Download

1 / 26

260 likes | 392 Views

CHARITABLE TAX PLANNING STATISTICS. H. King McGlaughon , Jr., JD, , Wachovia Nonprofit and Philanthropic Services. The number of 501(c)(3) organizations, 1996–2006. PROJECTIONS OF FILINGS.

E N D

CHARITABLE TAX PLANNINGSTATISTICS H. King McGlaughon, Jr., JD,, Wachovia Nonprofit and Philanthropic Services

PROJECTIONS OF FILINGS THE NUMBER OF PROJECTED FILED TAX RETURNS FOR TAX-EXEMPT ORGANIZATIONS (FORM 990s) IS PROJECTED BY THE IRS TO BE 1.023,900 BY THE YEAR 2012

The Dimensions of Giving • More Americans give than individuals from any other country in the world • 80% of US households donate money each year to over 1.5 million charities, social welfare organizations and religious congregations in the U.S. • an estimated 75% of those donors receive no tax benefit from their charitable gifts • As our wealth increases, the percentage contributed rises markedly • 95% of families with a net worth in excess of $1 million give to charitable organizations annually • 98% of families with a net worth in excess of $5 million give annually Source: Chronicle of Philanthropy

The Importance of Giving for the Affluent Source: Boston College - Social Welfare Research Institute & Bankers Trust

The Dimensions of Giving • Aggregate contributions from individuals, corporations and foundations for 2006 was $295 billion, an increase of 5% over 2005 • contributions from individuals (lifetime, at death and through private foundations) made up more than 90% of the total • since 1959 contributions have grown at an average of 3% per year above inflation • contributions fall an average of 0.7% in recession years Source: Center for Philanthropy at Indiana University

LARGEST DONORS 2007 – Leona Helmsley – 4 billion Barron Hilton – 1.2 billion Jon and Karen Huntsman – 627 million T. Denny Sanford – 503 million George Soros – 475 million John Kluge – 400 million See more at: The 2007 Slate 60.

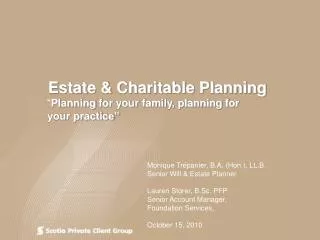

2006 CONTRIBUTIONS: $295 BILLIONBY TYPE OF RECIPIENT ORGANIZATION Environmentand animals$8.863.4% Internationalaffairs$6.392.5% Foundations$21.70 8.3% Arts, culture, and humanities$13.515.2% Unallocatedgiving $16.156.2% Public-society benefit$14.035.4% Human services $25.36 9.7% Religion $93.18 35.8% Education$38.56 14.8% Health $22.548.7%

Average rates of change, 1987–1996 and 1997–2006 by type of recipient (adjusted for inflation) 1997–2006 1987–1996

Total giving, 1966–2006 Inflation-adjusted dollars Current dollars Recessions in yellow: 1969–70; 1973–75; 1980; 1981–82; 1990–91; 2001

Total giving by sourceFive-year spans, adjusted for inflation 1,381.94 $ in billions 1,200.69 829.65 766.08 671.94 597.70 563.91 551.47 1967–71 1972–76 1977–81 1982–86 1987–91 1992–96 1997–01 2002–2006 Individuals Bequests Foundations Corporations Giving USA uses the CPI to adjust for inflation.

Individual giving as a share of income, 1966–2006Personal income and disposable personal income

Philanthropy is one of the top 4 financial issues for UHNW (Ultra High Net Worth) investors Tax Tax 91% Minimization Minimization Asset 89% Management Estate Planning 73% Philanthropy 51%

The Current Market Environment • CRTs are excellent asset management tools • Tax free asset management zone • Ability to move around in market without concern for realization of gains in portfolio • Creates cash flow through Income Tax Deduction, conversion of dividends a/o interest into income stream based on total value • Ability to control taxability of income stream through changes in asset allocation

The Current Market Environment • “CLTs: Leverage Market Down-Turns” • Tax benefits inverse to market conditions • Strong stocks that have lost value • Client intends to hold • Deflated value makes for optimal • CLT funding • Leverage the Market AND the lifetime estate/gift tax exemptions

The Boom in Donor-Advised Funds • Size of Donor Advised Fund Market grew almost 800% from 1995 to 2005 • Proliferation of “commercially sponsored” DAF programs

Growth in Private Foundations: • Over 60,000 private foundations in US today. • 50% were created in last 10 years. • Funding of private foundations is at its highest level ever in terms of annual transfers to private foundation endowments.

Giving to foundations, 1978–2006 $ in billions 29.22 29.50 25.67 16.23 9.12 12.63 6.60 5.30 4.98 Inflation-adjusted dollars 4.96 4.46 2.39 Current dollars 1.61 1978 1981 1986 1991 1996 2001 2006 Data: The Foundation Center