Download

1 / 6

70 likes | 196 Views

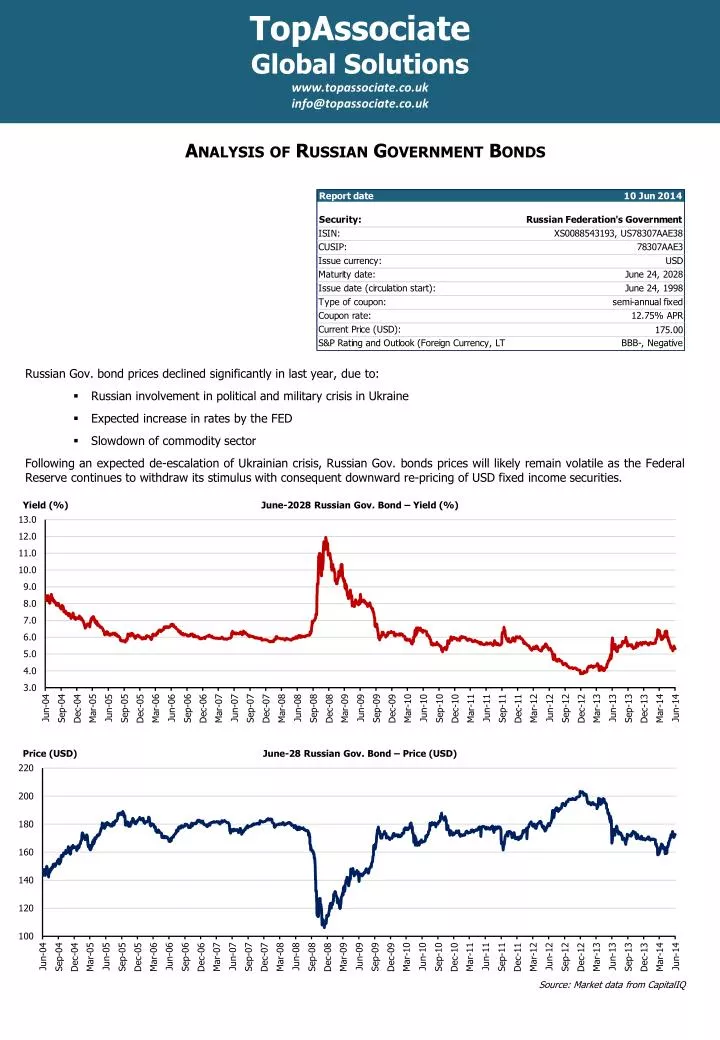

TopAssociate Global Solutions www.topassociate.co.uk info@topassociate.co.uk. Analysis of Russian Government Bonds. Russian Gov. bond prices declined significantly in last year, due to: Russian involvement in political and military crisis in Ukraine

E N D

TopAssociate Global Solutions www.topassociate.co.uk info@topassociate.co.uk Analysis of Russian Government Bonds • Russian Gov. bond prices declined significantly in last year, due to: • Russian involvement in political and military crisis in Ukraine • Expected increase in rates by the FED • Slowdown of commodity sector • Following an expected de-escalation of Ukrainian crisis, Russian Gov. bonds priceswilllikelyremain volatile as the Federal Reservecontinues to withdrawitsstimulus with consequent downward re-pricing of USD fixedincomesecurities. Yield (%) June-2028 Russian Gov. Bond – Yield (%) Price (USD) June-28 Russian Gov. Bond – Price (USD) Source: Market data from CapitalIQ

TopAssociate Global Solutions www.topassociate.co.uk info@topassociate.co.uk Russian Government Bonds: Key Positives and Negatives Key Positives The country is the world’s second producer of natural gas and the third producer of oil. The Russian Federation supplies a significant volume of fossil fuels and is the largest exporter of oil and natural gas to the European Union. The largest importers of gas are Germany and Italy but most EU countries are also dependent on Russian exports: this circumstance gives Moscow a significant geopolitical advantage. Public finances are extremely robust as central government debt is equivalent to circa 11 percent of Gross Domestic Product; moreover, most of this debt is denominated in Russian rubles. The government ran a deficit of 0.4 percent of GDP through the first four months of 2014, compared with a balanced budget last year. Unemployment rate in Russia decreased to 4.9 percent in May of 2014 from 5.3 percent in April of 2014. At the same time, industrial production increased 2.8 percent in May of 2014 over the same month in the previous year. Although thougher and more resilient forms of opposition are mounting, Vladimir Putin’s hold on power still seems undisputable. This ensures that the political situation in Russia is very stable – perhaps too stable – unlike in other developing countries. The amount of foreign currency reserves held by the Federation is absolutely appropriate to pay off its international obligations. Central bank gold holdings crossed the 1,000 tons mark for the first time during the third quarter of 2013, making Russia the 7th biggest gold holder in the world. Key Negatives Russia runs regular trade surpluses but the commodities boom driving Russian growth over the past decade has been slowing in recent times; natural resource dependence has arguably delayed much needed structural reforms. Federal budget revenues dropped to 19.5 percent of GDP in 2013 in comparison to 20.5 percent in 2012. This decline was caused by a reduction in both oil and non-oil revenue. In particular, oil revenues decreased in 2013 to 9.8 percent of GDP from 10.3 percent of GDP one year before. There is a long list of structural, home-grown problems including: the absence of spare industrial capacity, the lack of labour mobility, an ageing population and the low rate of private sector investment. Also, the business environment suffers because of high corruption levels and strong political interference: Transparency International ranked Russia 127th in its recently published 2013 Corruption Perceptions Index with a modest improvement over previous years. Inadequate rule of law is perhaps the major deterrent to foreign investment in the country. The political and military tensions with bordering Eastern European countries have recently soared to new heights following Russia’s occupation of Crimea. According to the International Monetary Fund, Ukraine-related sanctions by Western countries are scaring off investors and are pushing Russian economy towards recession. For this reason, the Fund cut its forecast on output growth to just 0.2 percent this year, down from a previous estimate of 1.3 percent. It also forecasts capital outflows of $100 billion as a result of geopolitical uncertainty. The Federal Reserve commitment for scaling back and ultimately ending its highly accommodative monetary policy could result in further capital outflows and sizable currency depreciation.

TopAssociate Global Solutions www.topassociate.co.uk info@topassociate.co.uk Swot Analysis Strengths Weaknesses • Abundant natural resources (oil, natural gas, metals…) • Skilled labour • Low public debt, strong government balance sheet, comfortable foreign currency reserves • Regional power and assured energy supply • Industrial and private sector’s lack of competitiveness • Dependence on public sector support and benefits • Weak infrastructures • Persistent business environment shortcomings • High Corruption Opportunities Threats • De-escalation of current political and military tensions • Commodity sector booming • Increased integration with the West and China • Positive re-rating based on Gov. balance sheet strenghts • Downward re-pricing of fixed income assets due to FED’s tapering and tightening • Political and military tensions with bordering Eastern European countries • Commodity sector worsening • Limited access to foreign currency markets • New threats from military tensions in Asia-Pacific territorial disputes

TopAssociate Global Solutions www.topassociate.co.uk info@topassociate.co.uk News-Flow Evolution 7 May 2014: Russian markets surge on Putin's claim of troops pullback 16 June 2014: Russia cuts off gas supply to Ukraine after talks on a long-running pricing dispute failed 19 September 2013: Federal Reserve unexpectedly decides against reducing monetary stimulus March 2014: Escalation of the political crisis in Ukraine: Russian forces take over Crimea Price (USD) June-28 Russian Gov. Bond – Price (USD) May-July 2013: bond prices, shares and commodities decline in anticipation of the Federal Reserve plans to scale down its bond-buying programme (Tapering) 25 April 2014: S&P downgrades Russia amid Ukraine crisis to BBB-, one notch above “junk” status 13 March 2014: Russian deploy troops near the Ukrainian border Source: Market data from CapitalIQ

TopAssociate Global Solutions www.topassociate.co.uk info@topassociate.co.uk Relevant Economic Data Source: IMF, Central Bank of Russia, Ministry of Finance, EIA

TopAssociate Global Solutions www.topassociate.co.uk info@topassociate.co.uk Debt Denominated in Foreign Currency and Exchange Rate USD million Russian Government Eurobonds by maturity RUB / USD Russian Ruble to US Dollar 2014 - History Source: CapitalIQ