Download

1 / 18

190 likes | 554 Views

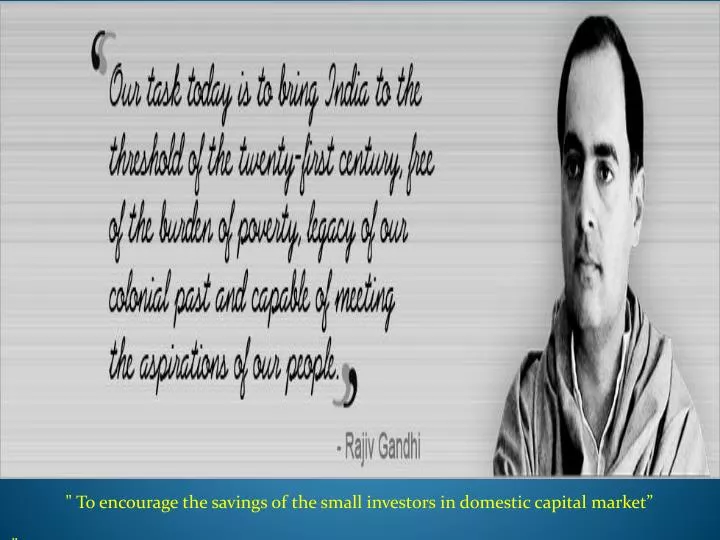

Rajiv Gandhi Equity Savings Scheme or RGESS is a new equity tax advantage savings scheme for equity investors in India, with the stated objective of "encouraging the savings of the small investors in the domestic capital markets." It was approved by The Union Finance Minister, Shri. P. Chidambaram on September 21, 2012.

E N D

" To encourage the savings of the small investors in domestic capital market” "

RGESS • Rajiv Gandhi Equity Savings Scheme or RGESS is a new equity tax advantage savings scheme for equity investors in India. • Rajiv Gandhi Equity Savings Scheme (RGESS) announced in Union Budget 2012-13 is a new equity tax advantage savings scheme for equity investors in India. • The scheme got it's approval on September 21, 2012. It is exclusively for the first time retail investors in securities market.

The Scheme not only encourages the flow of savings and improves the depth of domestic capital markets, but also aims to promote an 'equity culture' in India. • This is also expected to widen the retail investor base in the Indian securities market. • Basically its one of the best investment in tax saving in India.

Example… • Let us say, you invest Rs.50,000 under RGESS. • The amount eligible for tax deduction from your income will be Rs.25,000. • Let us say, you invest Rs.40,000 under RGESS. • The amount eligible for tax deduction will be Rs.20,000. • So you may save about Rs.2,575, Rs.5,150 for income tax slabs 10% and 20% respectively under this scheme.

Latest Updates… • Effective 1 April 2014, investors with a gross total income of up to Rs.12 Lakhs can invest in RGESS, up from an earlier income limit of Rs.10 Lakhs. • Investors can park funds in MFs and listed shares and extended tax benefits to three successive years.

How the scheme works • The RGESS is only for individuals who have not invested directly in • Equities. • including shares . • Derivatives, * Before 23 November 2012. If you hold units in an equity mutual fund, you are eligible to invest in it under the present rules.

Continuation… • If you have a demat account. • But have not used it for transactions before the specified date, • you can avail of the RGESS benefits. Besides, only those whose gross annual income is up to Rs 12 Lakhs can invest.

Eligibility Demat Account Not Opened Resident Individual Annual Income < =Rs. 10 Lakhs No transactions in Equity or F&O 2nd & 3rd holder of an account can open a new account as 1st holder New Retail Investor Resident Individual Annual Income < =Rs. 10 Lakhs Demat Account already Opened No transactions in Equity or F&O

Benefits • The investor would get 50% deduction of the amount invested during the year, up to a maximum investment of Rs.50,000 per financial year, from his/her taxable income for that year, for three consecutive assessment years. • It provides additional tax benefits over and above the present tax savings schemes under the Income Tax Act. • Gains, arising of investments in RGESS, can be realized after a year. This is in contrast to all other tax saving instruments.

Continuation… • The benefits can be availed for three consecutive years. • Dividend payments are tax free. • This scheme has a long run benefit of educating the retail investment segment and thereby moving towards financial inclusivity in the country.

Continuation… • Investments are allowed to be made in instalments in the year in which the tax claims are filed. • Success of this scheme can lead to transfer of assets from traditional savings instruments such as bank deposits • FDs to the capital markets, leading to diversification in retail investor portfolio and also leading to more productive "capital formation" assets.

Eligible Securities • Equity Shares in BSE-100 or CNX 100 • Equity Shares of Maharatna, Navratna, Miniratna • Units of eligible ETFs or MFs • Eligible FPOs & NFOs • IPOs of eligible PSUs

Flexible lock-in period • The RGESS investment has a lock-in period of three years. However, there is flexibility after the first year of investment. • This means that during the first year of lock-in period, the investor cannot sell the holdings for which he claims tax benefit. • From the second year onwards, he can sell a portion of his holdings, provided he maintains the aggregate value in his account for which benefit is claimed for the next two years.

For instance, if your initial investment of Rs 50,000 rises to Rs 60,000 after the end of first year of the lock-in period, you can sell Rs 10,000 worth of securities and maintain Rs 50,000 in the account for the next two years. • However, if the value declines to Rs 40,000, you are not required to make up the balance. However, if you choose to sell a part of your holdings from Rs 40,000, you will need to replenish it.

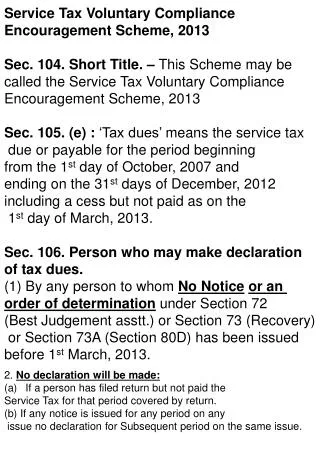

May you think your investment in the right way • Ekarup • CoimbatorePH:9894447881 • ekarupcbe@gmail.com • Chennai PH:9894447882 • ekarupchennai@gmail.com • Madurai PH:9894447883 • ekarupmadurai@gmail.com • Pondicherry PH:9894447884 • ekaruppondy@gmail.com For more information visit us on the web: www.ekarup.com www.zerobrokerageunlimitedtrading.com