Download

1 / 21

370 likes | 876 Views

Chapter 2 The double entry system for assets, liabilities and capital. Learning objectives. After you have studied this chapter, you should be able to: Explain what is meant by ‘double entry ’ Explain how the double entry system follows the rules of the accounting equation

E N D

Chapter 2The double entry system for assets, liabilities and capital

Learning objectives After you have studied this chapter, you should be able to: Explain what is meant by ‘double entry’ Explain how the double entry system follows the rules of the accounting equation Explain why each transaction is recorded into individual accounts Describe the layout of a ‘T-account’

Learning objectives (Continued) Explain what is meant by the terms debit and credit Explain the phrase ‘debit the receiver and credit the giver’ Prepare a table showing how to record increases and decreases of assets, liabilities and capital in the accounts Enter a series of transactions into T-accounts

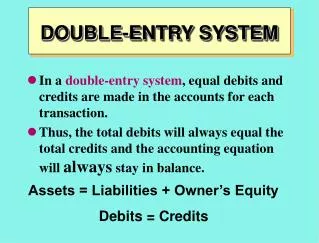

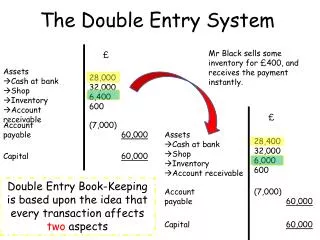

The double entry system Every transaction affects two items. These effects need to be shown in the accounting books. This is double entry bookkeeping.

Activity The owner starts the business with £10,000 in cash on 1 August 2012.

Activity (Continued) A van is bought for £4,500 in cash on 2 August 2012.

Activity (Continued) Fixtures (e.g. shelves) are bought on credit from Shop Fitters for £1,250 on 3 August 2008.

Activity (Continued) Paid the amount owning to Shop Fitters in cash on 17 August 2012.

Activity (Continued) Combining all four of these transactions, the accounts now contain:

Learning outcomes You should have now learnt: That double entry follows the rules of the accounting equation That double entry maintains the principle that every debit has a corresponding credit entry That double entries are made in accounts in the accounting books

Learning outcomes (Continued) Why each transaction is entered into accounts rather than directly into the statement of financial position How transactions cause increases and decreases in asset, liability and capital accounts How to record transactions in T-accounts