Download

1 / 10

100 likes | 108 Views

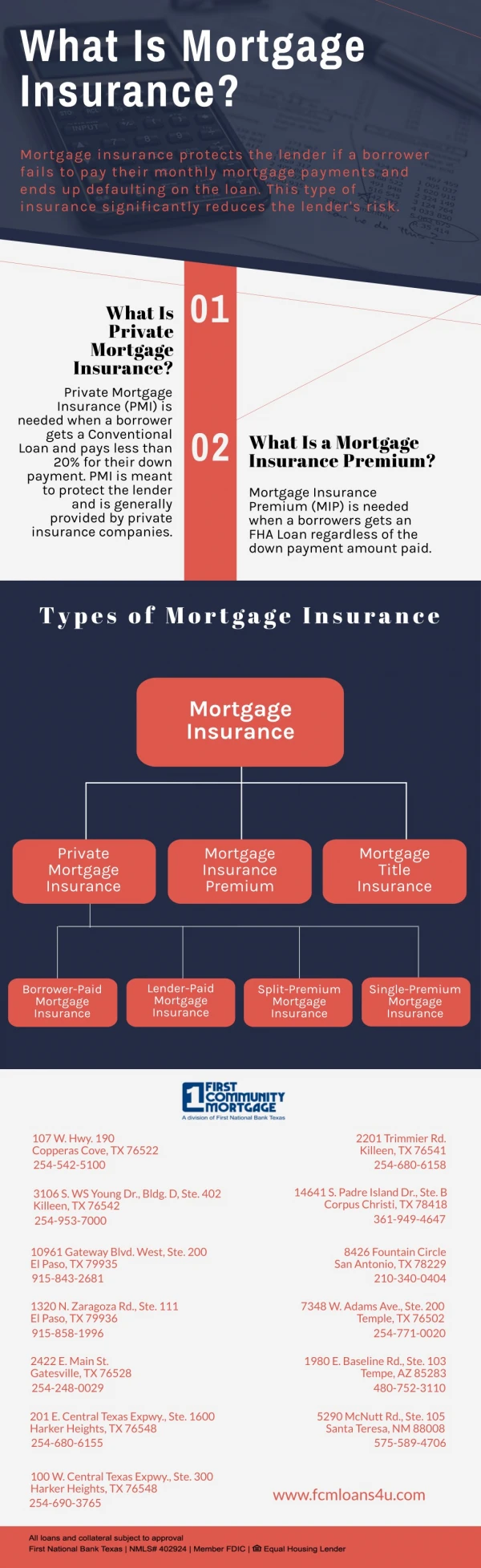

PMI is a mortgage insurance provided by a private mortgage insurance company designed to protect the lender in case the borrower stops making their monthly payments. Most lenders generally require PMI for a loan with a loan-to-value (LTV) percentage in excess of 80 percent<br>

E N D

What is Private Mortgage Insurance (PMI) David Reecher

David Reecher PMI is a mortgage insurance provided by a private mortgage insurance company designed to protect the lender in case the borrower stops making their monthly payments. Most lenders generally require PMI for a loan with a loan-to-value (LTV) percentage in excess of 80 percent

David Reecher If you can put 20% down on your purchase, you can avoid this expense. If you do need to get PMI (which is very common especially for first time homebuyers), make sure you keep an eye on how much your houses increases in value, and how much principal you pay down.

David Reecher “Your bank is not going to tell you when you no longer need PMI, so you must bring it up at the time your mortgage balance is 80% or less of the value of your house” David Reecher said. Removing your PMI payment will be a nice reduction in your monthly payment.

David Reecher David Reecher and his Rapid Results team specializes in buying and selling homes throughout the state of Maryland. David has more than 20 years of real estate experience.

Request Cancellation As mentioned above, if you’ve reached an 80% LTV, you can ask your lender to cancel your PMI payments. This must be in writing and you need a good payment history if you wish to get approved by your lender.

Wait for Your PMI to Play Out as Normal It may work for you to wait it out and continue making the stipulated PMI payments and wait for it to play out as normal. If you forget to request cancellation by the time you reach 20% equity, your lender is obliged to automatically cancel when you hit 22 percent equity.

Pay a One-time Premium Paying monthly is not the only option. You can pay upfront as part of your closing cost or add to your loan amount. Note however, that if you refinance or move at a later date, you likely will not be able to get back what you paid upfront. Single-premium option is not available with every mortgage company so reach out to them before your mortgage closing to find out if they offer this option.

Make a Down Payment of 20% or Higher Save for a minimum 20 percent down payment before you start your homebuying journey. This will put you at 80 percent LTV and will save you on your mortgage payments. Keep in mind, your PMI depends on your credit rating and LTV and can range from $30-$70 per month for every $100,000 borrowed.