Download

1 / 47

470 likes | 478 Views

The Employer Basics. Affordable Care Act The Basics of Self Funding. 11106s0513 Edition 05.20.13. Allied National. Innovation Stability Service. 2. Why would an employer self fund? Why take the risk?. Self funding is the most cost effective way to fund a health plan over the long term.

E N D

The Employer Basics • Affordable Care Act • The Basics of Self Funding 11106s0513 Edition 05.20.13

Allied National Innovation Stability Service 2

Why would an employer self fund? Why take the risk? • Self funding is the most cost effective way to fund a health plan over the long term. • If costs are equal, why wouldn’t you choose a plan that gives you a refund during a healthy year? 3

What does the ACA have to do with self funding? • Avoids the high costs & rate shocks of fully insured plans under the ACA. 4

Affordable Care Act • What does it mean for me? • What does it mean for my business? • What does it mean for my employee’s health plan? 5

For the Individual - Employee What does ACA mean for an individual? • Individual Mandate says individual must have health insurance or pay a penalty • Penalty starts at $95 for 2014 then in 2016 escalates to $695 or 2.5% of taxable income (which ever is greater) • Insurance can be employer provided or an individual plan • Must be qualifying coverage • New health insurance exchanges for 2014 • Only way for individual to receive premium subsidy for their coverage 6

For Your Business - Employer What you need to know about ACA for your business . . . … 7

Do I have to offer health insurance to my employees? more than 50 less than 50 Based on full-time equivalent employee counts. Part-timers count! 8

What type of coverage must I offer? • Must offer coverage for all full-time employees and dependents (not spouses) • Must offer ACA defined minimum essential coverage (MEC) that meets minimum value • Must be affordable for each employee (“affordable” is defined by their income) 9

What is “Minimum Essential Coverage?” • Must cover a minimum of 60% of expected costs (called a Bronze Plan in the Exchange/Marketplace) • Fully insured plans must offer all 10 categories of essential benefits • Self-funded plans must only meet the 60% threshold(“minimum value”) • Required benefits are determined on a state by state basis and final regulations in each state are still to come 10

What are “Minimum Essential Benefits”? • 10 defined essential benefits – must be covered without $$ limits • Ambulatory patient services • Emergency services • Hospitalization • Maternity and newborn care • Mental health and substance abuse • Prescription drugs • Rehabilitative and habilitative services and devices • Lab services • Preventive and Wellness • Pediatric (including dental and vision) 11

What does “affordable” mean? • Affordable….. • The employer pays enough of the costs so that the employee’s share of the cost for single coverage is not: • More than 9.5% of the employee’s W-2 income; or • More than 9.5% of employee’s hourly rate of pay * 130 hours; or • More than 9.5% of FPL 12

What does “affordable” mean? Example The affordability test appliesto the employee cost (premium) only. Employee Income $28,735 Maximum Contribution by Employee is 9.5% $2729 ($227/month) 13

What happens to our business if we do NOT offer health insurance to our employees? • < 50 full-time employees • No requirement to offer coverage • No penalties • >50 full-time employees • Penalty if ANY employee goes to exchange and receives a subsidy: • Failure to provide Minimum Essential Coverage with minimum value • $2,000 per eligible full-time employee after the first 30 • Failure to make coverage affordable • For each employee who buys coverage on the exchange and receives a premium subsidy the penalty is $3000 14

What happens to our business if we DO offer health insurance to our employees? • It must meet minimum essential benefits standards • It must be affordable • If it’s affordable and meets minimums – • NO PENALTIES 16

Are there any new additional taxes or penalties under ACA that our business should be aware of? • YES • Transitional Reinsurance Tax – minimum$63/head beginning in 2014; to be adjusted every year through 2016 as required. • PCORI - Research Tax- $1/person/year in 2013; $2; in 2014; then indexed to national expenditures. 17

Will we still be able to have a health insurance broker to help us through this process? YES….but Plan on paying a consulting fee such as you would your accountant or lawyer. Most agents’ commissions have been greatly reduced or eliminated under the ACA. 18

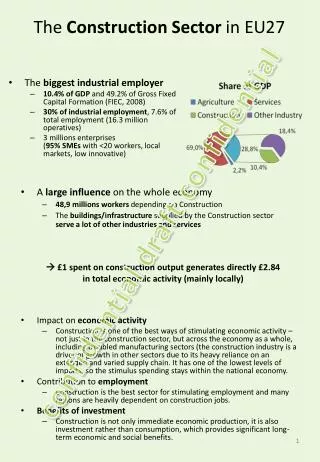

Adverse Impact of Affordable Care Act on Fully Insured Employers Increases Cost $ Community rating Minimum essential coverage 3:1 age slope rating Benefit Expansions Guarantee Issue Pre-ex included

Adverse Impact of Affordable Care Act on Fully Insured Employers? Allied “On the Air” Topics http://www.alliednational.com/ontheair.htm ________________________________________ Insurance Market ReformsAn explanation of what the reforms are, why they're part of ACA and what the rate impacts will be. Discusses options employers and individuals have to avoid the large fully insured rate increases resulting from the reform. Part 1: Affordable Care Act basics: 4 min. 49 sec. Part 2: Affordable Care Act impacts: 13 min. 30 sec. Part 3: Employer Options: 6 min 17 sec. Part 4: Individual Options: 2 min 39 sec.

How can we control the cost of our health insurance as a business? Self Insure Long term, self insuring /self funding is the most cost effective way for an employer to fund their employee health plan – even for smaller employers.

Why Would a Small Business Want to be Self Funded? Projected Self Funding Costs

Traditional Self Funding 65% >100 72.8M FTEs Who is self funded now…. Small Group Self Fundingand Fully Insured 24% >10 and <100 26.8M FTEs Fully Insured 11% <10 12.3M FTEs 100% 111.9M FTEs 11136s0413

Stop Loss Insurance Employer’s risk is contained 27

Self Funded Claim PaymentSample $60,000 Claim Employers Specific Stop Loss $33,000 Paid by Stop Loss Carrier Employers Aggregate Stop Loss Employers Specific Stop Loss Limit $25,000 Paid from employers claim fund Employers Claims Fund $2,000 Paid by employee 29

A new solution for smaller employers! 32

Self Funding “on training wheels” 10 or more lives Self funding made “SIMPLE” Prepackaged plan docs, integrated specific and aggregate stop loss policy Level monthly payment plan Terminal liability coverage included No hidden fees No complex contracts What is Funding Advantage? 33

Who is the ideal candidate • Experiencing adverse premium impact from ACA • Desires lower costs and predictable cash flow • Being forced to provide health insurance by ACA • Healthy groups • Desires greater control and flexibility • Needs better claims reporting • Promotes health and wellness with employees 34

Self Funded Group Health Plans are subject to “ERISA” regulation. What is ERISA? Employee Retirement IncomeSecurity Act 1974

Role of Allied as the Self Funded Plan Administrator • Assist with plan design • Manage Stop Loss claims • Assist with plan communications • Provide network access • Claims payment • Large claims management • Manage claim cost containment vendors • Reporting and compliance services 37

Allied National’sUnique Underwriting Philosophy TODAY Traditional Underwriting Past history Price based on past health history, experience, industry trends, and industry loads Allied National Underwriting Future costs Price based on futurehealth care costs

Self Funding Sample Case Study 85 Employees $6.5M Sales - pretax profit 12% Renewal Premium $612,000 Self Funded Program $610,000 Employer’s Loss Fund $366,000 Projected Refund 20% ($73,200) Net Cost $536,800 Refund = 9.3% of profit 39

Why Would a Small Business Want to be Self Funded? Projected Self Funding Costs

Why Would a Small Business Want to be Self Funded? “Employee Only” Rate Illustration $700 Fully Insured $600 2014-2015 ObamaCare Rate Shocks “Employee Only” Rate Self Funded $500 Potential Refunds $400 $300 2013 2014 2015 2016 2017 2018 Year This sample chart illustration is provided for educational purposes only. Actual results may vary and are not indicative of future performance. Allied National, Inc. l 4551 W. 107th St. Suite 100 l Overland Park, KS 66207 l 888-767-7133 l sales@alliednational.com l www.alliednational.com l twitter.com/alliednational 11149s0513

Next Steps • Agent contacts Allied • Current census • Plan design & benefits • Current and renewal billing

Life Cycle of a Funding Advantage Client start Allied National, Inc. l 4551 W. 107th St. Suite 100 l Overland Park, KS l 888-767-7133 l sales@alliednational.com l www.alliednational.com l twitter.com/alliednational

WARNING! Projected market capacity bottleneck. 4th Quarter 2014 DON’T WAIT!

In the works withAllied National! Unique small group self funded product for the low wage employee 3rd Quarter 2013

Thank you! For more information: Allied Sales Support 888-767-7133 www.alliednational.com sales@alliednational.comtwitter.com/alliednational Fax: 913-945-4396 Allied National, Inc.4551 W. 107th St. #100Overland Park, KS 66207 This is an invitation to inquire about the Allied Funding Advantage plan. This is a limited description of the plans. See plan brochure and plan documents for complete details.