Download

1 / 32

320 likes | 376 Views

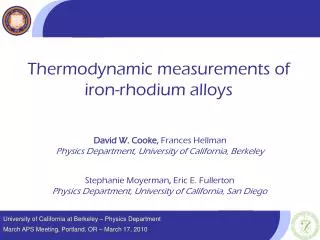

Crisis and Growth in the Advanced Economies: What we know, what we don’t, and what we can learn from the 1930s. Barry Eichengreen University of California, Berkeley October 2010.

E N D

Crisis and Growth in the Advanced Economies:What we know, what we don’t, and what we can learn from the 1930s Barry Eichengreen University of California, Berkeley October 2010

I argue in my paper that a high degree of uncertainty surrounds the question of whether the medium- and long-term growth potential of the advanced economies has been impaired. • This uncertainty arises for two reasons. • At least two…

First, because “this time is different” • In other words, experience in other recent crises is of dubious relevance to the current episode. Previous studies have looked at the trend rate of growth before and after a set of banking crisis dates. But those crises are heterogeneous: while some are as serious as the recent episode, others are considerably less so • Moreover,the crises considered are idiosyncratic national events, in contrast to the recent crisis, which infected the entire OECD. • Thus, the opportunity for individual countries to export their way out of trouble did not arise to anywhere near the same extent in the recent episode. • Finally, where previous studies look at growth in the wake of banking crises, the recent episode is more than just a banking crisis. • It affected the shadow banking system and securitization markets at the same time and even more powerfully than the banks.

Second, estimating what happened to trend growth presupposes an ability to measure the trend • But the trend is not constant in the absence of a crisis. A pre-crisis trend estimated over a relatively long period may understate pre-crisis growth potential and therefore understatepost-crisis damage if productivity growth was accelerating prior to the crisis. • Recall the “new economy” argument that U.S. productivity growth accelerated around the middle of the 1990s due to the adaptation to new information and communications technologies. If there really was and is a new economy, then attempting to measure the trend rate of growth over a longer period will underestimate it. • Alternatively, measuring pre-crisis growth over a shorter period, say as growth between the two immediate pre-crisis business-cycle peaks, creates the danger that estimates of the trend will be distorted by peculiar features of the cyclical expansion and the unsustainable growth that sowed the seeds for the crisis itself. • This will tend to overestimate pre-crisis growth and exaggerate the damage.

Given this, I will argue that progress on answering the question – has growth potential been impaired? – will occur through research on specific mechanisms through which recession and financial distress affect growth capacity.

In addition, I will suggest that historical evidence from earlier episodes like the 1930s – when the recession was deep, the crisis was global, and financial distress was pervasive – is a promising source of information on the issues at stake. • Indeed, it maybe the only source, given that it is too early to definitively evaluate the long-term consequences of the (still) recent crisis.

My bottom line • On economic grounds (and on the basis of the experience of the 1930s), I’m more optimistic about the US economy (and less worried that growth potential has been seriously damaged) than most people in this room. • But on political grounds (outcomes also depend on policy, and policy depends on politics), I’m more pessimistic.

My list of potential mechanisms 1) Impairment of the financial system • Heavier public debt burden • Costly structural change associated with rebalancing (and sometimes associated with structural unemployment) • Reduced R&D spending and related factors leading to lower productivity growth

Channel 1: Impairment of the financial system • Weakly capitalized banks may be reluctant to lend. • Burned once, they adopt tighter lending standards. • Aspiring borrowers, having suffered balance sheet damage, have less collateral and are less credit worthy. • More stringent regulation adopted in response to the crisis requires financial institutions to hold more capital and liquid assets and to otherwise restrain their lending. • A more limited supply of bank credit will mean a higher cost of capital. The lesser availability of finance will mean less investment. This effect is most likely to be felt by smaller, younger firms that are disproportionately the source of innovation and employment growth in normal times, that cannot expand on the basis of internal funds, and that find it difficult to tap securities markets. • Jan Hatzius of Goldman issued a report arguing all this yesterday…

Evidence of a persistent slump in bank lending in the 1930s is there • You can see it here. Between 1933 and 1937 the U.S. economy grew by more than 8 per cent per annum, but bank lending grew hardly at all. • In part this reflected balance-sheet problems: using state-level data, Calomiris and Mason show that banks with less capital and more real-estate losses grew their loans more slowly in the 1930s. • In part it reflected the flight from risk and scramble for liquidity by all banks: studies of individual bank data show that banks curtailed their lending and shifted into holding more liquid, less risky assets (primarily cash and treasury securities) following depositor runs in 1931 and 1933.

But how much difference this made for investment & growth is less clear • Here we have US capital spending as a percentage of GDP. • There is something of a recovery. • It kind of looks like firms were not credit constrained.

But how much difference this made for investment & growth is less clear • Indeed, a pair of surveys conducted by the National Industrial Conference Board found only limited evidence of borrowing difficulties. In 1932, 86 per cent of the responding industrial firms indicated either no attempt to borrow or no difficulty in obtaining bank credit. • It of course could be that the large number of respondents reporting no recourse to bank credit reflected the depressed circumstances of the time (no demand meaning no investment plans). • Alternatively, many firms may have been intent on deleveraging as a way of reducing their vulnerability to financial disturbances (so would argue Richard Koo).

But how much difference this made for investment & growth is less clear • Butof regular bank borrowers, nearly a quarter reported difficulties of borrowing. The firms in question were disproportionately small. • The 1939 NICB study concluded that the majority of loan refusals reflected changes in the instructions given loan officers (“bank policy”) and not the condition of the borrowing firm or its industry.

Channel 2: Additional public debt burden • Reinhart and Rogoff (2009) have famously shown that financial crises leave a scar of higher public debt. • Their stylized fact, based on experience in 13 post-World War II financial crises, is that real public debt doubles in the three years following onset. • The increase is due to a combination of lower tax revenues and increases in public spending in response to the crisis. • Higher debt burdens imply higher future taxes, higher interest rates and, other things equal, lower levels of investment and slower rates of growth.

But the other-things-equal caveat is obviously a big one • The argument that government deficits leading to higher debts crowd out private investment and depress growth operates mainly through higher interest rates, and there is no evidence of upward pressure on interest rates at the moment. • Deficit spending directed at recapitalizing a weak banking system and stabilizing economic activity, by restoring confidence, may do more to encourage investment than depress it. • The debt ratio may also rise insofar as the economic conditions are depressed and deflationary (that is to say, for other reasons). • Slow growth may cause heavy debts rather than the other way around.

The 1930s is again an obvious battleground for the competing views • In the U.S., the public debt/GDP ratio more than doubled from 17 per cent in 1929 to 40 per cent in 1933-37. • But the 1930s were, you will anticipate, not a period of high interest rates; just as in recent years, precisely the opposite was true. Arithmetically, the main factor behind the rise in the debt ratio was the fall in nominal GDP by nearly 50 per cent between 1929 and 1933. • The swing in the federal government deficit as a percentage of GNP between 1929 and 1933 was a relatively modest 4 per cent; this is telling us that the rise in indebtedness was mainly driven by the fall in GDP, not the other way around.

So those seeking to argue that public policy discouraged investment must look elsewhere

So those seeking to argue that public policy discouraged investment must look elsewhere • Some historians of the 1930s, like some current commentators, look to policy uncertainty. • Robert Higgs has famously made this argument about the effects of New Deal policies. • Notice his title…

Higgs looks at time variation in investment and policy uncertainty under Roosevelt • He argues that policy uncertainty, especially in the mid-1930s (Supreme Court throwing out the First New Deal, leading to the Second New Deal, etc.), depressed investment, especially around 1937-8. • 1938 then saw a significant change in the makeup of the Roosevelt Administration, with the replacement of dedicated New Dealers by pro-business men, and a strong Conservative Coalition opposing the New Deal in the Congress after the 1938 congressional election. • This was followed by a substantial rise in gross private investment in 1939 and again in 1940. • But the rise in investment is equally attributable to other factors, such as recovery from a 1937-8 recession widely attributed to the Fed’s decision to raise reserve requirements. So there is reason to doubt Higg’s argument (just like one might question the policy-uncertainty argument now).

Fortunatelyfor us, there is also a paper by Mayer and Chatterji (1985) that looks directly at the impact of policy shocks on industrial equipment orders and investment in nonresidential structures. • The authors find no evidence that it was policy shocks, as opposed to other plain-vanilla determinants of investment (like the cycle) that drove investment spending.

So why did investment remain low? • The most convincing explanation is extensive unutilized capacity (shown here). • This was the explanation of the original historian of U.S. capacity utilization in the 1930s (Streever 1960). • Capacity utilization in U.S. industry fell from 83 per cent in 1929 to 42 per cent in 1932; at its peak in 1937 it just matched the 1929 level of 83 per cent before falling back again in 1938 and 1939.

Channel 3: Structural changes that reduce labor input and efficiency • It’s harder to grow when you have to retrain construction workers and hedge fund managers to work as welders and nurses, as will be the case when the economy is rebalancing away from unsustainable activities that boomed before the crisis. • Firms may not be able to find workers with the requisite training and experience. • The mismatch between skills supplied and demanded may then constrain the growth of employment. • One currently hears complaints from manufacturing firms of a shortage of, inter alia, machinists.

Similar complaints were heard in the 1930s • Motor vehicle manufactures in Oxfordshire complained that Welsh coalminers lacked both the skills and attitudes required of productive factory workers. • More generally, mismatch is a theme in studies of the British labor markets in the 1930s.

Similar complaints were heard in the 1930s • Steve Nickell and coauthors (1989) develop an empirical measure of the extent of mismatch in interwar Britain , summing the absolute value of the change in the share of total employment across 27 industries. • They show that a high level of mismatch moderated the downward pressure on real wages normally exerted by a rise in the number of unemployed workers, in turn limiting employment and output growth in their model. • This was especially a problem in the early 1930s, as we see here. • But notice also how quickly evidence of mismatch evaporates with recovery.

Members of this audience will be familiar with the debate over whether there is a problem of structural unemployment now that will resist the application of aggregate demand stimulus, or whether supposed structural unemployment will dissolve in the face of demand stimulus. • My own views, based on this 1930s experience, are closer to those of the guy with the beard.

Channel 4: Negative impact on R&D and productivity growth • Research and development, especially by small firms and startups, is sensitive to the availability of venture funding. R&D has a long lead time, which means that financial disruptions can have persistent. • And, in fact, there was a sharp drop in R&D activity in the early 1930s due to the depth of the economic collapse and tighter financial constraints.

But this history also points to the possibility of a more positive outcome • Rather than being depressed as the previous perspective would suggest, TFP growth in the 1930s in the United States was unusually fast. • Between 1929 and 1941, TFP growth ran at 2.3 per cent, faster than any other time in the 20th century.

What explains this? • As the economic historian Alexander Field has shown, many firms took the “down time” created by the weak demand for their products to reorganize their operations. • In the U.S., factories that had previously utilized a single centralized power source installed more flexible small electric motors on the shop floor. • Railways reorganized their operations to make more efficient use of both rolling stock and workers. • More firms established modern personnel-management departments. • Others put in placein-house research labs.

There are hints of U.S. firms responding similarly now. • General Motors, faced with an existential crisis, has sought to transform its business model. • U.S. airlines have used the lull in demand for their services to reorganize both their equipment and personnel, much like the railways in the 1930s. • Firms in both manufacturing and services are adopting new information technologies, the 21st century analog to small electric motors, to optimize supply chains and quality management systems.

Of course nothing guarantees a positive response • Britain also suffered a severe negative shock in the 1930s, but productivity responded much less positively. Why? • The answerin the literature is: policy. The UK responded with import barriers, restraints on domestic competition, heavy regulation of public utilities, all of which hindered or discouraged the impulse to reorganize. • But this only strips one more layer off the onion. Why did it respond in this restrictive way?

Authors likeCavallo and Cavallo (2008) argue that constructive (as distinct from reactionary) policy reforms are more likely to follow a crisis when the political system possesses the capacity to derive lessons from the crisis and act on them. They point to political stability, cohesion and strong majority governmentsas determinants of this capacity. • In the UK, the political system arguably lacked this capacity. British politics became increasingly polarized in the 1930s and after WWII. There were repeated erratic swings in government between Labour and the Conservatives. No ability of the two main parties to work together. • Authors like Broadberry and Crafts trace the policy implications.

I thus leave you with a question: • Do we now have to worry that the United States suffers from the kind of disfunctional political system that hindered successful adjustment in the UK in the 1930s?