Download

1 / 20

200 likes | 377 Views

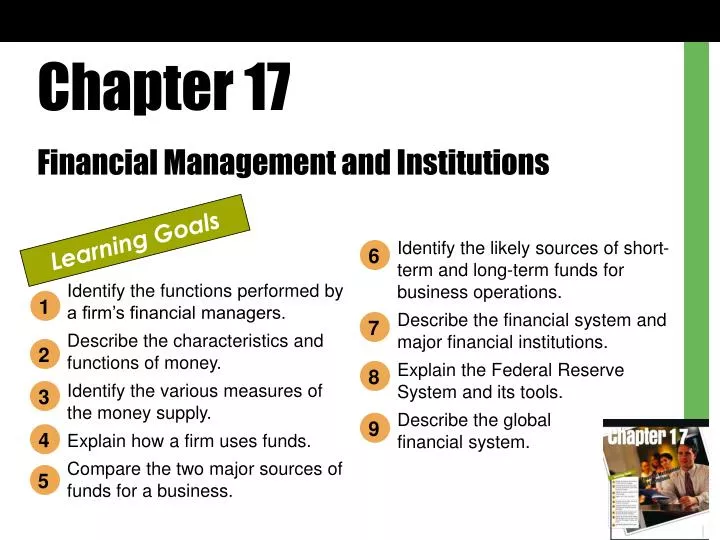

Chapter 17 Financial Management and Institutions. Learning Goals. Identify the likely sources of short-term and long-term funds for business operations. Describe the financial system and major financial institutions. Explain the Federal Reserve System and its tools.

E N D

Chapter 17 Financial Management and Institutions Learning Goals Identify the likely sources of short-term and long-term funds for business operations. Describe the financial system and major financial institutions. Explain the Federal Reserve System and its tools. Describe the global financial system. 6 Identify the functions performed by a firm’s financial managers. Describe the characteristics and functions of money. Identify the various measures of the money supply. Explain how a firm uses funds. Compare the two major sources of funds for a business. 1 7 2 8 3 9 4 5

Finance Business function of planning, obtaining, and managing a company’s funds in order to accomplish its objectives effectively and efficiently. • THE ROLE OF THE FINANCIAL MANAGER • Financial manager Executive who develops and implements the firm’s financial plan and determines the most appropriate sources and uses of funds. • • Chief financial officer Head of an organization’s finance operation. • • Reports directly to CEO or COO. • • Often a member of the board of directors.

• Three executives typically report to the CFO: • • Vice president for financial management or planning • • Treasurer • • Controller • Risk-return trade-off Optimal balance between the expected payoff from an investment and the investment’s risk. • The Financial Plan • Financial plan Document that specifies the funds a firm will need for a period of time, the timing of inflows and outflows, and the most appropriate sources and uses of funds. • • What funds will the firm require during the appropriate period of operations? • • How will it obtain the necessary funds? • • When will it need more funds?

CHARACTERISTICS AND FUNCTIONS OF MONEY • Characteristics of Money • Money Anything generally accepted as payment for goods and services. • • To be efficient, money must have certain characteristics: • • Divisibility • • Portability • • Durability • • Difficulty in counterfeiting • • Stability

THE MONEY SUPPLY • • M1 Total value of coins, currency, traveler’s checks, bank checking account balances, and the balances in other demand deposit accounts. • • M2 Financial assets that are almost as liquid as cash but do not serve directly as a medium of exchange. • • Examples: various savings accounts, certificates of deposit, and money market mutual funds. • • Use of credit cards growing rapidly. • • Amount of outstanding credit card debt has risen by more than 400 percent in the last 20 years.

WHY ORGANIZATIONS NEED FUNDS • • Run day-to-day operations, compensate employees and hire new ones, may for inventory, make interest payments on loans, pay dividends to shareholders, purchase property, facilities, and equipment. • • Use financial planning process to determine how to address shortfalls and surpluses. • Generating Funds from Excess Cash • • Most excess cash balances are invested in marketable securities. • • Most popular marketable securities: • • U.S. Treasury bills • • Commercial paper • • Repurchase agreements • • Certificates of deposit

SOURCES OF FUNDS • Debt capital Funds obtained through borrowing. • Equity capital Funds provided by the firm’s owners when they reinvest earnings, make additional contributions, or issue stock to investors. • • Even established firms may not generate sufficient funds to cover all of the costs of expansion or a significant equipment upgrade.

Short-Term Sources of Funds • 1 Trade credit extended by suppliers when a firm receives goods or services, agreeing to pay for them at a later date. • 2 Short-term loans from commercial banks and other sources. • 3 Commercial paper, which has interest rates typically 1 or 2 percent lower than short-term bank loans. • Long-Term Sources of Funds • • Loans, bonds, and equity financing. • • Public Sale of Stocks and Bonds • • Private Placements • • Venture Capitalists • Leverage Technique of increasing the rate of return on an investment by financing it with borrowed funds.

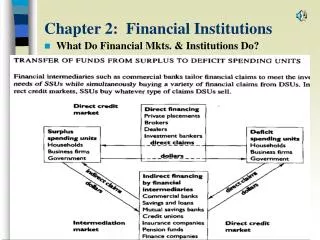

FINANCIAL SYSTEMS AND FINANCIAL INSTITUTIONS • Financial system System by which funds are transferred from savers to users.

• In U.S., households are generally net savers while businesses and governments are net users. • • Because of financial institutions, savers earn more, and users pay less. • Depository institutions Financial institutions that accept deposits that can be converted into cash on demand. • • Nondepository institutions include life insurance companies, pension funds, and the various government- sponsored financial institutions such as Fannie Mae and Freddie Mac.

Commercial Banks • • Offer a wide range of checking and savings deposit accounts, consumer loans, credit cards, home mortgage loans, business loans, and trust services. • How Banks Operate • • Raise funds by offering checking and savings deposits to customers. • • Then pool these funds and offer consumer and business loans. • Electronic Banking • • Electronic funds transfer systems (EFTSs) Computerized systems for conducting financial transactions over electronic links. • Online Banking • • More than one-third of American households use some form of online banking. • • Allows customers to make transactions at any hour on any day.

Bank Regulation • • Among the nation’s most heavily regulated businesses. • Who Regulates Banks? • • Most are state chartered. • • State banks that are federally insured are subject to Federal Deposit Insurance Corporation regulation. • Federal Deposit Insurance • • Insures deposits of up to $100,000 per depositor. • • Shifts risk of bank failure from depositor to FDIC. • Recent Changes in Banking Laws • • Congress revised Depression-era laws to allow banks to enter securities and insurance businesses. • • Also allowed financial services firms to offer banking services.

Savings Banks and Credit Unions • • In U.S., 1,300 savings banks with $1.7 trillion in assets. • • Credit unions are cooperative financial institutions owned by their members. • • 85 million Americans belong to one of the U.S.’s 9,200 credit unions. • Nondepository Financial Institutions • Insurance Companies • • Underwriting The process insurance companies use to determine whom to insure and what to charge. • Pension Funds • • Provide retirement benefits to workers and their families. • Finance Companies • • Offer short-term loans to borrowers in exchange for collateral.

THE FEDERAL RESERVE SYSTEM • Federal reserve system U.S. central bank. • Organization of the Federal Reserve System • • Nation divided into 12 federal districts. • • Each district bank supplies banks within its district with currency and facilitates the clearing of checks. • • Governed by a board of directors. • • Federal Open Market Committee sets monetary and interest rate policies. • Check Clearing and the Fed • • Clears checks and transfers money to and from financial institutions to improve the efficiency of the financial system.

Monetary Policy • Monetary policy Using interest rates and other tools to control the supply of money and credit in the economy.

U.S. FINANCIAL INSTITUTIONS: A GLOBAL PERSPECTIVE • • Major U.S. banks have extensive international operations. • • U.S. banks have more than $200 billion in outstanding loans to international customers. • • Only 3 of the 20 largest banks in the world (measured by total assets) are U.S. institutions • • Japan’s Mitsubishi UFJ Holdings is world’s largest. • • Other nation’s central banks play roles much like the Fed, often responding to changes in the U.S. financial system.