Download

1 / 3

30 likes | 37 Views

Tax audit applicability has a legal validation only if submitted by a Chartered Accountant or a firm of Chartered Accountants or a Statutory Auditor. The tax audit report needs to be signed by the accountant or the auditor who has performed the audit. More info visit <br>https://enterslice.com/tax-audit

E N D

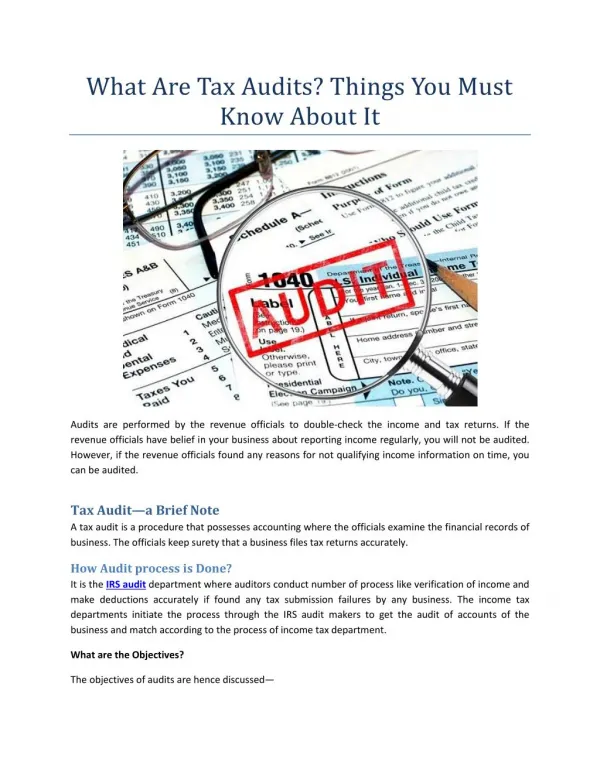

Things to know about the Tax Audit Audit is all about review. Tax audit involves the process of reviewing or examining of the books of accounts of a business entity to confirm the income tax computations, deductions and other such financial calculations have been done in compliance with Income Tax laws of the country. Tax audit enables easy income tax computation as well as Income Tax Return filing easy. The Tax Audit limit is regulated by Section 44D of the Income Tax Act. Person carrying business or in a profession have to be get their books of accounts audited compulsorily under Section 44AB pertaining to certain tax audit applicability. The tax audit applicability categories the following persons who have to undergo the audit process on a mandatory basis:- 1.Persons carrying on business with a turnover or aggregate sales exceeding 1 crore, but have not opted for Presumptive Taxation Scheme. 2.Persons carrying out business with total or aggregate sales or turnover exceeding 2 crore and have opted for the Presumptive Taxation scheme 3.Professionals whose gross receipts exceed Rs. 50 lakh annually The presumptive taxation scheme under Section 44AD mentions that tax audit is not required for persons who are enrolled for the scheme and have a turnover of less than INR 2 crore annually. Purpose of Tax Audit The tax audit process ensures that the books of accounts have been maintained correctly and as per Income Tax provisions. Tax audit brings out discrepancies as pointed out by the tax auditor after a thorough examination of the books. Since the tax audit report follows a prescribed format, it saves time of tax authorities in checking out minute details and correctness of the information as filed in ITR. Tax Audit Report Format The audit report is required to be furnished either through –

1.Form 3CA – this report is applicable for persons carrying out business or profession who need to get their books of accounts mandatorily audited as per the Act. 2.Form 3CB – this form is required to be furnished by persons carrying out business or profession for whom it is not compulsory to get their books audited under the Act. 3.Form 3CE – is applicable for Non-residents and foreign companies that receive any form of payment or fees for technical services or royalty from the Government of India. Tax audit applicability has a legal validation only if submitted by a Chartered Accountant or a firm of Chartered Accountants or a Statutory Auditor. The tax audit report needs to be signed by the accountant or the auditor who has performed the audit. For e-filing the online tax audit form, the report needs to be signed by the accountant or the auditor as well as his membership number needs to be mentioned alongside. The audit report first needs to be submitted to the concerned person or taxpayer digitally to get his approval before the online tax audit is filed electronically. There is a tax audit limit for Chartered Accountants too. They cannot undertake more than 60 tax audits in a year. The penalty for not getting the books of accounts audited for persons who are compulsorily required to get the audit done is 0.5% of the turnover or gross receipts, with a maximum limit of Rs. 1.5 lakh. The penalty is levied under Section 271B of the IT Act. However, the person is given a chance to give reasons for non-compliance, and if found acceptable, no penalty is imposed. The audit report needs to be obtained before or by 30th September of the said assessment year. Only the 3CE report has a due date of 30th November of the said assessment year. More info visit https://enterslice.site123.me/blog/things-to-know- about-the-tax-audit