Download

1 / 150

1.51k likes | 1.52k Views

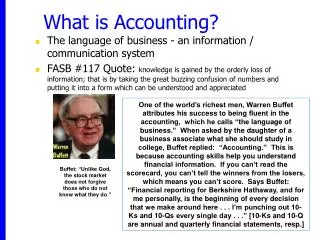

What is Accounting. The provision of information of an economic or financial nature. Enable to make better decision. What is Bookkeeping. Book-keeping is the process of recording the monetary worth of business transactions in the books of accounts. It is the record-making phase of accounting.

E N D

What is Accounting The provision of information of an economic or financial nature. Enable to make better decision.

What is Bookkeeping • Book-keeping is the process of recording the monetary worth of business transactions in the books of accounts. It is the record-making phase of accounting.

The Major Users of Accounting Information • Owners • Management • Lenders • Suppliers of Goods and Creditors • Customers • Competitors • Government • Employees • The Public

Accounting Equation Assets = Capital + Liabilities (Resources in the business) (Resources Supplied by the owner) (Resources Supplied by outsiders)

The Balance Sheet • The expression of the accounting equation

Example • The introduction of capital • 1 July 1997 • Peter opened a bank account for this new business and paid in a cheque of $40,000 as his investment in the business.

Example • The purchase of stock by cheque • 4 July 1997 • The business bought goods for resale of $5,000 by cheque.

Example • The purchase of stock by incurring a liability (i.e. deferring payment) • 10 July 1997 • The business bought goods $10,000 on credit from P.Tang.

Example • Sale of stock for cash • 20 July 1997 • Sold goods for cash $4,000.

Example • Sale of stock on credit • 22 July 1997 • Sold goods on credit to ABC Ltd. $1,000.

Example • The settlement of a liability • 25 July 1997 • Paid money owing to P.Tang by cash $4,000.

Double-Entry System • Every transaction affects two items in the balance sheet.

The Format of an Account • Traditional Format “T form” • The left-hand side is called the debit side. • The right-hand side is called the credit side. (ii) Computerized Format

Assets • They are economic resources which provide benefits to the business.

Assets • Fixed Assets • Current Assets

Fixed Assets • Intangible Fixed Assets • Tangible Fixed Assets

Intangible Fixed Assets E.g. • Goodwill • Patents • Franchises • Royalties • Development • Expenditures

Tangible Fixed Assets E.g. • Land and Buildings • Premises • Furniture & Fittings • Office Equipment • Machinery • Motor Vehicles • Long-term Investments

Current Assets E.g. • Stock • Debtors • Current Investments • Prepaid Expenses • Bills Receivable • Accrued Income • Bank/Cash

Liabilities • They are debts or obligations owed by the business to outside parties.

Liabilities • Long-term Liabilities (Repayable beyond the next accounting year) • Current Liabilities (Repayable within the next 12 months)

Long-term Liabilities E.g. • Debentures • Bank Loans • Loans from Others

Current Liabilities E.g. • Creditors • Accrued Expenses • Prepaid Income • Bank Overdrafts

Capital • Capital is what the company owed to the owners. • It is a liability of the business to its owners.

Any asset account Increase + Decrease - Any liability account Decrease - Increase + Capital account Decrease - Increase +

Example (A) • 1 May 2004 • Transaction • Started an engineering business putting $1,000 into a bank account. • Effect • Increases asset of bank • Increases capital of owner • Action • Dr. Bank account • Cr. Capital account

Bank 2004 $ May 1 Capital 1000 Capital 2004 $ May 1 Bank 1000

Example (B) • 3 May 2004 • Transaction • Bought machinery on credit from Unique Machines $275. • Effect • Increases asset of machinery • Increases liability to Unique Machines • Action • Dr. Machinery account • Cr. Unique Machines account

Machinery 2004 $ May 3 Unique 275 Unique Machines (Creditor) 2004 $ May 3 Machinery 275

Example (C) • 4 May 2004 • Transaction • Withdrew $200 cash from the bank and placed it in the cash box. • Effect • Increases asset of cash • Decreases asset of bank • Action • Dr. Cash account • Cr. Bank account

Cash 2004 $ May 4 Bank 200 Bank 2004 $ 2004 $ May 1 Capital 1000 May 4 Cash 200

Example (D) • 7 May 2004 • Transaction • Bought a motor van paying in cash $180 • Effect • Increases asset of motor van • Decreases asset of cash • Action • Dr. Motor Van account • Cr. Cash account

Motor van 2004 $ May 7 Cash 180 Cash 2004 $ 2004 $ May 7 Motor van 180 May 4 Bank 200

Example (E) • 10 May 2004 • Transaction • Sold some of the machinery for $15 on credit to S. Au. • Effect • Increases asset of money owing by S. Au • Decreases asset of machinery • Action • Dr. S. Au’s account • Cr. Machinery account

S Au (Debtor) 2004 $ May 10 Machinery 15 Machinery 2004 $ 2004 $ May 3 Unique 275 May 10 S Au 15

Example (F) • 21 May 2004 • Transaction • Returned some of the machinery, value $27, to Unique Machines. • Effect • Decreases liability to Unique Machines • Decreases asset of machinery • Action • Dr. Unique Machines • Cr. Machinery account

Machinery 2004 $ $ May 3 Unique Machines (B) 275 2004 May 10 S. Au (E) 15 May 21 Unique Machines (F) 27 Unique Machines (Creditor) 2004 $ 2004 $ May 21 Machinery 27 May 3 Machinery 275

Example (G) • 28 May 2004 • Transaction • S. Au paid the firm the amount owing, $15, by cheque. • Effect • Increases asset of bank • Decreases asset of money owing by S. Au. • Action • Dr. Bank account • Cr. S. Au’s account

S. Au (Debtor) 2004 $ 2004 $ May 10 Machinery (E) 15 May 28 Bank (G) 15 Bank 2004 $ 2004 $ May 1 Capital 1000 May 4 Cash 200 May 28 S Au 15

Example (H) • 30 May 2004 • Transaction • Bought another motor van paying by cheque $420. • Effect • Increases asset of motor vans • Decreases asset of bank • Action • Dr. Motor van account • Cr. Bank account

Motor van 2004 $ May 7 Cash 180 May 30 Bank 420 Bank 2004 $ 2004 $ May 1 Capital 1000 May 4 Cash 200 May 28 S Au 15 May 30 Motor van 420

Example (I) • 31 May 2004 • Transaction • Paid the amount of $248 to Unique Machines by cheque. • Effect • Decrease liability to Unique Machines • Decrease asset of bank • Action • Dr. Unique Machines • Cr. Bank account

Bank $ 2004 $ May 1 Capital (A) 1,000 2004 May 4 Cash (C) 200 May 28 S.Au (G) 15 May 30 Motor Van(H) 420 May 31 Unique Machines (I) 248 Unique Machines (Creditor) 2004 $ 2004 $ May 21 Machinery 27 May 3 Machinery 275 May 31 Bank 248

The double entry system: The treatment of stock • The stock of goods in a business is constantly changing because some more of it is bought, some of it is sold, some is returned to the suppliers and some is returned by the customers.

The treatment of stock In four accounts: Purchases account For the purchase of goods Sales account For the sales of goods Returns inwards account For goods returned to the firm by its customers Returns Outwards account For goods returned from the firm to its suppliers

As stock is an asset, • these four accounts are all connected with this asset, • the double entry rules for these four accounts are those used for assets.

Purchases of stock on credit (Credit Purchases) • Dr. Purchases account • Cr. Creditor/Supplier account

Example: • 1 August 2004 • Goods costing $165 were bought on credit from D. Hong. • The asset of stock is increased. • An increase in a liability

Purchases 2004 $ Aug 1 D. Hong 165 D. Hong (Creditors) 2004 $ Aug 1 Purchases 165

Purchases of stock for cash (Cash Purchases) • Dr. Purchases account • Cr. Cash