Download

1 / 46

490 likes | 677 Views

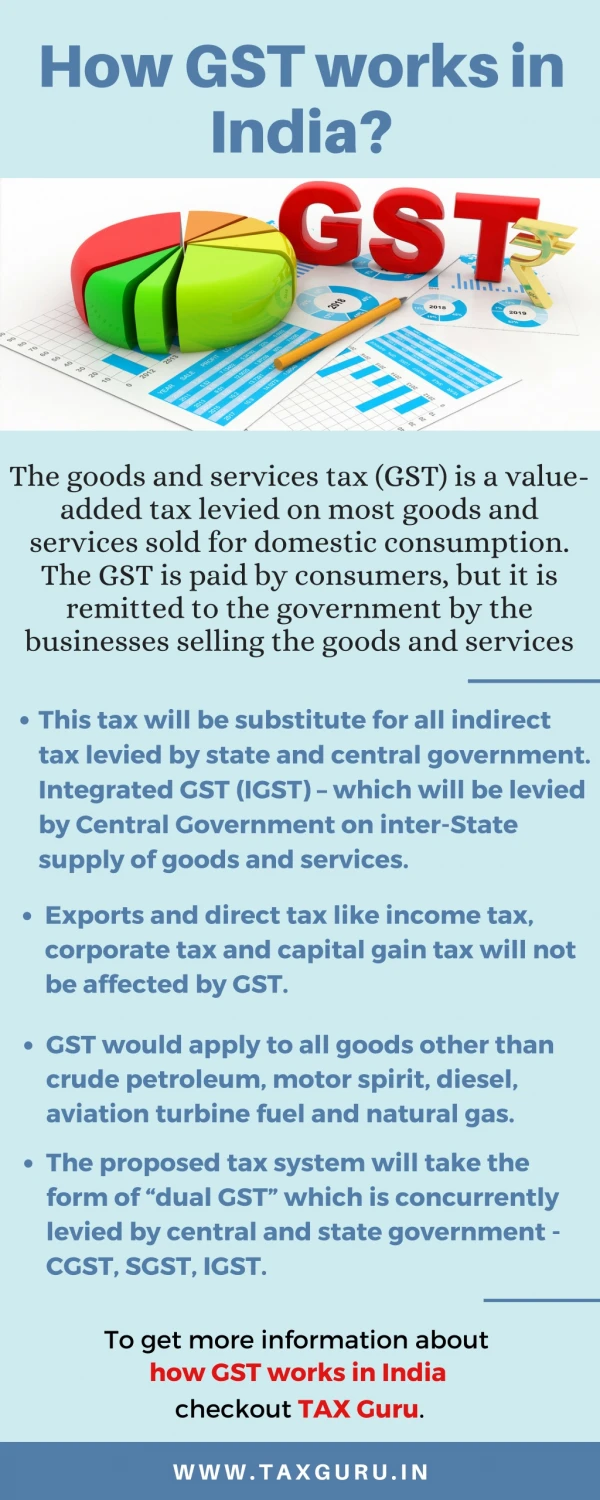

GST (Goods a service tax) is a Pan based comprehensive, multi-stage destination based valued added tax on the manufacture, Sale, and consumption of goods throughout the India. GST replaces all taxes levied by the state and central governments. Goods and Services Tax (GST) is not only the tax reforms in the India, it is going to be business reforms. The government aims to remove all tax barriers between central &states. It aims to create a single market with a mission of one nation one tax.

E N D

GST READY IN INDIA Lets ready for GST from 1stJuly 2017 A Guide to GST by India's Top 25 Consultant Copyright © 2017 Enterslice ITeS Private Limited. Share Alike. Attribution Required.

Taxes in India Taxes in India Indirect Taxes Direct Taxes Center State Income Tax VAT Service Tax REPLACED BY GST Excise Duty Entry Tax CST Octroi Custom Luxury Tax

Multi-Tiered System – GST rate on Goods LuxuryCars,Pan Masala,Tobacco, AeratedDrinks Soaps,Oil Toothpaste, Refrigerator, Smartphone Mass consumption itemslikeSpices andMustardoil, Sugar,tea 28% 18% 5% 0% 50%ofthe consumerprice basket,including Foodgrains,milk, vegitable 12% Processed Food 28% WhiteGoods, Cars

GST Rate on services Consultingservices, mid-hotel, Exhibition,and catering.Composite supplyunderwork contract Alltypeof Transportservices, Taxi/Cab 28% 12% 5% 0% Premiumhoteland otherservices, Airlines,Chitfund, IPR,Royalty/IPR,& Construction 18% Agriculture,Govt., Semigovt,NGOwith 12AACertificate, Emergencyservices, valuehotelwith DailyrentlessRs.1K

Relief for general public GST EXEMPETED LIST GSTCounciltoworkoutexemptedlistofitems Keyfooditems,Exportofservicestobekeptoutoftaxnet ThoseitemsthatdonotfaceVAT/Servicetaxmaybekeptout Someitemsthatdonotattractexcisedutyalsotogotaxfree PROBABELY TAX FREE ITEMS Bread,Milk,Curd,Salt,freshveggiesandfruitstogotaxfree TAX FREE ITEMS Birndi,Sindoor, Prasadsoldattemples GSTEXEMPETLIST Humanbloodcontraceptives,PrimaryHealthcare,Education

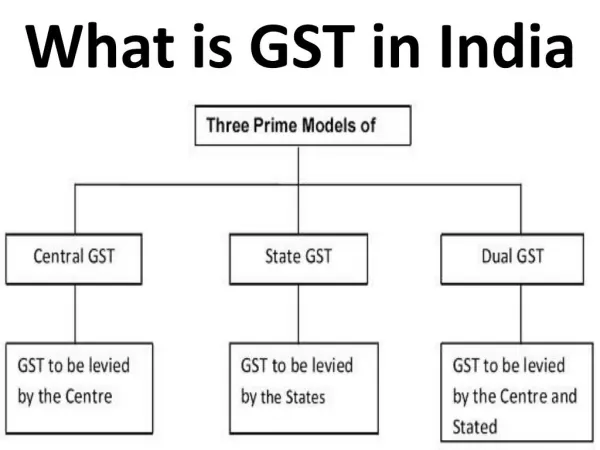

GST Models Three Prime Models Central GST State GST Dual GST GSTtobelevied bytheCentre GSTtobelevied bytheStates GSTtobeleviedbythe CentreandStated

New Tax Heading under GST - Central State Tax - VAT/Sales Tax §- Central Excise - Entry Tax §- Service Tax - Tax on Lottery etc CGST SGST IGST §- SAD - Surcharge and Cess §- CVD - Purchase Tax §- AED - Entertainment Tax - Luxury Tax §- Surcharge and Cess

System of Levying GST Goods/Services produced and consumed in same State Inter-state consumption of Goods/Services Exported Goods/Services Imported Goods/Services Present Indirect Taxes GST Type Excise Duty Service Tax Central GST Customs Duties Central Sales Tax CGST + SGST Rate levied In targeted GST levied (Now dropped) GST not applicable (Cannot export taxes) CGST +SGST Rate Ievied State Sales Tax Entertainment Tax State GST State VAT Professional Tax

GST Rules 1. Accounts & Records Rules [3 Rules] 8. Transitional Provisions Rules [4 Rules] 2. Advance Ruling [5 Rules] 9. Input Tax Credit Rules [10 Rules] 3. Appeals and Revision [8 Rules] 10. Tax Invoice, Credit & Debit Notes Rules [8 Rules] 4. Assessment and Audit [5 Rules] 11. Payment of Tax Rules [4 Rules] 5. Electronic Way Bill [5 Rules] 12. Refund Rules [8 Rules] 6. Composition Rules [5 Rules] 13. Registration Rules [18 Rules] 7. Determination of Value of Supply Rules [8 Rules] 14. Returns Rules [25 Rules]

GST Transitional credits 1. Taxpayer will credit against stock as on 30/06/17 2. Need to submit declaration by 30/09/17 3. For intra-state sale of goods which is non-excisable goods-ITC under GST shall be allowed Max 60% of GST Rate 4. For inter- state sale of goods which is non-excisable goods-ITC under GST shall be allowed max 30% of GST Rate 5. Credit on opening stock shall be only allowed if goods lying as on 30/06/17 is sold with 180 days. 6. Any receipt of VAT & Excisable goods in the month of july-17, full ITC under GST shall be allowed 7. In Case Taxpayer will return the goods within 180 days from the date of purchase, he will get 100% ITC under new rule subject certain restriction under the GST laws.

Registration Number ü ThetaxpayerwillbeallottedaStatewisePANbased15digitGoods and/orServicesTaxpayeruniqueIdentificationNumber(GSTIN). ü ThedigitsintheGSTINwilldenotethefollowing State Code PAN Entity Code Blank Check Digit 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Multiple Registrations within the same State ü TheGSTmodellawsallowsmultipleregistrationswithinoneStatefor differentbusinessverticalslikeGarmentandfoodbusinessinonestate. Fewconditionhavebeenimposed- ü ITCacrossthebusinessverticalsofsuchtaxablepersonsshallnotbe allowedunlessthegoodsand/orservicesareactuallysuppliedacrossthe verticals. ü Fortherecoveryofdues,allbusinessverticalswithonePAN,though separatelyregistered,willbeconsideredasasinglelegalentity.

ChecklisttomakeyourbusinessGSTready ü Define your Goods / Services in HSN / SAC and fix GST rate in your billing system ü Understand your business process in GST scenario and classify which Business transactions are goods and services ü ClassifyyourBusinesstransactionsundergoodsandservices,andplaceof provisions ü NeedtoDefinethechangeinbusinessinstagesofpre,duringandpost manufacturingprocess,Definelogisticmodel,BranchandWarehouse ü Re-defineyoursalespolicy,amendcontracts,Returntermsanddiscount policy. ü NeedReviewyourVendorsnatureofgoods,placeofsupply,contractual terms&ObtainGSTINNowithHSN/SACforeachproductitem ü PricingStrategywithproductandservices

Intra State - Invoice Invoice– IntraState– UnderPresentLaw Particulars ValueofSupplyofGoods Add:Excise(say)@15% SubTotal Add:VAT(say)@15%[Caution:CascadingEffect] Total Amount 200,000 30,000 2,30,000 34,500 2,64,500 Invoice– IntraState– underGSTLaw Particulars ValueofSupplyofGoods Add:CGST(say)@15% Add:SGST(say)@15% Total Amount 2,00,000 15,000 15,000 2,60,000

Intra State - Invoice Invoice–InterState– underGSTLaw Particulars Amount ValueofSupplyofGoods 200,000 Add:IGST(say)@28% 56,000 Total 260,000 Invoice– IntraState– UnderPresentLaw Particulars Amount ValueofSupplyofServices 100,000 Add:SGST(say)@18% 18,000 Total 118,000

Intra State - Invoice Invoice– IntraState– underGSTLaw Particulars Amount ValueofSupplyofServices Add:CGST(say)@8% Add:SGST(say)@7% Total Invoice– InterState– underGSTLaw Particulars ValueofSupplyofServices Add:IGST(say)@15% Total 100,000 7,000 7,000 115,000 Amount 100,000 15,000 115,000

Exemption Limit for Small Scale Business under Goods and Service Tax (GST) TheGoods&ServicesTax(GST)Councilhasdecidedthatbusinessesinthe North-easternandhillstateswithannualturnoverbelowRs.10lakhwould beoutoftheGSTnet,whilethethresholdfortheexemptionintherestof IndiawouldbeanannualturnoverofRs.20lakh.

Good and Services Tax Network (GSTN) AGSTCouncilhasbeenformedbytheFinanceministryinordertoestablishcommonfilingplatformfor th community ThecompanywasincorporatedonMarch28, 2013asanon-government,privatelimited company Itwillhaveaself-sustainingrevenuemodel, whereGSTNwillbeabletolevyusercharges ontaxpayersandtaxauthoritiesforavailingits services Itisanexclusivenationalagencyresponsible fordeliveringintegratedindirecttax-related servicesinvolvingmultipletaxauthorities

Composition Levy GST - Goods and Service Tax - 1% to 3% without ITC for turnover less than 75Lac in FY

Composition scheme under GST Act • Reduced Tax Liability ( 1% to 5% ) • Reduced Compliances ( only 4 return in a year instead 37 in normal scheme • Increases Liquidity – Need to pay taxes on quarterly basis • No Input Tax Credit • No Tax Invoices • High Penalty • Only Intra-state trading • Not for E-commerce / App driven business operator • Turnover limit In Financial year Rs. 75 Lac • Claim of TDS is allowed

Good and Services Tax Network (GSTN) WHAT STATES NEED TO DEVELOP/MODIFY WHAT GSTN NEEDS TO BUILD GSTN SHAREHOLDING State Govt Along with empowered group of state finance ministry Registration Assessment 24.5% 24.5% Union Govt ReturnFiling Refund NSG Strategic Investment Corporation 10% TaxPayment Recovery HDFC Bank 10% IGSTSettlement Appeal 10% HDFC M IS/81/Dashboards Investigation 10% ICICI Bank DealerInformation&Ledger Survey/Enforcement 10% LIC Housing Finance Helpdesk/CallCentre MIS/Analytics

GST Tax Ledger (e-Tax Liability Ledger | e-Credit ledger) e-Tax Liability Lager As all we Know Form 26AS in TDS Credit, which shows the tax credit statement of the Assesse in pan login ; in same in the proposed GST regime, e-Tax Ledger is prescribed to contain information on tax credit received from counter party GST and tax liabilitybasedonreturnsfilledbythetaxableperson E-Cash Ledger Tax InGSTregime,the"Deposit"ofthetax,interest&penalty canbemadebythefollowingmodes Tax Netbanking Credit/DebitCard NEFTNationalElectronicsfundtransfer RTGSRealTimeGrossSettlement

The Electronic Cash Ledger Depositof Interest,Tax,Penalty,Feeoranyotheramount byataxablepersoncan be madebythe followingmodes: a. InternetBanking b. Credit/DebitCards c. NationalElectronicFundsTransfer- NEFT d. RealTime GrossSettlement– RTGS e. Anyothermodeas may be prescribed– (Challanpayment inBanks)

GST Tax Ledger (e-Tax Liability Ledger | e-Credit ledger) E-Liability Ledger E-Credit Ledger Thisledgerisrequiredtobe maintainedelectronicallyforallGST Liabilitiesviz: InputTaxCredit(ITC)onpurchases shallbecreditedtoe-CreditLegeras perGSTreturnfiledbythecounter party.Thee-CreditLedgerincludes: - Liabilitybasedonself-assessmentof GSTreturnsby10thand15thofthe Month - ITConinwardpurchasesfrom RegisteredTaxPayers ITConclosingstockason30stJune 2017 - - AnyInformofLiabilityoutofdemand noticeforGSTauthorities - Creditutilizedagainsttheavailable amountsinthee-cashledgerore- creditleger

FAQs CPIN stands for Common portal Identification Number(CPIN) given at the time of generation of GST challan. It is a I4 digit unique number to identify the challan.CPINvalid only for I5 days. CIN stands for ChallanIdentification Number. It is a I7 digit number that is I4-digit CPIN plus 3-digit Bank COde. CIN is generated by the authorized bank/Reserve Bank of India (RBI) when payment is actually recieved by such authorized bank or RBI and credited in the relevant government account held with them. It is an indication that the payment has beenrealized and creditedto the appropriate government account. CIN is communicated by the authorized bank to taxpayer as well as toGSTN. • E-Cash Ledger, E-Credit Ledger and E-Liability Ledger featuresof proposedGSTregime. are unique • The taxcredit system predicted to be updated on real-time basis in GST Network. entire tax payment and Form-26AS income figures is now universally accepted by statutory authorities. Similarly, in the days to come GST E-Leedger reconciliation with Forms 26AS will be the prima-facie exercise for all compliances. reconciliation with E-FPB stands for Electronic Focal Point Branch. These are branches of authorized bank which are authorized to collect payment of GST. Each authorized bank will nominate only one branch as its E-FPB will have to open accounts under each major head for all governments. Total38 accounts(one each for CGST, IGST and one each for SGST for each State/UT Govt.)will have to be opened. Any amount received by suchE- FPB towards GST will be credited to the appropriate account held by such E-FPB.For NEFT/RTGS Transactions,RBIwill actas E-FPB. Assessees and •

GST Return Filling Forms in from GSTR-1 to 8

GST Returns (GSTTaxpayer@NormalRates) GSTR 1 Outward Supply 10th of Next Month GSTR 2 Inward Supply 15th of Next Month 37 GSTR 3 Monthly Return 20th of Next Month GSTR 8 Annual Return 31st Dec of Next FY

GST Returns (GSTTaxpayer@CompoundingRates) GSTR 4 Quarterly Return 18th of Next Month to Quarterly 5 GSTR 8 Inward Supply 31st Dec of Next FY

Utilization of ITC & Cross Utilization InputTax OutputTax(IntheorderofPreference) IGST CGST SGST IGST CGST CGST IGST SGST IGST SGST

Compliance Rating 04 01 EverypersonliabletopayGSTshall beratedandwillbeassignedaGST complianceratingscore The methodologywouldbeprescribed details of parameter & The compliance rating score will be updated periodically intimated as follows: - To the taxable person - Will be placed in the public domain and will be The rating would be based on his compliance with the provisions of CGST,SGST &IGST 03 02

Registration Eligibility The following persons shall have to register irrespective of the turnover • • • • • • • • • • Personmakinganyinter-statetaxablesupply(i.e.sellingoutsidethestate) CasualTaxableperson PersonwhorequiredtopayunderReverseCharge Non-residenttaxableperson Apersonrequiredtodeducttax(e.g.e-commercebusiness– marketplace). Thepersonsupplyinggoodsorservicesorbothasanagentofanyotherperson. InputServiceDistributor Apersonwhosuppliesgoodsorservicesthroughe-commerce. Everye-commerceoperator Anaggregatorwhosuppliesservicesunderhisbrandname

Anti-Profiteering measure ü In order to prevent any rise in price of commodities after goods and service tax (GST) implementation, the Centre has proposed an ‘anti-profiteering’ measure to ensure that trade and industrypass the benefitsofreductionintax rates toconsumers. ü As per Model GST Law, the central government will constitute an authority or entrust the task to an existing authority to examine that the input tax credits or reduction in tax rates are passed byregistered tax payersto consumers. ü Tax evasionup to Rs 2 crore a bailableoffence

Pricing Analysis Under GST most of the indirect taxes are subsumed ü IGST:ITCshallbeseamlesslyavailableandhencesometaxeslikeentrytax,LBT,CST,etc., whichwerehithertocostsshallbeeliminated ü ITCReversal:EvencertaincreditreversalscurrentlyprevalentunderstateVATwillbe removed andthuscosttothatextentwillgodown ü PriceChange:WhenGSTcomesinforce;Pricerevisioncannotbedoneallofasudden

GST Training Alltheemployeesoftheorganizationshall undergoextensivetraininginGSTsothat itsimplicationsaswellasdocumentation canbewellunderstoodandtakencareof Trainingshouldencompassallthe facetsoftheGSTsothatempowered employeescantakeappropriateand correctdecisionswiththehelpof professionalswhentheyfaceanychallenge

GST Training Alltheemployeesoftheorganizationshall undergoextensivetraininginGSTsothat itsimplicationsaswellasdocumentation canbewellunderstoodandtakencareof Trainingshouldencompassallthe facetsoftheGSTsothatempowered employeescantakeappropriateand correctdecisionswiththehelpof professionalswhentheyfaceanychallenge

Transition Issues ü MigrationofexistingtaxpayerstoGST ü AmountofCENVATCreditcarriedforwardina returntobeallowedasITC ü UnveiledCENVATcreditonCapitalGoods ü PendingRefundClaims ü CreditonStock ü SwitchingfromregulartoComposition scheme ü Anymanymore

GST Council Recommendation a) The taxes, all type of cessand surcharges to be subsumed under GST; b) The goods and services that may be subjected to or exempted from the GST; c) The date from which the specified petroleum products would be subject to GST; d) Model GST laws, principles of levy, apportionment of IGST and the principles that govern the place of supply; e) The threshold limit of turnover below which the goods and services may be exempted from GST; f) The rates including floor rates with bands of GST; g) Any special rate or rates for a specified period to raise additional resources during any natural calamity or disaster; and h) Special provision with respect to the North-East States, J&K, Himachal Pradesh and Uttarkhand

VOTING STRENGTH GST COUNCIL Chairperson UNION FINANCE MINISTER Centre 1/3 VOTE IN COUNCIL Other Member from Centre MINISTER OF STATE FOR FINANCE States 2/3 WEIGHT IN COUNCEL Vice-chairperson ONE OF THE STATE FINANCE MINISTERS Members DECISION NEEDS 75% VOTE SUPPORT STSTE FINANCE MINISTERS

Job Work ü Section43A ü RegisteredTaxablePersontoJobWorker(NoGST) ü JobWorkertogetregistered ü Turnoverwillbeincludedinprincipal(goodssupplied) ü JobWorkertoCustomer(possible) ü ITC– section16A ü 1year/3years(ifnotreceivedback/billedthentheITCamounthastobepaidalong withinterest) ü ExemptedGoods/Non-TaxableGoods(JWprovisionnotapplicable)

E-Commerce E-CommerceOperator E-CommerceAggregator E Registration of GST Tax Collectionat Source (TCS) Matchingin E-Commercetransactions Discrepancy will be communicated E-return

ImpactAnalysis ImpactAnalysiswithrespecttoRateofTaxmustbedonewhentheratesarefinalizedby GSTCouncil(ThisisimportantbecausetherateoftaxesunderGSTwillbedifferentis boundtobedifferentfromtheexistingratesandhenceitshallhavetremendousimpacton thepricesoftheproductorservices) ü GSTshallhaveatransformationalimpactontheIndustry(AsGSTisleviedonSupplyas opposedtoExcisewhichisleviedonmanufactureandVATwhichisleviedonSales,it fundamentallyaltersthewayofdoingbusiness) ü GSTshallmakeIndiaacommonmarket,thusdecisionslikesettingupwarehousesand supplychainmanagementshallberevisited;evendecisionofsettingupnewunitsshall considertheimpactofGST

GST – The Conclusion ü ThetargetdateforintroductionofGSTis1stJULY2017. ü Introductionofthistransformationaltaxreformisexpectedtobroadenthetaxbase, increasetaxcomplianceandreduceeconomicdistortionscausedbyinter-State variationsintaxes. ü GSTwillboosteconomicactivityandwillbenefiteveryone. ü Itwillstreamlinethetaxadministration,avoidharassmentofthebusinessandresult inhigherrevenuecollectionfortheCentreandStates. ü Compliancecostsfortheindustrywillgodown. ü Lastbutnottheleast,itwillcreatemorejobs. ü Insum,itwouldbeawin-winsituationforeveryonei.e.taxpayers,governments, consumers,etc.

Looking for GST implementation advisory or confuse about GST ? Enterslice has helped entrepreneurs like you. Write us at: info@enterslice.com

GST – The Conclusion ü ThetargetdateforintroductionofGSTis1stJULY2017. ü Introductionofthistransformationaltaxreformisexpectedtobroadenthetaxbase, increasetaxcomplianceandreduceeconomicdistortionscausedbyinter-State variationsintaxes. ü GSTwillboosteconomicactivityandwillbenefiteveryone. ü Itwillstreamlinethetaxadministration,avoidharassmentofthebusinessandresult inhigherrevenuecollectionfortheCentreandStates. ü Compliancecostsfortheindustrywillgodown. ü Lastbutnottheleast,itwillcreatemorejobs. ü Insum,itwouldbeawin-winsituationforeveryonei.e.taxpayers,governments, consumers,etc.

What is Enterslice Role in GST ü Business model and process definition so that your business will be GST Compliant ü Effectivenavigationthroughtransitionalandcutoffissueslikepre-GSTcreditand pre-GSTstockofgoods ü Reviewofoftaxcompliancesoftware,Businesscontracts,taxmanuals,statutory recordstemplates,calendarsofthecomplianceandtrainingofyourFinanceteam ü DiscussionwithSeniormanagementonexecutionofGST ü GSTimpactAnalysisandtherouteforfutureforspecifiedgroupslikesales,supply chain,ITC,e.t.c.andlocationslikeheadoffice,depotsandfactory,etc.

GST Implementation GET FREE CONSULTANCY Helpline: +91 9069142028 Email: info@enterslice.com Website: www.enterslice.com