of an extract from the working paper of a committee known as “ Badan Petugas Khas ” set up by the government in 1982 to study the feasibility of setting up Islamic Insurance in Malaysia. • The “Badan Petugas Khas” also concluded that conventional insurance contract is fasid, however, the objection is not against the concept of insurance per se but against the existence of certain weaknesses in the insurance contract.

(b) Elements of Gharar, Maisir and Riba (i) Gharar : • Element of uncertainty in a contract ; • The Prophet was reported to have forbidden all transactions involving gharar but did not specifically state what these constitutes ; • “Deficient of clarity (or uncertainty) with regard to the subject matter (“Ma’kud ‘Alaih”) being contracted” ; • “O Believers ! Do not devour one another’s property by unlawful ways : instead do business amongst you by mutual consent”. (An-Nisa, verse 29)

The following are examples involving gharar expressly forbidden by the Prophet : (a) Habal al-habalah – sale of the offspring of a still-to-be born animal ; (b) Musamasah – sale of fruit prior to ripening ; (c) Bai’ munabadha – a sale performed by the vendor throwing a cloth at the buyer and achieving the sale without giving the buyer the opportunity to properly examine the object of sale ; (d) Al-Madhamin wa’ Imalagih – sale of what was in the loins and wombs ; (e) Bai’ Al-hassat – a type of sale where the outcome is determined by the throwing of a stone on the object to be sold ;

Gharar is present in all those business dealings in which “one party does not know what is in store for him at the end of the bargain” ; • Gharar is not just about lack of information regarding the quality or quantity of the subject matter but according to Ibn Rushd, it may originate from : (a) Ignorance and lack of information over the nature and attributes of an object ; (b) Doubt over its availability and existence ; (c) Lack of information concerning the price and terms of payment ; (d) Prospect of delivery ;

According to the “Badan Petugas Khas” Report with regards to gharar in an insurance contact : • “It is clear that the insurance contract as practiced presently give rise to Al-gharar as the “Ma’kud ‘Alaih” is not clear with regards to : (a) Uncertainty as to whether or not the insured will get the compensation which has been promised ; (b) Uncertainty as to how much the insured can get ; (c) Uncertainty as to when the compensation can be paid ;

(ii) Maisir • The word ‘maisir’ literally means ‘getting something too easily’ or ‘getting a profit without working for it’ ; • The Prophet forbade all forms of business in which the monetary gain comes from mere chance or speculation and not from work ; • The prohibition with regards to games of chance is explicit in the following verse : “O Believers ! Intoxicants and gambling and divining arrows are an abomination of satan’s handiworks. Leave it aside in order that you may prosper. Indeed satan intends to sow enmity and hatred among you by means of intoxicants and gambling and to prevent you from the remembrance of Allah and from prayer. Will you not, therefore, abstain from these things? Obey Allah and His Messenger and abstain from these things”. (Al-Maidah 90-92)

Insurance practitioners is of the opinion insurance reduces risk where as gambling increase or create risk ; therefore they are not one of the same ; the notion that the insured lost his premium when claim do not occur is not quite correct ; the premium is in fact has been exchanged for financial security ; to them this should not be considered as ‘wrongful devouring’, it is totally different from the money earned from gambling ; • The elements of gharar and maisir are interrelated ; the presence of gharar could lead to maisir if it is excessive ; there cannot be maisir unless the element of gharar is present ;

(iii) Riba • Literally means ‘increase in’ or ‘addition to’ anything ; • Islam prohibits riba ; • The following Quranic verse : “O you who believe, devour not usury, doubling or quadrupling, the sum lent, Fear Allah and observe your duty to Him ; that you may really prosper”. (Al-Imran, verse 130) • Present day insurance activities involve the element of riba. For example : (a) Investing in interest bearing instruments ; (b) Paying interest on some of their products ; (c) Many insurance contracts contain usury, as it promises to pay more than the premium paid ;

Riba is of two forms : riba al-fadl and riba al-nasiah ; Muslim jurists differ in interpreting riba al-fadl however they are all of the same opinion with regards to riba al- nasiah ; (iv) Roles of Takaful Operator : • As Custodian of Fund ; • acts as manager/ operator of the takaful fund ; • acts as Mudharib ; • As Risks Taker versus Risk Sharing ; • Takaful operator does not own the takaful fund ; they acts as the professional manager ; • All the participants mutually agree to share the risk among them ;

Transparency and Fairness • Sincerity ; • The parties to the contract must have the sincerity not to gain but to be bound by the principles of mutual cooperation, solidarity and brotherhood; • Absolute Shariah Principles ; • Aims and operations do not involve any element which is not approved by the Shariah; • Moral Attributes ; - The parties involved in the contract should observed the principles of utmost of good faith, honesty, disclosure and truthfulness. • Element of Contract. - The parties to the contract must have legal capacities; must have insurable interest; consideration; mutual consent;

TAKAFUL MODELS (a) Mudharabah Model : • A mudarabah contract is a commercial profit sharing contract between the provider or providers of fund for a commercial venture and the entrepreneur. • In a mudarabah model the takaful operator acts as a mudarib and the participant as rabul mal. The takaful operator manages the operations of the fund in return for a share of the surplus. The surplus is shared in a pre-agreed proportion between the operator and the participant. • In a pure mudarabah model, the management expenses and any other direct expenses for management of the fund will be borne solely by the operator from the shareholders fund and its share of the surplus of the underwriting and investment returns.

Under the modified mudarabah model, the management expenses direct or otherwise will be charged to the takaful fund. The surpluses from the fund which is a combination of the underwriting surplus and the investment surplus will be shared between the participants and the operator in the pre-agreed proportion.

(b) Wakalah Model : • In a wakalah model, the takaful operator acts as the agent on behalf of the participants. The operator is paid a pre-agreed management fee for the services rendered in respect of underwriting, management and investment of the fund. The operator does not share in the underwriting surplus. • In underwriting, the takaful operator act as an agent on behalf of the participants to manage the takaful fund. Any liabilities for risks underwritten are borne by the fund and any surplus arising from belongs exclusively to the participants. The operator is not liable for any deficit of the fund. The operator is being paid a management fee termed as wakala fee which is usually a percentage of the contributions paid by the participants. This is normally deducted upfront from the contributions. As for the management of the investment activities of the fund, the operator is also paid a wakala fee based on an agreed percentage.

(c) Waqaf Model : • In a waqaf model, a waqaf fund is established by the shareholders of the takaful company through the contribution of ‘ceding amount’ to compensate the beneficiaries or participant of the takaful scheme. The ceding amount of the waqaf will remain invested. The takaful fund, consisting of the contributions paid as tabarru’, will be further invested by the company based on the principle of Islamic modes of trades. Any person by signing the proposal from contributing to the Waqaf and subscibing to the policy documents shall become the member of the waqaf fund.

CLASSIFICATION OF BUSINESS • In general, the commercial takaful is categorized into two basic types of business namely : (i) Family business; (ii) General business; • In terms of licensing, it varies among the various jurisdictions throughout the world. Some issue license on a composite basis (both family & general) while some others issue on a monocline of business basis. In Malaysia, under Takaful Act 1984, licenses are granted on a composite basis. (a) Family Takaful Plans : • The Family Takaful Plan provides protection and also the platform for savings for members. Various products are designed to provide solutions to the needs and demands of the individuals and the commercial segments.

The following benefits can be by an individual participant in a long-term family takaful plan: • Protection in the form of financial mutual aid to his family members arising from the benefits of the takaful plan should the participant die before the maturing of the takaful plan. • Regular savings for a definitive period with the view of creating retirement fund to be utilized during old age. • Earning investment profits acceptable to Shariah from the contribution to the fund. • Availability of funds to finance children education should be chooses the education plan offered under the Family Takaful business. • Avenue to assist each other through the concept of tabarru’.

Basically a family takaful plan covers death benefit, maturity benefit riders can be incorporated to provide hospitalization benefits, accidental and permanent disability benefits and also critical illness benefits.

For the commercial sector, family takaful offers schemes such as Group Family Plans and Group Family Takaful Hospitalization and Surgical Plans. These are arrangements of cooperation and mutually based on the principles of ta’awun and mudarabah among members of the fund. Group Family Plans are normally taken by the corporate bodies as employers for the benefit of their employees under an employment contract. • Apart from the above, there are various other Family Takaful Plans or products available to the individual or group such as : • Takaful mortgage plans; • Takaful education plans; • Investments Linked plans; • Credit Related Takaful plans;

In general, the Family Takaful comprise of two funds namely the Participants Account (PA) and the Participant special Account (PSA). The PA is meant solely for the purpose of savings and investments, while the PSA is to pay takaful benefits such as death and maturity of the contract. (b) General Takaful Plans : • The General Takaful business is basically a contract of joint guarantee. It is a short-term contract usually covering a period of one year or less. General Takaful contracts are designed to meet the needs for protection in the event of any material loss or damage or bodily injury consequent upon the accident happening of a peril whether it is catastrophic in nature or otherwise inflicted upon properties, material belongings or mankind.

In consideration of agreeing to contribute to the pool, the participants undertake as Tabarru’ these contributions for the purposes of mutual compensation to be made available to any defined loss or damage or sufferings. These contributions are pooled into a fund called general Takaful Fund and it is from this fund that mutual compensation would be paid to any participants suffering from a defined loss. • The takaful operator will act as a mudarib for the fund and will make all the necessary efforts to diligently invest this fund in Shariah approved investment instruments to earn the necessary returns or profits. In order to prudently manage the fund and to protect it from suffering severe financial impact or loss, appropriate re-takaful arrangements are made. The cost of these re-takaful arrangements are charged to this fund apart from the appropriate reserves for unexpired risks, claims and also the incurred but not reported claims (IBNR) which are deducted from this fund.

The fund has to be managed prudently, any outflows must be properly accounted for in order not to result in any deficit. Any surplus from the fund will normally be shared between the participants and the takaful operator depending on the business model it has adopted. Should there be any distribution of surplus, it can only be given to participants at the expiry of their takaful contracts provided they have not received any compensation or incurred any claims during the period of the contract. • The following are the various types of General Takaful Plans : • Motor Takaful Schemes; • Fire Takaful Schemes; • Miscellaneous Accident Schemes; • Marine Takaful Schemes; • Engineering Takaful Schemes; • Aviation Takaful Schemes;

SHARIAH PRINCIPLES (a) Sources of Shariah: • There are four fundamental sources of Shariah : (i) Quran; (ii) Sunnah; (iii) Ijma; (iv) Qiyas; • Apart from the four sources of Shariah that have been agreed upon by Scholars, there are also other sources of namely : (i) Istihsan; (ii) MaslahahMursalah; (iii) Istishab; (iv) Uruf; (v) MazhabSahabi; (vi) Sharun man Qablana;

(b) Legal Maxims : • Apart from the sources of shariah, qawaidfiqhiyah are also used in the discussion of takaful; legal maxims are statements of principles that are derived from the detailed reading of the rules of Islamic Jurisprudence; • There are five fundamental legal maxims which are : (i) “Acts are judged by the intention behind them” (Al-umuru bi-maqasidiha); (ii) “Certainly is not overruled by doubt” (Al-yaqinu la yuzallu bish-shakk); (iii) “Custom is the basis of judgement” (Al-’aadatu muhakkamatun); (iv) “Hardship beget facility” (Al-mashaqqatutujlab at-taysir); (v) “Harm must be eliminated” (Ad-dararuyuzal); The five legal maxims are further broken down into seventeen corollaries.

Some of the more common corollary legal maxims that has been used in the discussion of takaful are : (i) The original legal position of any matter is permissible until there is evidence prohibiting it. (ii) Whatever leads to haram, is in itself haram. (iii) In contracts effect is given to intention and meaning and not to words and phrases. (iv) Difficulty brings ease. (v) The ends do not justify the means. (c) Law of Transactions : • Law of transaction deals with fiqhmuamalat which includes exchange contracts (e.g., sale and purchase), profit sharing contracts (e.g. mudarabah and musharakah), contracts of guarantee, agency contracts and others.

The Sale Contract • The sale contract is the most prevalent form of contract and can be said to form the basis of other contracts. The Quran mentioned and legalised the sale contract the verse “And Allah has permitted trade and prohibited riba” (Al-Baqarah 275). The Sunnah further sactioned and endorsed the sale contract as narrated by Al-Hakim: “The work of a man with the hands and the mabrur sale”. • Tenets of a Sale contract • In order for the sale contract to be accepted by Islamic law, it has to fulfill certain tenets and conditions, which are; (i) The contracting parties; (ii) The objects; (iii) The offer and acceptance;

(d) Principles of Takaful : • The takaful concept is based on the following principles : (i) Mutual Responsibility; (ii) Mutual Help and Cooperation; (iii) Mutual Protection;

TAKAFUL STATUTES (a) Malaysia : • In Malaysia, the takaful operations are governed by the Takaful Act 1984, which contains four parts and sixty eight sections. The four parts are : • Deals with definitions and classification of takaful business; • Deals with conduct of takaful business; • Deals with returns, investigations, winding up and transfer of business; • Deals with miscellaneous and general provisions; • Under the Takaful Act 1984, a takaful operator must be incorporated as a company as defined in the Companies Act 1965 or as a society as registered under the co- operative sociaties.

The Act require the operator to establish a Shariah advisory body which is approved by the Director General, to advise an operator on the operations of its takaful business so as to be shariah complaint. (b) Bahrain : • In Bahrain, the law governing the takaful industry is Legislative Decree No.17 of 1987 with respect to insurance companies and organizations. The Decree Known as “the insurance law of 1987” contains 4 Chapters and 37 Articles. However, the central Bank of Bahrain and Financial Institutions Law 2006, which was passed recently, superseded the Decree . (c) Indonesia : • In Indonesia, the takaful operations are governed by the same laws governing conventional insurance.

(d) Singapore • Like Bahrain and Indonesia, the same law that governs conventional insurance governs the takaful operations in Singapore. i.e., Singapore Insurance Act (SIA). SIA contains 4 Parts with 65 sections.

The following are the statutory bodies entrusted to regulate and supervise the takaful industry in each of the jurisdiction : (i) Malaysia – Central Bank of Malaysia; - Minimum paid up capital in RM100 million; - Takaful Act 1984; - Various guidelines have been issued to regulate the industry in a systematic, orderly manner. (ii) Bahrain – Central Bank of Bahrain; - CBB Rulebook Vol. 3; - ES-1; ES-2; ES-1.19;

(iii) Indonesia – PeraturanPemerintahanNombor 73 Tahun 1992 tentangPenyelenggaraan Usaha Peransurian. - Mininum paid- up is RP50 milliard (iv) Singapore – Monetary Authority of Singapore (MAS); - Minimum paid-up not less than S$25 million; - Set various levels of margins of solvency;

REGULATIONS ISSUED BY GOVERNING BODIES • Governing bodies tasked with the development of the takaful industry issuing fatwas and/or guidelines under the international Islamic organizations are: • OIC Fiqh Academy, • The Islamic Financial Services Board (IFSB) and • The Accounting and Auditing Organization of Islamic Financial Institutions (AAOIFI).

There is also the International Association of Insurance Supervisors (IAIS) formed in 1994 among governing bodies in various countries for non-shariah matters. IAIS is mirrored along the lines of Basel Committee on Banking Supervision (BCBS) which issued Basel Capital Accord and Basel II. • The IAIS was established to promote cooperative among insurance supervisors and liaise with supervisors and regulators on other financial sector. • The IAIS develops principles, standards and guidance on insurance supervision and is active in promoting their implementation, in particular the Insurance Core Principles and Methodology (ICPS) which consist of : • Essential principles that need to be in place for a supervisory system to be effective; • Explanatory notes that set out the rational underlying each principle; • Criteria to facilitate comprehensive and consistent assessments;