Download

1 / 57

570 likes | 671 Views

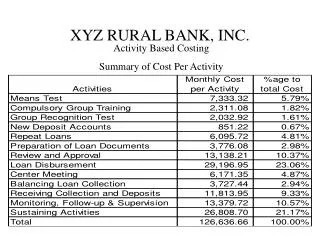

AGROBANCO, RURAL DEVELOPMENT BANK. Contents. - Strategic Planning - Participation and Portfolio Growth - Term of Placements - Growth of our Clients - Portfolio Quality - Potential Demand - National Coverage - Financial Products - Major Crops Financed - Financial Results - ANNEXES

E N D

Contents - Strategic Planning - Participation and Portfolio Growth - Term of Placements - Growth of our Clients - Portfolio Quality - Potential Demand - National Coverage - Financial Products - Major Crops Financed - Financial Results - ANNEXES - Human Resources and Business Managers - Other Services - Other Variables

SectionOne StrategicPlanning

Key Indicators WHAT ARE OUR ASPIRATIONS? ¨IN LINE WITH AGRICULTURE¨ STRATEGIC OBJECTIVE: ¨CAPITALIZATION OF THE AGRICULTURAL SECTOR¨ FacilitateSustainableIncomeGeneration Rural Development Bank

Vision “To be an innovative Rural Development Bank with mixed shareholders, and a leader in financial services, supported by a high human performance and the use of state-of-the-art technology.”

Mission “To provide financial products and services in promotion of rural savings and accompany the development of production, agricultural businesses and complementary activities in the rural areas, focused on the financial inclusion of people in poverty and/or other limitations.”

SectionTwo Participation and Portfolio Growth

Credits to the Agricultural Sector Source: SBS 2013 2,260,973 agriculturalunits (IV CENAGRO)

Créditos al Sector Agrario Source: SBS 2013

Distribution of Placements (in thousands of US$) +20% +20% +17% +16% +13% +16% Agriculture Industry Trade Logistics Other sectors Real estate The inter-annual growth of the placement balance in the agriculture sector was 21%, above other sectors

Projected Placements Projection

Evalution of Disbursements + 94% Year 2011 Year 2012 Year 2013 Year 2014

SectionThree Term of Placements

Distribution Portfolio Term IN MILLIONS OF US$ Year 2012 Year 2013 Year 2014 Short term Long term Medium term

SectionFour Growth of ourClients

New and Recurring Clients 23,887 32,867 87,908 62,534 Jan-2014 New clients Recurring clients

SectionFive Portfolio Quality

Re-financed Portfolio Million $.

High-risk Portfolio Million $.

High-risk Portfolio / Provisions Million $ A January 2014

SectionSix PotentialDemand

Potential Market • Productive Sub-Sectors • Total : 2,260 M Farming Units • Agricultural 321 M • Livestock 416 M • Forestry 4 M • Agricultural, livestock 1,169 M • Agricultural, forestry 15 M • Agric., livestock and forestry 333 M • Property and condition • Irrigation and basins • Energy supply • Altitudinal tiers • Wealth and Conditions • Total 38.7 M of ha • Agricultural 7.1M Ha • Livestock 18.0M Ha • Forestry 13.5 M Ha • Business Chain • Total : 7.1 M of ha • 1. Agricultural Surface in Use : 4.10M • - Self-consumption 0.70 M • Agroindustry 0.96 M • For sale 2.40 M • 2. Agricultural Surface in Development: 3.00 M Source IV CENAGRO 2012

Number of points of sale (Dec. 13) AGROBANCO Potential Market Number of points of sale (Dec. 13) FinancialSystem 111 15 458 17 113 10 507 10 385 18 Source: National Agricultural Sector 2012 – INEI; SBS (2012)

SectionSeven NationalCoverage

National Coverage AGROBANCO Cities with greater restrictions Source: AGROBANCO (2014), INEI (20112

SectionEight FinancialProducts

Financial Services Investment capital products Working capital products Relationto rural areas

Disbursement by Credit Product En Millones de $. 200 A December 2013

SectionNine MajorCropsFinanced

Main Crops 63% de la Cartera

List of Disbursements MAIN CROPS

Section Ten FinancialResults

AGROBANCO Results Net Profit (thousands of US$/.) Income tax thousands of US$/.)

International Rating INVESTMENT GRADE

AGROBANCO Funding Own resources 42% Owed COFIDE 24% Owed IFI’s , BN, Citi 34% FUND MINAG (100%) 1st Floor $. 306.2 MM (98.0%) 2nd Floor $. 6.9 MM (2.0%) 1st Floor $. 66,9 MM (17.6%) Source: AGROBANCO, JAN-14 A total of $.359.6 MM of placements in the Agricultural Sector

Section Eleven ANNEXES

Section Eleven HumanResources and Business Managers

Business Managers TYPE OF PERSON

Business Managers GENDER

Section Eleven OtherServices

IIInternational Seminar on Rural Financial Services BREAKING PARADIGMS • Held on November 11 • Speakers: Peruvian and international professionals will share their experience in rural financial services for the agricultural sector. http://www.agrobanco.com.pe/index.php?id=ii-seminario-internacional&lang=es Objectives of the Seminar: • Contributing to a better understanding of the rural agricultural sector. • Promoting growth and development of a bank industry for the agricultural sector. • Placing financial services as factors for social inclusion, growth and development of the banking industry in the sector.