Download

1 / 16

160 likes | 161 Views

This presentation discusses the main roles of internal audit, focusing on assurance services and consultancy services, as well as their implementation standards and particularities. It also includes a comparative analysis of these services.

E N D

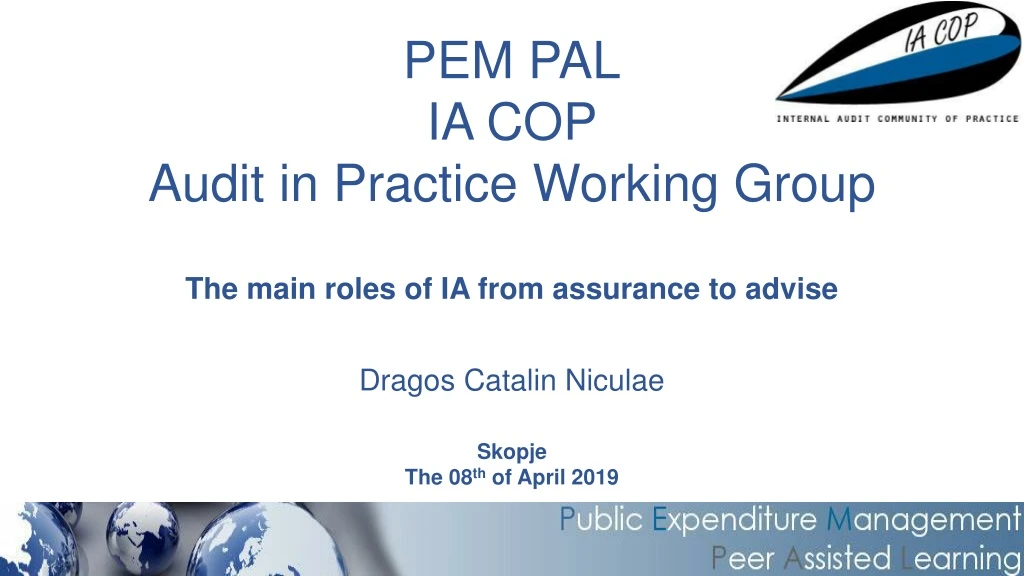

PEM PAL IA COP Audit in Practice Working Group The main roles of IA from assurance to advise Dragos Catalin Niculae Skopje The 08th of April 2019

SUMMARY • A. Assurance services • Definition • Implementation Standards • Particularities • B. Consultancy services • Definition • Implementation Standards • Particularities • C. Comparative analysis

Assurance Services.An objective examination of evidence for the purpose of providing anindependent assessmenton governance, risk management, and control processes for the organization. (IIA Glossary from INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING )

Assurance Services PerformanceStandards 2010 Planning 2110 Governance 2120 Risk Management 2130 Control 2201 PlanningConsiderations 2210 EngagementObjectives 2220 EngagementScope 2240 EngagementWork Program 2330 Documenting Information 2410 Criteria for Communicating 2440 DisseminatingResults 2500 Monitoring Progress AttributeStandards 1000 Purpose, Authority, andResponsibility 1110 OrganizationalIndependence 1111 Direct Interaction with the Board 1112 Chief Audit Executive Roles beyond Internal Auditing 1130 Impairment to Independence or Objectivity 1210 Proficiency 1220 Due Professional Care

1. Involve the internal auditor’s objective assessment • 2. Provide opinions or conclusions regarding an entity, operation, function, process, system, or other subject matters • 3. The nature and scope of an assurance engagement are determined by the internal auditor • 4. Three parties are involved: • a.the process owner(person or group directly involved with the entity, operation, function, process, system, or other subject matter) • b.the internal auditor (the person or group making the assessment) • c.the user (the person or group using the assessment) Assurance services

Consulting Services.Advisory and related client service activities, the nature and scope of which are agreed with the client, are intended to add value and improvean organization’s governance, risk management, and control processes without the internal auditor assuming management responsibility. (IIA Glossary from INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING )

Consulting Services AttributeStandards Performance Standards 1000 Purpose, Authority, andResponsibility 1130 Impairment to Independence or Objectivity 1210 Proficiency 1220 Due Professional Care 2010 Planning 2120 Risk Management 2130 Control 2201 PlanningConsiderations 2210 EngagementObjectives 2220 EngagementScope 2240 EngagementWork Program 2330 Documenting Information 2410 Criteria for Communicating 2440 DisseminatingResults 2500 Monitoring Progress

1. Are advisory in nature and are generally performed at the specific request of an engagement client. • 2. The nature and scope of the consulting engagement are subject to agreement with the engagement client. • 3. Two parties are involved: • a.the internal auditor (the person or group offering the advice ) • b.the engagement client (the person or group seeking and receiving the advice ) Consulting services

Assurance services Consulting services Specific request of engagement client Trigger factor Internal Auditor assessment Nature and scope Determined by auditor Agreed with engagement client Opinions and conclusions Advisory activity and added value Result 3 2 Parties

Romania experience - Consulting service MioaraDiaconescu Director CHUPIA-Romania

Romania experience - Consulting service • The IAs are reticent to use this type of engagements • Informal consulting missions (not formalized) – especially at the local administration (Fireman method) • Meetings • Telephone

Romania experience - Consulting service Internal Auditors refuse to be involved in the consulting engagements

Romania experience - Consulting service Why? • Restrictions for audits - standards • Not sufficient knowledge for Internal Auditors; difficulties to find the appropriate solutions

Romania experience - Consulting service Misinterpretation of the standards - not be involved in auditable actions • No solutions for management • Loss of management trust • „We don’t need audit” • Audit=control – no solutions for management

List of questions for Panel discussions • The Internal Auditors can be involved in the the design of systems, elaboration of procedures, etc ? 2. Formal versus informal consulting

Thank you for your attention! dragos.niculae@mfinante.gov.ro mioara.diaconescu@mfinante.gov.ro