Download

1 / 8

80 likes | 292 Views

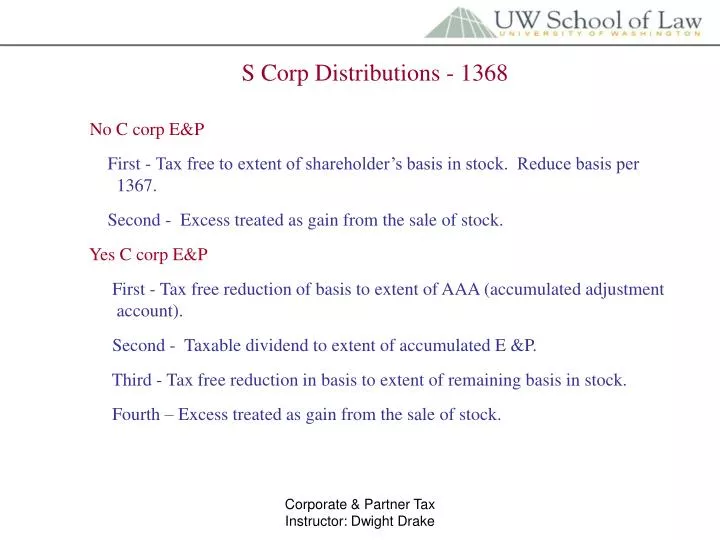

S Corp Distributions - 1368. No C corp E&P First - Tax free to extent of shareholder’s basis in stock. Reduce basis per 1367. Second - Excess treated as gain from the sale of stock. Yes C corp E&P

E N D

S Corp Distributions - 1368 No C corp E&P First - Tax free to extent of shareholder’s basis in stock. Reduce basis per 1367. Second - Excess treated as gain from the sale of stock. Yes C corp E&P First - Tax free reduction of basis to extent of AAA (accumulated adjustment account). Second - Taxable dividend to extent of accumulated E &P. Third - Tax free reduction in basis to extent of remaining basis in stock. Fourth – Excess treated as gain from the sale of stock. Corporate & Partner Tax Instructor: Dwight Drake

S Corp Property Distributions 1. FMV is measure of distribution to shareholder – apply normal distribution rules at shareholder level. 2. Shareholder’s basis in property is FMV. 3. S corp has gain equal to excess of FMV over basis, which is passed through to shareholders. 311(b) via 1371(a). 4. No loss recognized if FMV less than basis at corporate level. 311(a) via 1371(a). Corporate & Partner Tax Instructor: Dwight Drake

Problem 910 - 1 Basic Facts: A Corp calendar year S; D owns 1/3, share basis 3k; M owns 2/3, share basis 5k; Corp has 9k net operating income, 3k LTCG. A Corp distributes 5k to D and 10k to M on 10/15. D: 3k of ordinary income; 1k LTCG. Basis adjusted up 4k to 7k. Basis adjustment required before characterizing distribution. 5k reduces basis to 2k. M: 6k ordinary income; 2k LTCG. Basis pre-distribution up to 13k; after 10k distribution down to 3k. A Corp distributes 8k to D, 16k to M. D: Pre-distribution 7k basis reduced to zero. 1k gain on sale of stock. M: Pre-distribution 13k basis reduced to zero; 3k gain on sale. Corporate & Partner Tax Instructor: Dwight Drake

Problem 910 - 1 Basic Facts: A Corp calendar year S; D owns 1/3, share basis 3k; M owns 2/3, share basis 5k; Corp has 9k net operating income, 3k LTCG. A Corp redeems all D’s stock for 20k on 12/31. Basis still 7k. 13k gain recognized on sale. 10/15, redeem ¼ D stock for 5k, ¼ M stock for 10k. Considered dividend because pro rata. Same answer as (a). (e) Land to D – 8k FMV, 9k basis. Land to M – 16k FMV, 13k basis. D: No loss to corp; 1k of 3k gain on land to M increase pre-distribution basis to 8k; land distribution reduce basis by FMV (8k) to zero. D basis in land 8k. M: Corp has 3k gain, 2k allocated to M. Pre-distribution basis is 15k. Land distribution 16k; 1k treated as gain on stock sale. M basis in land is 16k. Corporate & Partner Tax Instructor: Dwight Drake

Problem 910 - 1 Basic Facts: A Corp calendar year S; D owns 1/3, share basis 3k; M owns 2/3, share basis 5k; Corp has 9k net operating income, 3k LTCG. 12% notes distributed by A Corp, 8k FMV to D, 16K FMV to M. No corp gain under 311(b)(1)(A). D – 7k pre-distribution basis; zero basis post-distribution; 1k gain on stock sale; basis in note 8k. M – 13k pre-distribution basis; zero basis post-distribution; 3k gain on stock sale; basis in note 16k. Corporate & Partner Tax Instructor: Dwight Drake

Problem 910 - 2 Basic Facts: P Corp new S corp, 6k accumulated E&P from C years. O & N equal shareholders – O basis 5k, N basis 1k. P current operating income 6k (32-18-8) and LTCG of 4k. Distributes 5k to each of O and N on 11/15. - Basis of each increased 3k plus 2k, or 5k. O basis pre-distribution increased to 10k, then down to 5k post-distribution. - N basis pre-distribution basis to 6k, then reduced to 1k post-distibution. - P Corp accumulated adjustment account increased 10k for earnings (6k plus 4k) and then reduced 10k for distributions. Hence, zero. Same, but 10k each distribution. O – 5k current accum. adj account; 3k accumulated E&P; 2k reduction in basis. Basis reduced to 3k. N – 5k accum adj. account; 3k accumulated E&P; 1k basis recovery; 1k gain on stock sale. Stock basis 0. P Corp – accum adj account is zero. Corporate & Partner Tax Instructor: Dwight Drake

Problem 910 - 2 Basic Facts: P Corp new S corp, 6k accumulated E&P from C years. O & N equal shareholders – O basis 5k, N basis 1k. P current operating income 6k (32-18-8) and LTCG of 4k. Same as (a), but P Corp also received 4k tax exempt interest and distributes 2k each to N and O. N – Basis in stock increased to 8k (1k plus 5k plus 2k). 5k is distribution of accum. adjustment account (which not increased for tax-exempt interest); 2k extra distribution dividend of C corp earnings. N stock basis 3k. O – Basis in stock increased to 12k (5k plus 5k plus 2k). 5k is distribution of accum. adjustment account (which not increased for tax-exempt interest); 2k extra distribution dividend of C corp earnings. N stock basis 7k. (d) N sells stock to R for 6k on 1/1 next year. 10k accumulated E&P. No earnings next year. Corp distributes 6k to R in 2/15. 5k basis recovery from accum adj. account picked up as N’s transferee. 1k dividend from C corp E&P. Corporate & Partner Tax Instructor: Dwight Drake

Problem 910 - 2 Basic Facts: P Corp new S corp, 6k accumulated E&P from C years. O & N equal shareholders – O basis 5k, N basis 1k. P current operating income 6k (32-18-8) and LTCG of 4k. No distribution current year. 1/1 next year revoke S election. 5k E&P next year and 7k distribution to each shareholder on 8/1 next year. - Per 1371(e)(1) distributions of former S corp during “post-termination transition period” (1 yr after last S day) may be treated as basis recovery from accum. Adj. account. So, here 5k to each can be basis recovery (because that each share of 10k accum. Adjust. Acount from prior year) and 2k dividend. - Per 1371(e)(2), may elect to treat all as dividend. C corp E&P 11k (6k prior and 5k current), do dividend 5.5k to each if election made. Extra 1.5k treated as return of capital. Corporate & Partner Tax Instructor: Dwight Drake