Download

1 / 2

20 likes | 143 Views

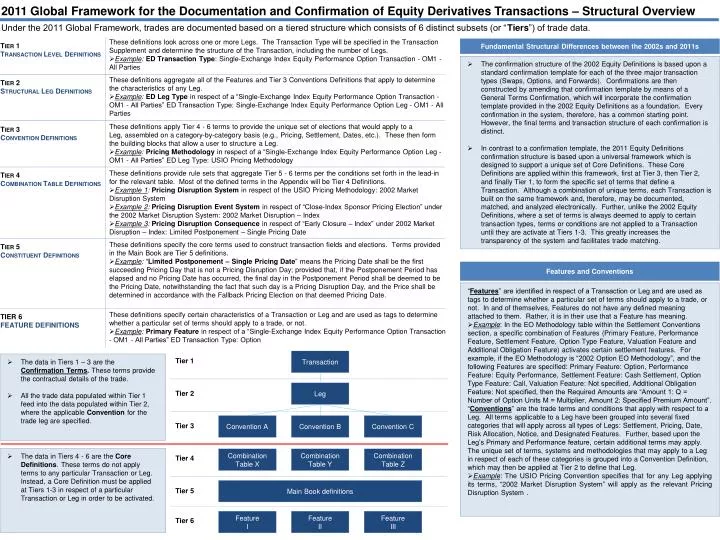

2011 Global Framework for the Documentation and Confirmation of Equity Derivatives Transactions – Structural Overview. Under the 2011 Global Framework, trades are documented based on a tiered structure which consists of 6 distinct subsets (or “ Tiers ”) of trade data.

E N D

2011 Global Framework for the Documentation and Confirmation of Equity Derivatives Transactions – Structural Overview Under the 2011 Global Framework, trades are documented based on a tiered structure which consists of 6 distinct subsets (or “Tiers”) of trade data. • These definitions look across one or more Legs. The Transaction Type will be specified in the Transaction • Supplement and determine the structure of the Transaction, including the number of Legs. • Example:ED Transaction Type: Single-Exchange Index Equity Performance Option Transaction - OM1 - All Parties Tier 1 Transaction Level Definitions Fundamental Structural Differences between the 2002s and 2011s • The confirmation structure of the 2002 Equity Definitions is based upon a standard confirmation template for each of the three major transaction types (Swaps, Options, and Forwards). Confirmations are then constructed by amending that confirmation template by means of a General Terms Confirmation, which will incorporate the confirmation template provided in the 2002 Equity Definitions as a foundation. Every confirmation in the system, therefore, has a common starting point. However, the final terms and transaction structure of each confirmation is distinct. • In contrast to a confirmation template, the 2011 Equity Definitions confirmation structure is based upon a universal framework which is designed to support a unique set of Core Definitions. These Core Definitions are applied within this framework, first at Tier 3, then Tier 2, and finally Tier 1, to form the specific set of terms that define a Transaction. Although a combination of unique terms, each Transaction is built on the same framework and, therefore, may be documented, matched, and analyzed electronically. Further, unlike the 2002 Equity Definitions, where a set of terms is always deemed to apply to certain transaction types, terms or conditions are not applied to a Transaction until they are activate at Tiers 1-3. This greatly increases the transparency of the system and facilitates trade matching. • These definitions aggregate all of the Features and Tier 3 Conventions Definitions that apply to determine the characteristics of any Leg. • Example: ED Leg Type in respect of a “Single-Exchange Index Equity Performance Option Transaction - OM1 - All Parties” ED Transaction Type: Single-Exchange Index Equity Performance Option Leg - OM1 - All Parties Tier 2 Structural Leg Definitions • These definitions apply Tier 4 - 6 terms to provide the unique set of elections that would apply to a • Leg, assembled on a category-by-category basis (e.g., Pricing, Settlement, Dates, etc.). These then form the building blocks that allow a user to structure a Leg. • Example: Pricing Methodology in respect of a “Single-Exchange Index Equity Performance Option Leg - OM1 - All Parties” ED Leg Type:USIO Pricing Methodology Tier 3 Convention Definitions • These definitions provide rule sets that aggregate Tier 5 - 6 terms per the conditions set forth in the lead-in for the relevant table. Most of the defined terms in the Appendix will be Tier 4 Definitions. • Example 1: Pricing Disruption System in respect of the USIO Pricing Methodology: 2002 Market Disruption System • Example 2: Pricing Disruption Event System in respect of “Close-Index Sponsor Pricing Election” under the 2002 Market Disruption System: 2002 Market Disruption – Index • Example 3: Pricing Disruption Consequence in respect of “Early Closure – Index” under 2002 Market Disruption – Index: Limited Postponement – Single Pricing Date Tier 4 Combination Table Definitions • These definitions specify the core terms used to construct transaction fields and elections. Terms provided • in the Main Book are Tier 5 definitions. • Example: “Limited Postponement – Single Pricing Date” means the Pricing Date shall be the first succeeding Pricing Day that is not a Pricing Disruption Day; provided that, if the Postponement Period has elapsed and no Pricing Date has occurred, the final day in the Postponement Period shall be deemed to be the Pricing Date, notwithstanding the fact that such day is a Pricing Disruption Day, and the Price shall be determined in accordance with the Fallback Pricing Election on that deemed Pricing Date. Tier 5 Constituent Definitions Features and Conventions • “Features” are identified in respect of a Transaction or Leg and are used as tags to determine whether a particular set of terms should apply to a trade, or not. In and of themselves, Features do not have any defined meaning attached to them. Rather, it is in their use that a Feature has meaning. • Example: In the EO Methodology table within the Settlement Conventions section, a specific combination of Features (Primary Feature, Performance Feature, Settlement Feature, Option Type Feature, Valuation Feature and Additional Obligation Feature) activates certain settlement features. For example, if the EO Methodology is “2002 Option EO Methodology”, and the following Features are specified: Primary Feature: Option, Performance Feature: Equity Performance, Settlement Feature: Cash Settlement, Option Type Feature: Call, Valuation Feature: Not specified, Additional Obligation Feature: Not specified, then the Required Amounts are “Amount 1: Q = Number of Option Units M = Multiplier, Amount 2: Specified Premium Amount”. • “Conventions” are the trade terms and conditions that apply with respect to a Leg. All terms applicable to a Leg have been grouped into several fixed categories that will apply across all types of Legs: Settlement, Pricing, Date, Risk Allocation, Notice, and Designated Features. Further, based upon the Leg’s Primary and Performance feature, certain additional terms may apply. The unique set of terms, systems and methodologies that may apply to a Leg in respect of each of these categories is grouped into a Convention Definition, which may then be applied at Tier 2 to define that Leg. • Example: The USIO Pricing Convention specifies that for any Leg applying its terms, “2002 Market Disruption System” will apply as the relevant Pricing Disruption System . • These definitions specify certain characteristics of a Transaction or Leg and are used as tags to determine whether a particular set of terms should apply to a trade, or not. • Example: Primary Feature in respect of a “Single-Exchange Index Equity Performance Option Transaction - OM1 - All Parties” ED Transaction Type: Option TIER 6 FEATURE DEFINITIONS Transaction Tier 1 • The data in Tiers 1 – 3 are the Confirmation Terms. These terms provide the contractual details of the trade. • All the trade data populated within Tier 1 feed into the data populated within Tier 2, where the applicable Convention for the trade leg are specified. Leg Tier 2 Convention A Convention B Convention C Tier 3 • The data in Tiers 4 - 6 are the Core Definitions. These terms do not apply terms to any particular Transaction or Leg. Instead, a Core Definition must be applied at Tiers 1-3 in respect of a particular Transaction or Leg in order to be activated. Combination Table X Combination Table Y Combination Table Z Tier 4 Main Book definitions Tier 5 Feature I Feature II Feature III Tier 6

2011 Global Framework for the Documentation and Confirmation of Equity Derivatives Transactions – Structural Overview Determining Applicable Core Definitions Vertical Perspective (by Tier) Horizontal Perspective (by Category) Within the CTT, terms are arranged first according to Tier, then by Category Within the Appendix, terms are arranged first according to Category (by Article), then by Tier Tier 1 ED Transaction Type Transaction Conventions Structural Leg Conventions Pricing Conventions Single-Exchange Index Equity Performance Option Transaction - OM1 - All Parties ED Transaction Type Single-Exchange Index Equity Performance Option Transaction - OM1 - All Parties ED Leg Type Single-Exchange Index Equity Performance Option Leg - OM1 - All Parties Pricing Methodology Tier 2 Single-Exchange Index Equity Performance Option Transaction - OM1 - All Parties ED Leg Type Single-Exchange Index Equity Performance Option Transaction - OM1 - All Parties Single-Exchange Index Equity Performance Option Leg - OM1 - All Parties USIO Pricing Methodology Single-Exchange Index Equity Performance Option Leg - OM1 - All Parties USIO Pricing Methodology Pricing Disruption System Tier 3 Single-Exchange Index Equity Performance Option Leg - OM1 - All Parties Pricing Methodology 2002 Market Disruption System USIO Pricing Methodology Tier 4 USIO Pricing Methodology Pricing Disruption System 2002 Market Disruption System Pricing Disruption Event System for Close-Index Sponsor Pricing Election 2002 Market Disruption System Tier 4 2002 Market Disruption System Pricing Disruption Event System for Close-Index Sponsor Pricing Election 2002 Market Disruption - Index 2002 Market Disruption - Index 2002 Market Disruption - Index Pricing Disruption Consequence for Early Closure - Index Tier 4 2002 Market Disruption - Index Pricing Disruption Consequence for Early Closure - Index Limited Postponement – Single Pricing Date Limited Postponement – Single Pricing Date Tier 5 Section 9.8.7 “Limited Postponement – Single Pricing Date” means the Pricing Date shall be the first succeeding Pricing Day that is not a Pricing Disruption Day; provided that, if the Postponement Period has elapsed and no Pricing Date has occurred, the final day in the Postponement Period shall be deemed to be the Pricing Date, notwithstanding the fact that such day is a Pricing Disruption Day, and the Price shall be determined in accordance with the Fallback Pricing Election on that deemed Pricing Date.