Download

1 / 24

270 likes | 443 Views

PANDEMONIUM IN THE MARKETS. THE PANIC OF 1907. THE FINANCIAL CRISIS OF 2007. EVENTS IN 1906. DEVASTATION. SAN FRANCISCO EARTHQUAKE. Shortly after 5 a.m. on April 18, a 7.8-magnitude quake, unleashed offshore, shook the city for just less than a minute. SAN FRANCISCO EARTHQUAKE 1906.

E N D

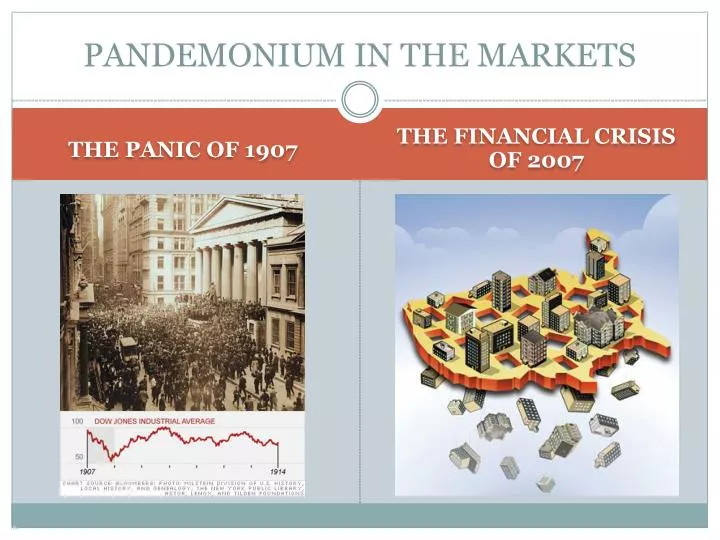

PANDEMONIUM IN THE MARKETS THE PANIC OF 1907 THE FINANCIAL CRISIS OF 2007

EVENTS IN 1906 DEVASTATION SAN FRANCISCO EARTHQUAKE Shortly after 5 a.m. on April 18, a 7.8-magnitude quake, unleashed offshore, shook the city for just less than a minute.

SAN FRANCISCO EARTHQUAKE 1906 UNCONTROLLABLE BLAZE 80% OF THE CITY DESTROYED Though the damage from the quake was severe, the subsequent fires from broken gas lines caused the vast majority of the destruction.

REMEMBERING THE SAN FRANCISCO EARTHQUAKE OF 1906 Audio Clip from an NPR Segment The Fires Raged for Four Days

THE GOLD STANDARD DIFFICULT BALANCING ACT INFLEXIBLE CURRENCY Between 1870 and 1914, many countries adhered to a gold standard, strictly tying national money supplies to gold stocks and standing ready to redeem currency for gold at a fixed exchange rate.

THE WORLD’S FINANCIAL SYSTEM HAD BECOME COMPLEX & INTERRELATED At the end of 1905, nearly 50 percent of the fire insurance in the city of San Francisco was underwritten by British firms. The San Francisco earthquake gave rise to a massive outflow of funds -- of gold -- from London, both immediately after the earthquake and again in the autumn of 1906. The magnitude of the resulting capital outflows in late summer and early autumn 1906 forced the Bank of England to undertake defensive measures to maintain their desired level of reserves. The central bank responded by raising its discount rate two hundred-fifty basis points between September and November 1906. Actions by the Bank of England attracted gold imports and sharply reduced the flow of gold to the United States. By May 1907, the United States had fallen into one of the shortest, but most severe recessions in American history.

EVENTS IN 1907 In October 1907 two brothers, Otto and F. Augustus Heinz, teamed up with Wall Street banker Charles W. Morse in an attempt to manipulate the stock of a copper company. They planned to corner the market in the copper company's shares by buying aggressively in hopes they could later force short sellers to buy them at high prices. The plan was undercapitalized and failed.

PANIC IN THE STREETS News of a cabal involving prominent New York banks in the failed scheme began a crisis of confidence among depositors. As additional institutions were implicated, queues formed outside numerous banks as people desperately sought their savings.

FURTHER COMPLICATING MATTERS Trust companies were a financial innovation beginning in the 1890s. They had many functions similar to state and national banks but were far less regulated. They were able to hold a wide array of assets and were not required to hold reserves against deposits. They could earn a higher rate of return on investments and pay out higher rates, but do this while highly leveraged.

The runs on deposits that sparked the Panic of 1907 were at two of the largest New York City Trust Companies: Knickerbocker Trust and Trust Company of America. A NEW YORK CITY BANK RUN IN NOVEMBER OF 1907

THE IMPACT The crash and panic of 1907 had a dramatic effect on the health of the American economy as well as those world-wide. In the United States: • Commodity prices fell 21% • Industrial production fell more than in any other crisis in American history to that point. • The dollar volume of bankruptcies declared in November was up 47% from the previous year. • The value of all listed stocks in the U.S. sunk 37% • In October and November of 1907 25 banks and 17 trust companies failed. • Gross earnings by railroads fell by 6% in December and production fell 11% • Wholesale prices fell 5%. • Imports shrank 26% • In a few short months, unemployment rose from 2.8% to 8%. • Immigration reached a peak of 1.2 million in 1907 but fell to around 750,000 by 1909.

WHAT WAS DONE? THE “BIG CHIEF” J.P. MORGAN HE WASN’T ELECTED OR APPOINTED, HE JUST FELT IT WAS HIS TIME TO ACT In the absence of a strong federal regulatory structure or any safety nets, the response to this crisis had to be delivered by a private citizen, J.P. Morgan the world’s most powerful banker. He used all of his influence to convince fellow titans of industry to pool their resources and salvage the nation.

LESSONS FROM THE PANIC OF 1907 Audio Clip from an NPR interview. Bucket Shop in 1907 The bucket shop, similar to a betting parlor, was outlawed in 1909 blamed for fueling the speculation surrounding the Panic of 1907. They provided people with a venue to place side bets on the direction they felt stock prices were going, without the inconvenience of owning the security. New York was first to ban them and then other states followed. In 2000, the Commodity Futures Modernization Act revived the bucket shop bet.

THE FINANCIAL CRISIS OF 2007 The world made a huge bet on the U.S. housing market ……….and lost!! By ignoring risk, remaining irrationally optimistic, and forgoing transparency through a wild array of fantastically complicated investment vehicles, the world’s financial markets were managed like an unsuccessful casino. The underlying assumptions at the foundation were that housing prices never fall and homeowners almost always pay back their mortgages.

THE ORIGINS OF THE CRISIS During and after the mild recession of 2001, the Fed lowers interest rates Former Fed Chairman Alan Greenspan

THE ORIGINS OF THE CRISIS Former President George Bush Strongly promotes home- ownership. In 2002, the Bush administration made a very public promotion of the importance of homeownership. “We can put light where there’s darkness, and hope where there’s despondency in this country. And part of it is working together as a nation to encourage folks to own their own home” –President Bush, October 15, 2002.

CAUSES OF THE CRISIS Highly complex forms of financing By June of 2007, financial firms and hedge funds owned more than $2 trillion of securitized debt from sub-prime loans. The momentum behind the expansion of homeownership led the government to reduce regulations and capital requirements for making loans. This led to a dizzying amount of innovative ways to get less qualified borrowers a mortgage and deflect the loan originator from the weight of the risk. Mortgages could be bundled and sold around the world as securities.

CAUSES OF THE CRISIS The agencies trusted to warn investors failed Risk rating agencies The MBS were multi-layered securities constructed of mortgages of differing quality levels. The obligations of solid borrowers were mixed with the sub-prime variety in a manner that made it very difficult for experts to calculate risk. The assumption that U.S. housing was a sure bet led agencies to rate these as AAA lowering investor’s guard.

EFFECTS OF THE CRISIS What were we thinking? “The Perfect Storm” Homeownership peaks in early 2005 at 70% of households The Fed raises interest rates Home prices fall ARMs adjust higher increasing payments for sub-prime borrowers Borrowers default in waves Dozens of sub-prime lenders file for bankruptcy The substantial holdings of MBS world-wide tank and some of the biggest institutions gasp for air. Fannie and Freddie seized by the federal government.

“FINANCIAL WEAPONS OF MASS DESTRUCTION” Financial institutions were allowed to book bets on whether people would default on their mortgages. CDS are private insurance contracts that paid off if the investment went bad, but you didn’t actually have to own the investment to collect on the insurance. These bets were unregulated and the big investment houses didn’t have to set aside any money to cover their bets.

The Federal Government releases its entire arsenal With a great deal of uncertainty, the federal government unleashed a tsunami of remedies in an attempt to contain and destroy the contagion. Showing little regard for the burdens being placed on future generations, massive sums of money were created to capture toxic assets and bailout key elements. In the process, the taxpayers took over several familiar companies and had to accept the consequences of greed.

BAILOUT TRACKER Sources: Federal Reserve, Treasury, FDIC, CBO, White House (as of 11/16/2009)

SIMILARITIES 1907 2007 Highly complex and linked financial system Strong growth in the economy starting in 1900 Many people and institutions highly leveraged Innovative form of finance: Trust Companies Stock market setting all-time highs A limited role for government Markets swing from great optimism to great pessimism Global interdependent financial system Vibrant economic recovery after recession in 2001 Lenders willing to take more risk in making loans Unregulated financial institutions: Hedge Funds Companies reporting record earnings Absence of many safety buffers Dow 14,164 to 6500 in 16 months

DIFFERENCES 1907 2007 J.P. Morgan, a private citizen, orchestrates the bailout. The Panic lasted for six weeks, though the economy didn’t return to pre-Panic levels until 1909 Many banks were closed and depositors lost their savings The nation was on the gold standard and the supply of money was fixed The San Francisco earthquake was a catalyst for the Panic The climate toward business was hostile in advance The Federal Reserve and Treasury Department organize the reaction The event has been unfurling for over two years Many banks have closed but have been folded into healthier banks and depositors have yet to lose any of their savings The nation uses Federal Reserve notes which are apparently in limitless supply Hurricane Katrina was generally benign as a catalyst The climate toward business was friendly in advance

![get [PDF] Download Where's Waldo? Paper Pandemonium](https://cdn7.slideserve.com/12443437/slide1-dt.jpg)

![get [PDF] Download Where's Waldo? Paper Pandemonium](https://cdn7.slideserve.com/12521657/slide1-dt.jpg)