Download

1 / 4

40 likes | 212 Views

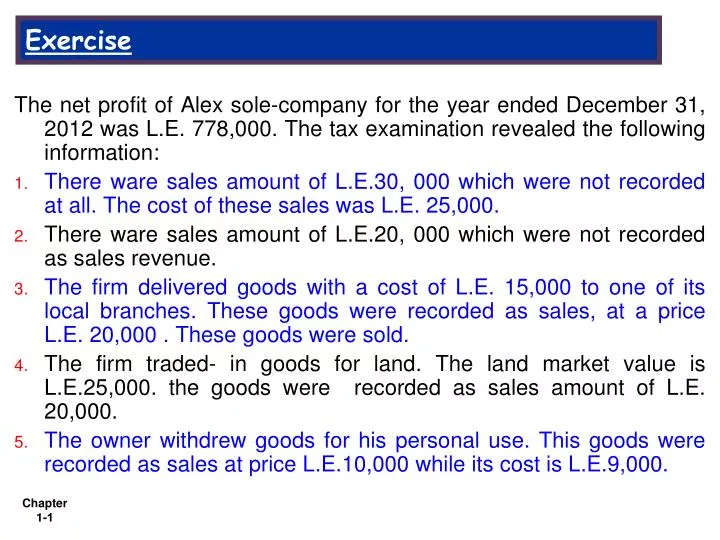

Exercise. The net profit of Alex sole-company for the year ended December 31, 2012 was L.E. 778,000. The tax examination revealed the following information: There ware sales amount of L.E.30, 000 which were not recorded at all. The cost of these sales was L.E. 25,000.

E N D

Exercise The net profit of Alex sole-company for the year ended December 31, 2012 was L.E. 778,000. The tax examination revealed the following information: • There ware sales amount of L.E.30, 000 which were not recorded at all. The cost of these sales was L.E. 25,000. • There ware sales amount of L.E.20, 000 which were not recorded as sales revenue. • The firm delivered goods with a cost of L.E. 15,000 to one of its local branches. These goods were recorded as sales, at a price L.E. 20,000 . These goods were sold. • The firm traded- in goods for land. The land market value is L.E.25,000. the goods were recorded as sales amount of L.E. 20,000. • The owner withdrew goods for his personal use. This goods were recorded as sales at price L.E.10,000 while its cost is L.E.9,000.

6- The income statement includes the following items: • L.E. 20,000 subsidies received. The amount includes L.E.10,000 received in cash and the remainder is in the form of furniture, its fair market is L.E. 17,000 • L.E.9,000 bad debts recovered including L.E. 7,000 was earlier allowed as deduction and the rest was not allowed. • L.E. 20,000 capital gain of a building which was sold for L.E. 90,000 in May,1 2012. The book value of the building for accounting purpose was L.E.70, 000 and for tax purpose was L.E.72, 000. • L.E. 10,000 interest expenses which include L.E. 2,000 belonging to interest on the owner's loan. The remaining interest was related to the loan of the owner's brother. The interest amount of this loan under the central bank equals L.E. 8,500. • L.E 20,000 contributions to government units. • L.E. 15,000 computer depreciation expense, while taxable computer depreciation expense L.E 14,000.

G-L.E. 10,000 the firm's share in social insurance. • H-L.E. 7,000 allowances for retirement compensation. This amount was deposited in the favor of the independent private insurance fund. The total wages = L.E 40,000. • 7- L.E. 12,000 compensation received from an insurance company for goods which were damaged by fire, the total amount of compensation was used to purchase other goods. This compensation was not recorded in the accounting books during the year. • 8- L.E.5,000 annual social insurance contribution of the owner is not recorded. • Required: • Make the necessary adjustments to measure the taxable net profit and the tax base of the firm for the taxable period 2012. • Determine the tax amount for the taxable period 2012.

The end of Tax accountability of Commercial and industrial profit

![[Exercise Name] Functional Exercise](https://cdn0.slideserve.com/621913/exercise-name-functional-exercise-dt.jpg)

![[Exercise Name] Functional Exercise](https://cdn1.slideserve.com/1717560/exercise-name-functional-exercise-dt.jpg)

![[Exercise Name] Functional Exercise](https://cdn3.slideserve.com/6680259/exercise-name-functional-exercise-dt.jpg)

![[Exercise Name] Tabletop Exercise](https://cdn4.slideserve.com/9191716/exercise-name-tabletop-exercise-dt.jpg)